Ask 100 Americans what caused the 2008 financial crisis, and 99 will supply some version of the “Standard Narrative.” That is, they will say that the crisis was caused by some mix of the following factors:

- Excessive official faith in free markets,

- Wall Street’s outsized political influence,

- Deregulation,

- Financial innovation and,

- The moral turpitude of bankers.

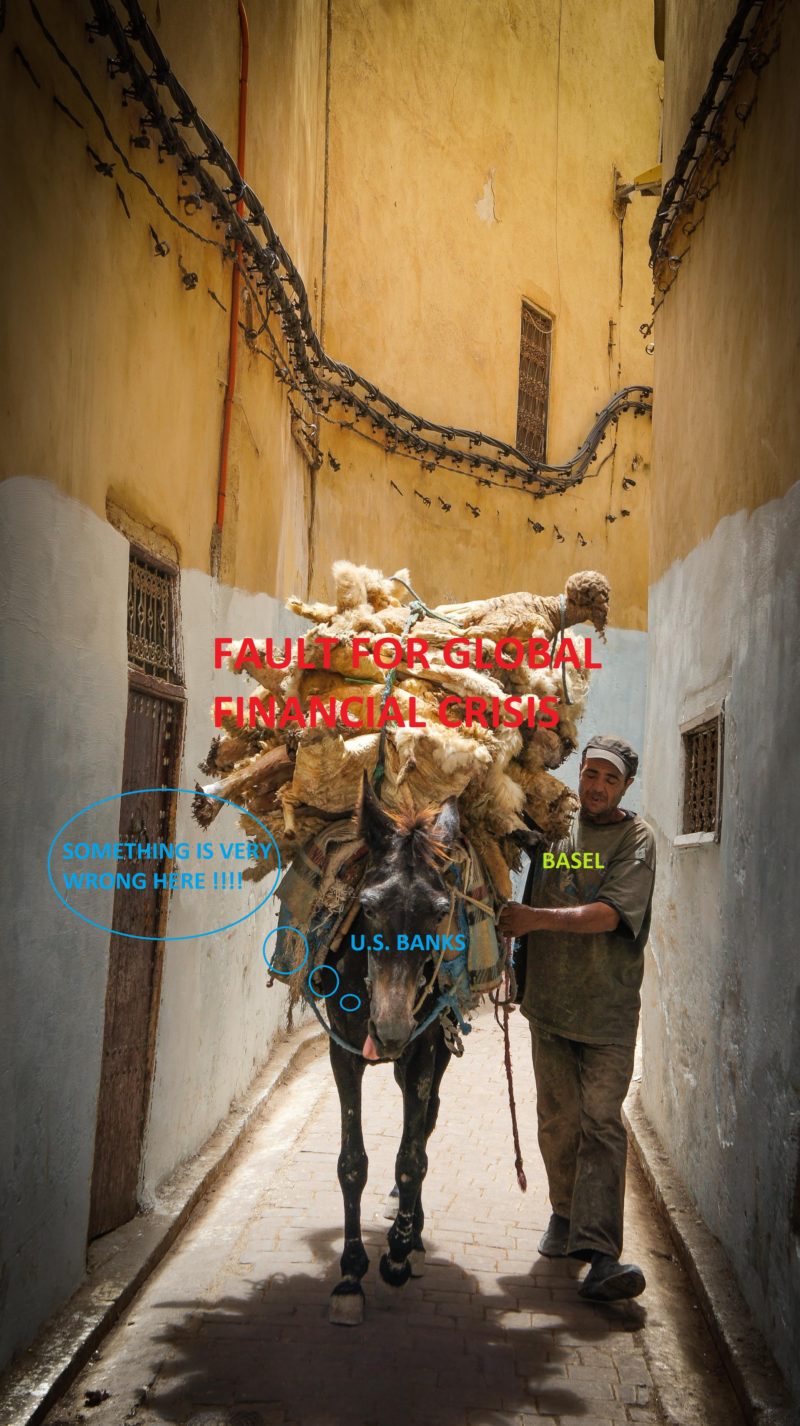

However, as we will show, the standard narrative is grossly inadequate to explain the crisis. The crisis was both far more complex and far more international than is represented in the standard narrative. But its underlying cause was deceptively simple: an obscure set of regulatory edicts known as the Basel I and Basel II capital standards.

Thus, when we jointly take a peek under the hood, I believe you’ll find that the crisis was more a case of bad regulation than it was a case of free markets run amok. In this paper, we will discuss the weaknesses of the standard narrative and the central significance of Basel. We will argue that the failure of policymakers to grasp the true nature of the crisis led to a misguided regulatory response intent on punishing commercial banks. This response burdened the banking industry and weighed heavily on the post-crisis economic recovery. We will conclude by arguing that policymakers should reappraise bank regulation and step back from Dodd Frank’s back door nationalization of the commercial banking industry.

Here’s a brief outline of how the paper will progress :

- The Financial Crisis – A National Trauma: We’ll start with a comprehensive review of the financial crisis and why the standard narrative is insufficient in explaining the events that transpired

- Basel – The True Cause of the Crisis: An introduction to Basel I and Basel II, and why they were those specific regulations created “The Perfect Storm.”

- Modern Regulation: The framing of US banks and why Dodd-Frank & Basel 3 are bad for the economy

- Policy Recommendations: My recommendations for changes in the bank regulatory structure.

Part 1: The Financial Crisis – A National Trauma

The financial crisis of 2007-8 was more than just an economic disaster for the United States. It was a national trauma. To an extent, that we are only now beginning to appreciate, it tore apart the fabric that had – however tenuously – bound our society together for decades. The crisis brought to the surface long-simmering political and cultural divisions. A conviction has taken hold among all political persuasions that the system is not just unequal but rigged.

The crisis has deeply shaken our confidence in capitalism. Nearly half of Americans under 30 today say they prefer Socialism to Capitalism. Thinkers as different as Stephen Pinker and Jonah Goldberg caution that the entire “Enlightenment Project” – reason, rule of law, and the systematic search for truth – is under threat.

Capitalism has its flaws, but in 300 years it has more than doubled lifespans, raised billions worldwide out of poverty and today allows most of us to live in freedom, comfort, and safety that our forebears could not have dared to imagine. Possessing only imperfect knowledge about how this wealth-creating system operates, we must be careful about the constraints we place upon it.

Any society must strive to strike a balance between free markets and regulation. I am convinced that for banks, in particular, the pendulum has swung much too far toward increased regulation and state micro-management. I believe that this trend is largely due to policymakers’ misunderstanding of the nature of the financial crisis. I hope that this essay enhances our understanding of the crisis and convinces many of the legislative errors it spawned.

The Standard Narrative: “Banks” caused the crisis

To tease out the truth about the crisis, let’s begin by reviewing the explanation that has become consensus, if not gospel. We will refer to this conventional wisdom as the “standard narrative”. While there are some variations, these tend to be its key tenets:

- Excessive faith in free-market dogma. Starting with the Reagan administration, faith in free-market capitalism and skepticism of government intervention had been in the ascendancy.

- Undue Influence of Wall Street. In administrations of both parties, Wall Street executives held senior advisory and cabinet positions. Political contributions and lobbying enabled Wall Street to influence policy in its favor.

- Deregulation. According to the standard narrative, this combination of free-market zeitgeist and Wall Street influence enabled banks to become increasingly deregulated.

- Financial Innovation. Set free from oversight, banks concocted a slew of new, increasingly complex products, including Private Mortgage-backed Securities (PMBS) and Credit Default Swaps (CDS.)

- Lending standards and corporate ethics were debauched. Generous pay structures created perverse incentives. Sub-prime mortgages were fraudulently forced on unsuspecting borrowers. Because banks were selling assets on to greater fools, they didn’t care if a loan they originated could be repaid.

- Rating Agencies rubber-stamped ratings for PMBS, trading AAA ratings for fees.

- Regulators fell asleep at the switch, victims of the same faith in free and efficient markets that infected policymakers.

- Bankers “bet the bank” because their institutions were “too big to fail.” The “Standard Narrative” alleges that “Moral Hazard” pushed bankers to take outsize risk: if they won, they’d get rich, if they lost, they’d get bailed out and taxpayers would foot the bill.

- A “Savings Glut” provided the funds for the bubble. This glut was caused by economic growth and high savings rates in Germany, Japan, and especially China which resulted in large trade surpluses.

- The Fed kept interest rates too low for too long. This kept sub-prime loans affordable and encouraged mortgage refinancing, enabling citizens to live off debt.

While some of these points contain kernels of truth, for the most part, they are small potatoes. To focus on these is to miss just about everything that was important about the crisis.

The Standard Narrative is Deeply Flawed.

The most important thing about the standard narrative is what it leaves out; it barely touches on or simply ignores the most salient features of the crisis.

Let’s take each of these flaws one by one:

- The standard narrative focuses myopically on events in the United States. It ignores the international dimension of the crisis. In fact, the crisis was worse in Europe than in the United States. The first large institution to fail was Northern Rock in the UK, nearly a full year before Lehman. Far more European than American Institutions failed or were restructured. Entire industries in Europe were obliterated – the Cajas in Spain, the building societies in the UK, the Landesbanken in Germany. Ireland, Iceland, Portugal, Greece, and the Baltics were devastated. As Adam Tooze points out in his magisterial book “Crashed,” fully half of Fed assistance in the crisis went to European banks. Much more on this later.

- The US commercial banking industry proved resilient. Unforgivably, the standard narrative conflates the solid US commercial banks and their flimsy foreign and shadow bank competitors. By “commercial banks” I mean deposit-taking institutions regulated by the Fed, the FDIC and / or the OCC. Commercial banks overall suffered only moderate losses. Shadow banks (US credit institutions such as WAMU, Fannie Mae, AIG, Countrywide, General Motors, and Merrill Lynch that were NOT regulated as commercial banks) and European banks caused the vast bulk of the problems.

- The standard narrative fails to identify the source of the tsunami of funds that flooded our credit markets between 2000 and 2006. Certainly, hypotheses exist – notably the Savings Glut — but this is clearly inadequate. China’s dollar reserves in 2008 were about $2 trillion. This is not nearly large enough to account for the crisis – including at least $4 trillion in Fed support to Europe alone. Plus, both Japan and China held agency and treasury securities almost exclusively, not private-label RMBS.

- The events of 2007-8 were a liquidity crisis, not a solvency crisis. That is, the crisis was a run, a panic — a sudden loss of confidence in the ability of counterparties to make a payment or obtain good collateral. The long-term solvency of most American institutions was never threatened.

A Brief Digression on Solvency and Liquidity

Point #4 is critical if one is to understand the financial crisis. The following section is a brief but essential discussion of the linkage between liquidity and solvency.

By “solvency” we simply mean that the value of a firm’s assets is greater than the value of its liabilities.

By “liquidity” we mean the ability to obtain cash to meet one’s obligations. For most businesses, cash in hand is the best source of liquidity, followed by cash flow from operations. Accounts receivable and inventory are secondary sources since they can be readily sold, albeit at a discount. Plant and equipment are tertiary sources since they can only be sold with great difficulty, or can serve as collateral for a bank loan (they are “illiquid” ),. Most businesses are “liquid” because they generate cash and have more short-term assets than liabilities.

In contrast, banks are “illiquid” by definition. They are the mirror image of the “real” business economy.

It’s easy to see why this is so. When a bank makes a loan, it creates a demand deposit:

- Debit: Bank loan $1,000

- Credit: Customer Checking account $1,000

(This, incidentally, is how money is created.) The customer can draw on her checking account immediately and even spend the whole amount. The loan, however, might not come due for years. (The best description I have seen of this process appears, of all places, in “Sapiens” by Yuval Harari, pages 305-315.)

Most banks, especially large banks, need to borrow in the normal course of business to pay maturing obligations. For instance, if the depositor described above does decide to spend what she has been lent, then the bank must immediately borrow to replace those funds. Many such borrowings are short-term, often overnight. Short-term creditors to banks regularly “roll” out of maturing obligations into new ones.

This all works fine 99.9% of the time. But if, as in Spring 2007 and worsening into 2008, those who extend short-term credit to banks sense a problem, they may elect not to renew their loan.

Bank creditors have every incentive to pull their loan at the slightest hint of trouble. There is no upside in maintaining the position, but big downside if it turns out rumored problems are real. “Shoot first, ask questions later” is the operative strategy.

Concerns about one bank can quickly cascade to other banks, whether real problems exist or not. It doesn’t help that banks are “black boxes” to most investors. That is, as Gary Gorton emphasizes, creditors lack sufficient information to make an informed decision.

At times like this, a bank has 3 alternatives if it wishes to honor its maturing obligations.

- It can try to find other creditors to borrow from

- It can sell assets

- It can borrow from the central bank

With the first alternative closed off and an understandable reluctance to go hat in hand to the Fed, banks begin to sell assets. Carefully, at first. Then, indiscriminately. The potential for a panic arises.

In a panic, values of all assets collapse regardless of whether they are fundamentally “Good” or “Bad”.

“If you can’t sell what you want to sell, you’ve got to sell what you can.”

Art Cashen, CNBC

Unfortunately, in 2007-8, it turned out that many assets were not as liquid as they appeared to be pre-crisis. As sellers became increasingly desperate, buyers stepped away out of fear or to hoard cash and wait for the bottom. Gaping spreads opened up between bid and ask prices as “Price Discovery” broke down. A feedback loop emerged as investors worried that the panic-driven asset price collapse presaged fundamental problems. This caused more selling.

As the liquidity panic drove down asset prices, the solvency of some institutions was called into question. Since a market in panic mode can’t distinguish between good assets and bad, let alone good banks and bad, all banks were considered guilty until proven innocent. Any attempt to confidently ascertain a bank’s solvency in such conditions was a fool’s errand.

At such times, the central bank must stand ready to provide funds to banks. In the US, the Fed typically operates through the “Discount Window” to provide funds. In 2008, they operated through a variety of inventive programs. The PR image of going to the discount window certainly gives the appearance of a bailout, but the safety net for banking is a necessary evil in the reserve banking structure most of the world uses today.

Some folks like to insist that there’s a clear distinction between liquidity and solvency. In the long term, there is certainly a big distinction. But in the very short term (the time frame in which these decisions must be made) it’s a distinction without a difference. There is not adequate time or information to conduct effective triage

How can we be certain that 2007-8 was a liquidity crisis and not a solvency crisis? Because the AAA-rated PMBS tranches that caused most of the losses and were written down as much as 40% in the heat of the panic, soon recovered to 100 cents on the dollar, or nearly so.

Even the FCIC (Financial Crisis Investigation Committee), with every incentive to dissemble, said, “most of the triple-A tranches . . . . have avoided actual cash losses through 2012 and may avoid significant unrealized losses going forward.”

Lawrence Ball in his book “The Fed and Lehman Brothers” argues convincingly that even Lehman may not have been insolvent prior to its bankruptcy. It almost certainly had sufficient collateral to borrow from the Fed. But the Fed, for whatever reason, declined to support Lehman, and it just ran out of cash with which to pay its debts.

A note on terminology.

Let’s be very careful about exactly what we mean when we say “bailout.” When the public thinks “bailout,” it might mean anything from Fed borrowing to some sort of under-the-table payoff to wealthy shareholders.

When I say bailout, I mean that the government provides equity funding to an insolvent organization with no immediate prospect for recovery. In my kind of bailout, shareholders are typically wiped out, mainly through dilution.

Loans from the Fed to commercial banks were emphatically not bailouts. This was simply the Fed doing its job.

Part 2: Basel – The True Cause of the Crisis

So, to truly understand the financial crisis one must clear one’s head of the standard narrative and reject most of what one may have read or heard or viewed on the big screen. The truth lies in an arcane set of regulatory directives that few economists or journalists have even heard of, let alone understand: the Basel I and Basel II capital standards. Many have criticized Basel for not preventing the crisis, but few appreciate its role as the central underlying cause.

Before discussing Basel in detail, a brief digression on bank capital standards might be in order.

Traditionally, regulators have required banks to maintain a minimum amount of capital. This capital cushion protects creditors (largely depositors) against losses on the bank’s asset portfolio. In practice, modern bank capital requirements have ranged between $5 and $10 in capital for every $100 in assets. This equates to a 5% to 10% “leverage ratio.”

With a 5% leverage ratio, a bank with assets of $100 can sustain a $5 loss before shareholders are wiped out. Any greater loss is absorbed by the creditors (mostly depositors). It’s roughly analogous to buying a $100,000 house with a $95,000 mortgage and a $5,000 down payment. (Your leverage ratio is 5%.) If the value of your house drops, the most you can lose is $5,000. Anything more than that and the bank takes the hit (and the house.)

Basel was a sea change for bank regulation and capital standards in particular. Promulgated in 1988, it was intended as an effort to unify international banking regulations. It was not intended as an act of deregulation.

Basel made sense in theory as regulations occasionally do. Its objective was to make a given bank’s capital requirement correspond to the riskiness of that bank’s balance sheet. Its method was to assign “risk weightings” to each class of assets. Sovereign debt (e.g. Treasury Bills) was assigned zero risk weighting – no capital required. Commercial loans were assigned 100% risk weightings – full capital allocation. Mortgages were assigned a risk weighting of 50%, requiring half the capital of a commercial loan. Thus, a bank whose assets consisted of 100% T Bills would require almost no capital, while a bank specializing in construction lending would require the maximum.

Fair enough. Unfortunately, there were at least four big problems with Basel:

- There was no lower limit on the leverage ratio. (Providentially, US commercial banks retained a leverage constraint, and that is what saved them.)

- Large banks (mostly European banks) were given license to value their own trading books

- Minimal attention was paid to maturity and currency mismatches (a key to the crisis.)

- Risk weightings were arbitrary and ultimately proved bogus. For instance, among the assets assigned very low-risk weightings were Greek Sovereign Debt and AAA-rated sub-prime CDO’s (Collateralized Debt Obligations.)

Basel II was issued in 2004, and it doubled down on bank self-regulation. It allowed many of the largest banks to rate their own loan portfolios as well as their trading books. In effect, European regulators abdicated any supervisory role in bank regulation.

The Basel Bubble

In at least two ways, Basel heightened worldwide financial risk.

First, Basel amplified systemic leverage, making financial firms less able to withstand a large loss, as a top-heavy ship is vulnerable to a rogue wave.

We have talked a little about bank leverage, identifying 5% as a rough historical standard. Thanks to Basel, large international banks became much more leveraged than that. Some European banks were off the charts. The leverage ratio for Barclay’s in 2007 was 2.1%, and 1.4% for UBS. Even mighty Deutsche Bank, that paragon of financial probity, was leveraged nearly 100 to 1.

Second, by stoking an insatiable appetite for assets deemed “low risk,” Basel set the stage for credit inflation on a colossal scale. Paramount among these “low-risk” assets were residential mortgage loans (risk weight 50%) and highly rated MBS (risk weight 20%.) With these, a Eurobank could leverage $1 of capital 20 to 50 times – achieving two to five times the returns on equity of a corporate loan with an equivalent yield.

These risk weightings may have made sense for conventional mortgages or MBS. But Basel didn’t differentiate between conventional and sub-prime mortgages. For European banks desperate to deploy capital in low-risk assets (as defined by Basel), US sub-prime PMBS were the perfect candidate. For one thing, the yield was higher than that of conventional mortgages. More importantly, the potential market was far bigger than anything they could find in Europe. Plus, securitizations and related derivative spinoffs could generate huge fees for traders. The lower-rated tranches of the PMBS were sold to investors, while Eurobanks retained the senior AAA tranches. Eventually, thanks to further regulatory changes and financial machinations, these assets could be leveraged nearly 100 to 1.

How big was this Basel bubble? I estimate that between 2000 and 2007 European banks booked about € 7 trillion in “excess” assets due purely to increasing leverage. This meant that by 2007, the European banking system held roughly €12 trillion in assets in excess of what would have been acceptable at a leverage ratio of 5%. This was fully a third of the European banking system assets. Many, if not most, of these assets were US-domiciled.

Permit me to observe that these are very, very, very big numbers. Seven trillion Euros was more than three times China’s dollar reserves. It was roughly equal to the total value of US commercial bank loans. It was roughly equal to the US national debt at the time.

Most Eurobanks conducted these operations through their US offices (often former US brokers like First Boston, Bankers Trust, SG Warburg, and Paine Webber.) In what is by far the most important analysis of the crisis – Hyun-Song Shin’s “The Global Banking Glut” (2012) — Shin details how Eurobanks lent money in the US mostly through PMBS and financed those mortgages with short term borrowing, largely from money market funds. This arrangement of long-maturity PMBS with financed with money market funds implied a colossal maturity mismatch and an equally large, albeit latent, foreign exchange mismatch, since the PMBS were priced in dollars.

In retrospect, it is hard to fathom why the European banks failed to see that they were sitting on a powder keg. As the panic started rolling, and especially after Lehman went bankrupt and a large money market fund “broke the buck,” it became impossible for Eurobanks to obtain dollar funding. Their own central banks had nowhere near enough dollars and the Fed was limited in its ability to lend directly to foreign institutions. Finally, the Fed resorted to lending many trillions of dollars to the European central banks, who divvied them out to their institutions.

In a very real sense, then, the gist of the financial crisis was a Fed bailout of Europe. For a moment, all of Europe was poised on the knife-edge of literally going bust. Here is Adam Tooze, “Lesser countries in this kind of predicament would be directed to the IMF. . . . But for the ECB or the Bank of England to have resorted to the IMF would in 2008 have been a disaster of historic proportions.”

US shadow banks compounded the mania. Brokers had long been lightly regulated by the SEC, which focused less on financial soundness than on investor protection (Also, Patriot Act issues diverted attention from less pressing concerns – understandable at the time.) In 2001, the SEC liberalized the “net capital rule” for brokers, which allowed them to assume even greater leverage. This increase in leverage was largely a competitive response to European bank leverage. (Cosmetically, shadow bank leverage would have been much greater if US institutions had adhered to the same accounting methods for derivatives as the European banks.)

As Shin’s work suggests, Eurobanks and Shadow banks mostly financed their blistering asset growth with short-term – often overnight – borrowing. The mechanisms that allowed this prodigious borrowing were the Repo and Asset-Backed Commercial Paper (ABCP) markets (Just to throw another acronym into the mix, ABCP typically funded Special Interest Vehicles (SIV’s) which were off-balance-sheet entities used to house PMBS).

Crucially, both Repo and ABCP were collateralized. As such, they were regarded as effectively risk-free by bank creditors. However, the subprime crisis ignited a downward spiral in collateral values as banks scrambled to sell assets to raise cash. Compounding these problems, most of the credit default swaps (CDS) that backstopped these securities also required collateral. In at least two books and many articles, Gary Gorton grippingly details this short-term collateral crisis.

Several further regulatory changes added fuel to the fire. In 2001, a change in the “Recourse Rule” encouraged institutions to sell the high-risk tranches of PMBS and retain the low-risk ones by reducing the capital requirement for low-risk tranches. As both Jeffrey Friedman and Edward Conant emphasize, this stoked huge demand for AA and AAA PMBS — funded short term, naturally. The net result was a small systemic reduction in credit risk and a huge increase in liquidity risk.

As Tamim Bayoumi points out in “Unfinished Business,” three esoteric but critical changes further encouraged Repo lending. First, in 2003 the SEC allowed private MBS to be eligible for repo collateral. Next, in 2005, Repo was given a “Safe Haven” in bankruptcy. Finally, also in 2005, the Basel Committee loosened its capital requirement for Repo.

Much European bank leveraging was done with derivatives. For instance, UBS’s derivatives book exploded from €26 billion in 2001 to €450 billion in 2007 (at which point it exploded for real) – nearly 20% of the company’s assets. Traders and financial managers did all they could to transmute assets into derivatives and jam them into the trading book. There, accounting standards were hazy, capital requirements were minimal, and the firms themselves were in control of valuation.

The bottom line in 2007 was gargantuan systemic counterparty risk. When it all hit the fan, there were hundreds of trillions of dollars of notional dollars from derivatives piled on top of tens of trillions of cash assets, all short-term funded and with no capital to back them up. No firm could be confident in the ability of any other to honor its obligations. Moreover, each country had its own legal and bankruptcy code, so it was not clear how debts could be collected even if the borrowers could be identified and held accountable.

So, we can see that the 2008 financial crisis was largely the bastard child of Basel. The financial system in 2007 was like a forest stuffed with dry tinder. The sub-prime crisis was just the spark that set it all alight. Once Basel was enacted in 1988, an eventual crisis became highly likely, if not inevitable. Regulation established perverse incentives for the European banking industry, and US shadow banks happily piled on. Competitive pressure dictated that managers had to “dance” or risk being replaced. The response of these economic actors pursuing their own self-interest was entirely rational.

Secondary Causes of the Crisis

I will just touch on the secondary causes of the crisis, some of which receive insufficient attention.

The financial Institutions themselves. By placing the onus for the crisis on Basel, I don’t mean to let the private sector managements off the hook. Management was execrable in many cases and probably criminal in others. Still, it is important to appreciate that for the most part financial firms were trying to do the thing that firms do; maximize shareholder value within the parameters imposed by policymakers.

After all, the crisis didn’t happen all at once. Managements didn’t decide one day to bet the bank on PMBS and CDS’s. Rather, it was an Incremental process. Quarter by quarter, with no leverage constraint, they could always do a little bit more of what had worked previously to increase their earnings and hopefully their stock prices. The incremental risk was pretty much invisible to them, and, anyway, it had all been blessed by Basel. As Shin puts it,

“ . . . .greater lending by banks leads to further compression of spreads and other measures of risk, which induces banks to lend even more. So, Basel II made banks and the financial system much more procyclical and prone to booms and crashes.”

Or, to paraphrase Hyman Minsky, the so-called “Great Moderation” prior to 2007 was just a rubber band waiting to snap.

As years passed, managements gradually abdicated to the traders and the “quants” whose mathematical models supported the traders. While there were numerous warnings about risk levels, most managements felt they couldn’t afford to kill the golden goose. And anyway, it had all been blessed by Basel. This does not absolve management, but it does help explain how it all came about.

The ascendancy of the quants is a fascinating sidebar to the crisis. Basel I enshrined a risk model for bank trading books known as Value at Risk (VAR). For bank loan portfolios, Basel II followed up with the “Vasicek Model.” This is not the place to discuss these models in detail or the economic theories behind them. But let’s just say that as applied by Basel, these models were suspect. Oldrich Vasicek himself objected to how Basel applied his model. VAR had already been proven deficient in the collapse of Long Term Capital in 1998 and had been convincingly dismantled theoretically by such thinkers as Benoit Mandlebrot and Nassim Taleb. VAR is predicated on the assumption that market risk is “normally distributed” – like a bell curve. Mandlebrot and Taleb argued – rightly – that major downturns in most markets happen far more often, and are far more severe than can be explained by the normal distribution. This should have been common knowledge but was never factored in by the quants, perhaps because it didn’t suit their purposes.

Federal Housing policy, and in particular Fannie Mae and Freddie Mac (the GSE’s), have been singled out by a number of experts as the primary cause of the crisis. Peter Wallison lays out the argument clearly in his FCIC dissent and his book “Hidden in Plain Sight.” In a nutshell, he argues that quotas for GSE lending to low- and moderate-income borrowers steadily increased prior to the crisis, dumbing down systemic credit standards. Such GSE assets increased from 40% in 1995 to 58% in 2008. In 1999, 7% of Fannie’s loans to low or moderate incomes had loan-to-value ratios of 95% or above. In 2008, that number was 41%. I disagree that housing policy was the driving force behind the crisis, but it was certainly a major contributor.

The advent of the Euro opened the floodgates to Eurobank lending to the periphery. Throughout much of the early 2000s, loans to Greece, Italy, and the Baltics carried interest rates equal to or lower than those to Germany.

Basel II allowed banks to self-value not just their trading books, but their loan portfolios. It was promulgated in 2004 and not adopted by any Eurobanks until 2008. But key provisions had been well known for years so banks had already begun to game the system.

Rating agencies rubber-stamped ratings for Sub-Prime PMBS. In the end, though, the ratings turned out not to be so bad after all; AAA rated PMBS tranches suffered minimal losses. More problematical, actually, were the agencies’ knee jerk DOWNGRADES in the heat of the crisis…

Mark to market accounting accelerated the collapse of PMBS prices.

In the US, de novo banks could obtain new charters too easily prior to 2007. These banks were not sub-prime lenders as such but provided construction loans to build the product and provide incomes for sub-prime borrowers.

Some factors widely perceived as culprits actually had minimal impact:

Repeal of Glass Steagall (Gramm-Leach Bliley) was a non-factor. Mistakenly, many commentators single out Gramm Leach Bliley to “prove” that deregulation caused the crisis. This fiction underlies much of the “break up the banks” sentiment that is still prevalent in some circles. But even an economist as liberal as Alan Blinder recognizes that “the case that tearing down the Glass-Steagall walls was a major cause of the crisis is an urban myth. “

I reject the claim that US managements were “betting the bank,” intentionally at least. For one thing, management-owned huge holdings of their own stock. Also, prior to Bear Stearns, there was no reason for any creditor to believe that the government stood behind shadow banks.

This calls into question the significance of “Moral Hazard.” Moral Hazard is a real concern, it just wasn’t much of a factor in the crisis. Not for US financial institutions, at any rate. Except for the GSE’s, none of the shadow banks had government guarantees, either implicit or explicit. The commercial banks DID have such guarantees, but they weren’t the problem. Creditors to shadow banks thought their loans were “risk-free” not because of a government backstop, but because they were fully collateralized (Repo and ABCP.)

Part 3: Modern Regulation

“We Wuz Framed:” Railroading the Commercial Banks

Many buy into the myth that all or nearly all US banks needed bailouts during the crisis. This is a fantasy. In fact, unlike Europeans and US shadow banks, US commercial banks weathered the crisis impressively well. The industry suffered a loss in just one year – 2008. Depending on how you define it, the aggregate loss for the industry was between $10-$40 billion. This represented between 1 and 6 percent of their $650 billion in 2007 equity. In perspective, the industry simply gave back in 2008 some of what it had earned 2007. The total industry loss was less than what the government spent to bail out GM and Chrysler.

Yes, some commercial banks failed, but that is entirely to be expected, even welcomed, in a capitalist system. Yes, TARP was forced on the industry, but that was completely unnecessary. Yes, Citigroup, the perennial weak link, received an equity infusion, but Citi was certainly not insolvent. BankAmerica received an equity infusion too, but only after being allowed to buy a failing Countrywide and strong-armed into buying Merrill Lynch. Overall, the industry emerged from the crisis nearly as strong as when it started.

The principal reason for US banks’ strong showing was that their balance sheets were much stronger going in. Prudently, US regulators (notably the FDIC’s Sheila Bair) and managements had insisted on a leverage ratio far in excess of Basel minimums. While the leverage ratios for many universal European banks were 2% or below, the average for US banks was nearly 6%. Not only was this nearly triple that of many Europeans, it turned out to be far more than adequate to weather the crisis.

Even more crucially, US bank funding profiles were far superior to those of the Europeans. This made them far less vulnerable to runs. In 2007, Wells Fargo had $500 billion in assets and only $50 billion in what one might classify as “hot” funding. Compare this to UBS, with $2 trillion in assets and €1.2 trillion in “hot” funding (ex-derivatives!) Truth is, most US banks were not even in the same business as the European banks and shadow banks.

In light of US bank’s impressive performance, more onerous regulation was the last thing they, or the economy, needed. Yet that’s exactly what they got in Dodd-Frank.

Dodd-Frank was a flagrant over-reaction to a system that was badly bent but far from broke. Its intent was more to glorify its framers and be seen to punish the “banks” than it was an effort to fashion an effective regulatory framework. In spite of its length, much of Dodd-Frank is surprisingly vague. Most details were left to the agencies who were under pressure from policymakers to appear tough.

Just to be clear: no one believes that banks should be entirely unregulated. My belief, and I think the belief of most Americans, is that regulation is necessary, but that less regulation is almost always preferable to more. That’s not because we have blind faith in the free market to get the economy right. It’s just that we have a whole lot more faith in the free market than we have in the Washington bureaucracy.

Dodd-Frank: A Capital Crime

The regulatory reaction to the crisis imposed a heavy burden on the banking industry and stifled the ensuing economic recovery. It was the worst possible policy at worst possible time, stanching the flow of bank credit at a time when banks were already back on their heels. Moreover, its focus on commercial banks was misplaced; they had been victims of the crisis as much as they were perpetrators, and in many cases had worked with regulators to rescue troubled companies.

Several key provisions of Dodd-Frank and subsequent federal policy were especially misguided:

- Onerous and arbitrary capital standards

- Radical restructuring (in effect, nationalization) of the mortgage industry

- Adversarial “scorched earth” examinations

- Politically motivated lawsuits that removed capital when banks were under pressure to raise capital

- Stress tests that were arbitrary, opaque and erratic

If regulators had been more honest about their own role in creating the crisis, they might have been a little less smug about imposing “solutions.”

Let’s home in on one of the most destructive features of Dodd-Frank – capital requirements. In typically ad hoc fashion, Dodd-Frank alludes only vaguely to higher bank capital standards. It was left to the agencies to provide specific language. Of course, as we have discovered, capital adequacy was never an issue for US banks in the first place. But, gauging Congress’ temperament, the agencies were punitive, arbitrarily hiking capital requirements on all banks, especially the largest ones.

The pressure from Dodd-Frank to raise capital was compounded by Basel III. (If you liked Basel I and loved Basel II, you’ll be thrilled to learn about Basel III!) Given how its predecessors turned out, one can be forgiven for entertaining skepticism regarding Basel III. Where Basel I was marked by permissive leverage and Basel II was marked by the abdication of all bank supervision, Basel III features sheer, mind-numbing complexity. For just a taste of what I mean, read “Davis Polk Basel III Final Rule.” Then ask yourself who could think this stuff up and sincerely believe it could work in the real world.

Most academics, too, misunderstood the nature of the financial crisis. Believing the crisis to be more about solvency than liquidity, many have been afflicted by a “capital fetish”, convinced that no amount of capital is ever sufficient. The most visible among these academics are Anat Admati and Martin Hellwig. In their book “The Bankers New Clothes” they advocate leverage ratios as high as 30%.

In making this argument, they point out—correctly — that back before the turn of the century – the 19th, not the 20th, – bank capital ratios were much higher. In the 1800s these ratios were as high as 40-50%. However, they neglect to point out that such elevated capital levels never prevented bank panics, which occurred in the US nearly every decade prior to 1932. In fact, in 1930, just prior to the mother of all bank panics, bank capital stood at 12%, (Gorton 161) more than double that prevailing in 2007.

Moreover, they assert that bank capital is cost-free to banks and to society. That is, they claim that the stock market will happily trade-off less risk (more capital) for lower returns (lower return on equity.) So, the market is just as happy with a bank that has 20% capital and a 4% ROE as it is with one boasting 5% capital and a 15% ROE. Not only does this seem to reflect a quaint allegiance to the thoroughly discredited Capital Asset Pricing Model, it almost makes one question whether they have ever actually considered owning a bank stock.

In fact, it is just common sense that compelling banks to hold excessive capital must impose a cost on both banks and society. It is simply a question of opportunity costs. Such draconian standards misallocate society’s precious capital, and we all pay the price.

The US banking industry today has $15 trillion in assets and roughly $1.4 trillion in equity — a 9% leverage ratio, give or take. If the industry is being compelled to hold 9% but only needs 6% — $900 billion. – then $500 billion in society’s capital is being squandered. The cost is uncertain, but at an 8-12% Cost of Capital, that’s a $40-70B annual deadweight social loss.

This cost is not just hypothetical. In practice, there are two ways for a bank to increase its leverage ratio. It can increase its equity, or it can reduce its assets. Post-crisis, US banks did both. Between 2010 – 2015 total assets of the 5 largest US banks actually shrank. Applauded by policymakers, this trend is hardly consistent with robust economic growth.

Let’s get some historical perspective to estimate the cost of incenting banks not to lend. The previous bank crisis (far less severe than 2008) was in 1991. Prior to 1991, total commercial bank loans peaked at $2.9 trillion. Loans reached their nadir in 1992 at $2.6 trillion. In the 8 subsequent years of recovery through 2000, loans grew to $4.6 trillion, a 7.2% compound growth rate. The economy grew 3.7% per year in that stretch.

In comparison, loans peaked in 2007 at $7.8 trillion, bottoming out at $7.1 trillion in 2009. In 8 years of recovery through 2017, loans grew to $9.6 trillion, a compound growth rate of just 3.9%. This is especially surprising because the 2008 crisis was so much more severe than 1991. The slower rate of loan growth Implies a lending “shortfall” of $340 billion annually or $2.7 trillion cumulatively over 8 years.

Of course, the really important question is, “What was the impact on the economy of this regulatorily suppressed loan growth?” Now one would think a quick call to the local economist would provide an answer to this question. Unfortunately, I have been unable to scrounge any study that deals with this issue. So, I’ll begin the debate with my own heuristic:

Historically, $2 in nominal GDP growth has been associated with $1 in commercial loan growth. This relationship has been surprisingly consistent, ranging from a high of 2.5 in 1993 to a low of 1.8 in 1986. Even at the low end, this implies a hit to nominal GDP over the last 8 years of $4.9 trillion ($2.7 x 1.8), or roughly $600 billion annually. Maybe this is too high, but even a quarter of that is $150 billion annually. Not quite 1% of GDP, but close enough for government work. I am convinced that this is the main reason why GDP growth from 2009 – 2017 was a measly 2.0% annually, only a bit more than half of the 3.7% achieved from 1991 to 1999. If these numbers are in the ballpark, then it is possible that regulatory repression post-crisis cost the economy nearly as much as the crisis itself.

Onerous capital requirements and adversarial examinations were by no means the only regulatory impediments to bank lending in the years following the crisis. In his book “Floored,” George Selgin details how a 2008 decision by the Fed to pay interest on bank reserves allowed banks to profitably hold excess reserves instead of lending them out. Given the toxic post-crisis regulatory world, this was an easy decision for banks. Thus, the Fed’s efforts to stimulate the economy through quantitative easing were seriously inhibited.

A superb 2017 study by the Urban Institute corroborates the argument that regulation artificially suppressed loan availability. In “Quantifying the Tightness of Mortgage Credit and Assessing Policy Options,” economist Laurie Goodman asks why the growth in single-family mortgages from 2009 — 2015 was so much slower than one would have expected. To find the answer, she compares actual mortgage production to what it would have been had the industry adhered to credit standards prevalent in 2001-2002, prior to sub-prime excesses.

Goodman finds that between 2009 and 2015, 6.3 million fewer mortgages were made than would have been made under 2001-2002 credit standards. At $150k a pop, that’s $945 billion in foregone mortgages – more than a trillion dollars in foregone home sales. Worse, average FICO scores rose to 700 from 660 in 2001-2, indicating that low-income borrowers were disproportionately denied mortgages. This exacerbated US economic inequality.

Goodman does not explicitly blame Dodd-Frank for these shortfalls, but several rules stemming from Dodd-Frank help to account for it. Most important was the “put back rule.” This rule allows the GSE’s to “put back” to a mortgage originator any loan that went bad if the GSE could find a flaw in the application. Of course, if you’ve ever taken out a mortgage, you know that the applications can be riddled with small errors, any one of which could result in the mortgage being returned to the originator. Understandably, mortgage lenders stopped approving any mortgage that was close to borderline in quality, and most banks abandoned the business.

Two further contributors were that 1. post-crisis, mortgages requiring down payments of less than 20% were scarce and 2. Banks were compelled to deduct from capital the value of their mortgage servicing intangible.

So, I’ve argued that the capital burden for banks post-crisis has been excessive. This raises the question: What IS the optimal amount of capital for a bank?

Most commentators totally wimp out on this issue. Noncommittal pabulum like this is typical: “Managing bank capital is more art than science. In light of the crisis, we should err on the side of conservatism and maintain capital at levels as high as possible.”

Well, excuse me, but that’s just wrong. The crisis was nothing if not an unprecedented real-world experiment that told us, with some precision, just how much capital banks require under some rather extreme conditions. Thanks to bonehead Basel, we now know that 1-2% tangible equity ratios are not adequate. (No surprise there.) Ratios of 4-5% may be sufficient for some low-risk institutions but are probably too low for a systemic standard. But given the pre-existing regulatory regime, ratios in the 6% range were more than adequate for US banks to endure the worst financial catastrophe in 70 years and emerge nearly unscathed.

Part 4: Policy Recommendations

For US policymakers, there are three key lessons to be drawn from the 2008 financial crisis:

- The crisis was caused by BAD regulation of Eurobanks and shadow banks.

- With all its flaws, the US commercial bank regulatory structure proved to be robust, ex-ante.

- The response of US financial regulators – Bernanke, Geithner, Paulsen – was massive, scattershot, unilateral, unfair, unorthodox, ad hoc, often flawed, and only borderline legal. But luckily for us, they threw everything against the wall and enough of it stuck to save the US and European economies from total collapse.

Unconscionably, most of us – notably our legislators – have failed to fully absorb this last lesson. The failure to do so could prove catastrophic. I have many thoughts about ways to improve our financial regulatory structure, but one stands out as imperative: rescind Title XI of Dodd Frank.

In its zeal to be seen as tough on “bailouts”, Congress included in Dodd-Frank “Title XI.” Title XI was intended to revise Fed section 13-3, which was used during the crisis as a pretext for huge and varied Fed support for banks, shadow banks, and European banks. In place of the flexibility enjoyed (?) by Bernanke et al, Title XI enacts rigid guidelines for the “orderly liquidation” of SIFI’s (Systemically Important Financial Institutions.) Most dangerously, it prohibits the Fed from lending directly to any institution that is “insolvent.” (We know what a fraught concept solvency is.)

Under Title XI, observes Lawrence Ball, “any lending program <by the Fed> must be designed for a substantial number of firms, not just one . . . . and all lending must be approved by the Secretary of the Treasury. Under these rules, future Fed leaders may be helpless to counter runs on financial institutions and prevent unnecessary financial disasters. . . . .Going forward, even if the Fed’s leaders are determined to resist political pressures, their actions to preserve financial stability may be vetoed by Treasury Secretaries motivated by politics.”

For most of us, the 2008 crisis struck without warning, with greater severity than anyone could have imagined and for reasons that few foresaw. Can anyone doubt that the next financial crisis – and there will be one – will similarly sweep in out of left field? Suppose we wake up tomorrow and a computer hacker has zeroed out all of Citigroup’s accounts. Do you think it is wise to prohibit the Fed from backstopping Citi? Under such conditions, who’s to say if Citi is solvent or not? If it is insolvent, so are a huge number of counterparty institutions. And remember, any decision to fund Citi cannot wait until the next day; it must be made immediately.

Every day trillions of dollars in “daylight overdrafts” –customer payments in the process of settlement – work their way through the banking system. That these payments routinely prove out at the end of the day is borderline miraculous. Yet there could be – and have been – “black swan” events that interrupt this process. If this happened, a bank, or many banks, would require significant funding at the end of the day, and some could be technically insolvent. We do not want Title XI to turn an operational glitch into a financial panic.

The point is that we were lucky in the last crisis to have folks in charge who used every resource and bent every rule to get us out of the mess we had dug ourselves into. To severely restrict options for the next set of crisis managers is the folly of the worst sort.

Title XI is only the most urgent of Dodd Frank’s provisions that require revision. As is expressed above, with few exceptions, the entire Dodd Frank / Basel III regulatory framework has been a failure and should be scrapped.

Many regulators and academics will take issue with this conclusion. They will contend that Dodd Frank has been a resounding success because no large banks have required bailouts since it was enacted, and the banking system is “safer” than it used to be. Even if this is true, it has come at an economic cost of hundreds of billions, if not trillions of dollars, if my numbers are anywhere close to valid.

Think of it this way: Say there’s an airport with a runway two miles long, more than sufficient for any plane. One day, little Jimmy loses control of his big drone and crashes it on the runway. As planes land, they struggle to avoid the wreck. Some swerve off the runway, some run off the end of the runway, but all land safely.

Concerned, the FAA decides that the airport can be made safer if it spends $500 million dollars to add another 2 miles to the runway. Later, seeking to eliminate even the remotest chance for a crash, the FAA says, “We’ve conducted a very sophisticated stress test and we’ve concluded that if four drones crash simultaneously, you would need six more runway miles.” Done, at a cost of $1.5 billion. So yes, maybe the airport is marginally safer, but $2 billion has been wasted and the real problem has not been addressed: Jimmy’s got his pilot’s license.

Let’s not kid ourselves; Dodd Frank represented a de facto, back door nationalization of our banking industry. No, the government does not own bank shares. But it has intruded into nearly every aspect of bank management. Few significant management decisions are not contingent- implicitly or explicitly – on regulatory say so. For the mortgage business, this nationalization has been explicit. (See “Comradely Capitalism” in the Economist, August 30, 2016.)

Some may applaud these trends, but I believe that they are dangerous for reasons that reduce to one word – incentives. There is a perception that regulation automatically puts folks in charge who have the public’s best interests at heart. I’m skeptical. I believe it’s more likely that when shareholders cede authority to regulators, power simply shifts from one self-interested constituency to another. Whereas shareholders are focused on taking measured risks to maximize stock value, regulators are primarily concerned with eliminating all risk to keep their jobs. Recently, their method in this endeavor has been to throw enough obstacles in the way to prevent banks from ever taking risk and making money.

In case you think I’m exaggerating, consider the following quote from an economist representing the “Basel” viewpoint at a Nov. 17, 2015 Brookings Institution conference. “The whole point … is to drive ROE’s down into the realm where you have safer institutions.” Now THAT is the regulatory perspective full stop.

Moreover, while private sector management can be, and often is, removed if proven ineffective, regulators need to commit a truly heinous act to be dismissed. However talented and committed a regulator may be, there is simply no upside in allowing risks to be taken. And a capitalist economy cannot function effectively if its banks are precluded from taking risk.

As I emphasized above, the consequences of this regulatory burden are plainly visible in the last decade’s glacial economic growth and rising inequality. It is past time to shift control of the banking industry back to its owners and managers.

So, the question arises: if not Dodd Frank, then what?

I wish I could offer a visionary plan that anticipated and solved all the future problems that the industry might face. But alas I’m not a visionary. In fact, I’m suspicious of grand plans. I believe that our knowledge is profoundly limited, especially our knowledge of the future. As Keynes observed, we inhabit a world of “radical uncertainty.” Actions taken today are likely to be rife with unintended consequences and, sadly, the bad consequences usually seem to outweigh the good ones. Our experience with Basel and Dodd Frank, properly understood, should give us pause about our ability to anticipate and effectively shape the future.

In fact, we must accept that we will never fashion the “perfect” regulatory structure. Instead, we should take a more practical approach. We should concentrate on what we know has worked in the past and build on that. And one thing we know for sure is that the commercial bank regulatory framework that predated the crisis worked nicely.

As we begin our effort to design a post-Dodd Frank regulatory structure, let’s start with the regulator’s prime directive.

Ask a bank regulator today about his top priorities and, if he is honest, he will say:

“My top priorities are to ensure that no bank in my jurisdiction ever needs a “bailout,” and that neither I nor my superiors are ever publicly flayed in front of a congressional banking committee.”

From a regulatory standpoint, those objectives are understandable, if not laudable. But I’m not sure they are the values we need to drive a vibrant economy.

Instead, let me propose an alternative prime directive:

The bank regulator’s first priority should be to establish the incentives that encourage the best managers to enter the industry and pursue the best practices once they get there.

Treating bank managers as incompetent at best and incipient criminals at worst is not the best strategy for achieving this end.

The strength of the banking industry lies not in capital ratios, or stress tests, or scorched earth examinations, but in management. Regulatory micromanagement does not make the industry stronger, but weaker. By focusing management time and resources inward on busy work like living wills and stress tests, the industry becomes less able to respond creatively to new challenges. Fostering flexibility, adaptability and experimentation will ultimately build a stronger banking system than simply keeping management trapped in a regulatory straitjacket.

A better framework would be to move away from today’s Rube Goldberg meets Alice in Wonderland regulatory world toward an environment of simplicity and clarity. I believe that it is best to eschew micromanagement and instead establish broad guidelines that allow managements – and the free market – considerable operating latitude.

In his trenchant (and entertaining) 2012 essay “The Dog and the Frisbee,” Andy Haldane, Chief Economist at the Bank of England, made a compelling case that when it comes to regulation, simpler is better:

“. . . . . the more complex the environment, the greater the perils of complex control. The optimal response to a complex environment is . . . . . to simplify and streamline . . . . In complex environments, decision rules based on one, or a few, good reasons can trump sophisticated alternatives. Less maybe more. “

And,

“Complex rules may cause people to manage to the rules, for fear of falling foul of them. They may induce people to act defensively, focusing on the small print at the expense of the bigger picture. “

These ideas dovetail with those of Nassim Taleb, who is an advocate of what he calls “antifragility”: striving to fashion systems that get stronger as volatility (external stress) increases. Now, Taleb is one of the more curmudgeonly and infuriating thinkers one will ever encounter. He is never in doubt. But unlike most policymakers and conformist economists who are never in doubt but usually wrong, Taleb is usually right.

To create, or at least head in the direction of, an antifragile banking system, we need to promote rules that are sufficiently flexible to allow banks to pursue their own strategies and succeed or fail in small increments in the hope of avoiding a large systemic risk event. To do this, we must junk the current adversarial regime that strives to preclude change at all costs and instead embrace change and “randomness.” In the words of Denis Noble, we need to learn how to “harness stochasticity.”

We should also try to give banks “skin in the game.” That is, we should try to create incentives that give individual banks an interest in building a robust systemic banking structure. We must accept that if we are to embrace change, it will be extremely difficult for regulators to stay ahead of the game. So, the banks themselves will need to pick up much of the slack.

To accomplish this, we first need to relax the byzantine capital rules for US banks. As demonstrated above, today’s near double digit leverage ratios are far in excess of what they need to be. We should allow banks to gradually return to pre-2007 capital levels which were clearly sufficient. Allow the private sector, not government, to decide what to do with the freed-up capital (with the important exception noted below.) Of course, if capital standards are lowered, it must be done with care. Rigorous examinations need to be an essential component of any large-scale capital reduction.

Next, we need to restructure the FDIC. Not surprisingly, few Americans understand how the FDIC operates. It is not a taxpayer financed reserve fund for bank bailouts. In actuality, it has always been a self-insurance fund financed by premiums from banks. Today, it is run by career FDIC employees and a few political appointees. It has long been responsible for monitoring banks and resolving those that fail. With Dodd Frank, it was assigned the additional task of managing the “orderly liquidation” of institutions deemed insolvent.

I propose to make the FDIC’s self-insurance function explicit by converting the agency into a special purpose private corporation owned by the banks themselves. It would have a board of directors consisting of bankers, regulators, and industry leaders. OCC operations would be folded into the FDIC. The banks themselves would receive a return on funds invested and benefit from lower than expected loss development. Of course, they would also incur pro-rata losses in times of negative development. There would be no more confusion over who was funding “bailouts.” It would be banks, not taxpayers. This would give them an incentive to keep the FDIC well-staffed (clearly, there would also be legislative mandates), share information, and carefully monitor the behavior of all FDIC members.

Importantly, measures must be taken to ensure that small banks are represented at least in proportion to big banks. While the industry trend is clearly in the direction of consolidation, the US endowment of small banks is a unique and invaluable feature of our financial system. It is crucial to the health of our vibrant small business sector.

A key feature of the transition to a public/private FDIC would be an actuarial study to determine the amount of reserves necessary for the fund. Then, before banks are allowed to reduce capital levels, there would be a one-time assessment to get the FDIC’s reserves up to the actuarial minimum (plus, presumably, some additional cushion.)

Hopefully, one benefit of this proposed structure will be that any resolutions are conducted with an eye to minimizing financial losses. Specifically, the FDIC might become more measured in its disposition of the assets it obtains from troubled banks. In the past, aggressive FDIC asset sales have pressured real estate prices in many markets at times when those markets were already severely distressed. Not only did this behavior mean that FDIC losses were greater than they needed to be, it also complicated workouts of troubled loans at surviving banks. In the future, perhaps the FDIC might be willing to hold these assets in portfolio and wait to sell into improving markets.

One complication to this proposal is that today the FDIC regulates only banks, not bank holding companies. This would have to change. In the short term, at least, the Fed, once relieved of its Dodd Frank lending limitations, would continue to monitor bank holding companies and serve as an unfettered lender of last resort. I’m convinced that duplication of regulatory effort, while arguably inefficient, provides effective checks and balances. Also, I believe that (as per Bagehot) loans from the Fed should be expensive so such borrowing is a last resort. TARP was unnecessary, but it was also too cheap.

I anticipate that this proposal for some will raise the specter of “regulatory capture.” Regulatory capture has traditionally meant that a regulator identifies too closely with the entity being regulated, compromising supervisory objectives. More recently, this term is applied to any regulator not seen as tough enough on banks.

In fact, what some call “regulatory capture” has always been a great strength of US bank regulation. Historically, bank – regulator relations have been, if not exactly collegial, at least non-adversarial. Banks were always careful to stay on good terms with regulators. That’s just good business. And examiners, in turn, tried to stay on good terms with the banks. Examiners were often hired by banks into their credit and compliance departments. Ex-examiners became some of the industry’s best credit people and more than a few CEO’s. These folks inculcated regulatory values into the industry while private sector opportunities kept examiners from acting capriciously.

To my knowledge, bank relationships never prevented regulators from acting when necessary, whether in 2008, Texas in the 1980’s or Bank of New England in the 1990 – 1992 recession. Again, the old system worked far better than the standard narrative allows.

It is no coincidence that my proposal might seem reminiscent of “clearing houses,” which were the de facto regulatory authority prior to the Federal Reserve Act of 1919. Clearing houses were consortiums of banks that banded together to clear payments. In a liquidity crunch, as in the panic of 1907, the clearinghouse banks cooperated in support of weaker members while sorting through them to determine who was really solvent. In the meantime, they issued “clearinghouse certificates” as payment to customers if cash (or specie) was not available. All of the banks stood behind these certificates.

“The clearinghouse response to panics was exactly the opposite of the view that it is important to “mark-to-market” the assets of the banking system. The clearinghouse decisively recognized that the assets could not be sold and that such “marking” was meaningless.”

Gary Gorton

I am under no illusions that my proposals will be the last word on regulatory reform. Nor would I want them to be. Hopefully, they are just the start of the discussion. For now, let’s admit that we were all wrong about the financial crisis and the lessons we drew from it. Then let’s do something Dodd-Frank never did. Lets’ have an honest, evidence-based, unbiased discussion about how to achieve truly effective financial regulation.

“I may be wrong and you may be right, and by an effort, we may get nearer to the truth.”

Karl Popper

About the Author: Charles Cranmer

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.