Investor-Stock Decoupling in Mutual Funds

- Miguel A. Ferreira, Massimo Massa, Pedro Matos

- Management Science, forthcoming

- A version of this paper can be found here.

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions

To fully comprehend this paper it’s necessary to get familiar with terms they utilize, “investor-stock distance (ISD)” and “decoupled Investors.” In this context of this paper “investor-stock distance ” is represented by geographic proximity to the underlying securities of a mutual fund. So, Suzie Q. buying a mutual fund with US stocks as the underlying has a closer “investor-stock distance” than a French person purchasing a mutual fund that owns US-based stocks. The French person buying the mutual fund with US Stocks as the underlying would be deemed a “decoupled investor.” This article compares two hypotheses. The first hypothesis posits that closer investor–stock distance is a source of competitive advantage: The idea is that funds with “decoupled” investors—i.e., the ones with a negative or low correlation between investor flows and portfolio stock returns—will have a natural hedge, experiencing fewer redemptions in market downturns and fewer inflows in upturns. The alternative hypothesis is that investor–stock distance is a source of competitive disadvantage. One rationale for that is that investors are closer to the action and are more apt to trade frequently. (see our piece on “Limits of Arbitrage”)

The authors test these hypotheses on the role of investor–stock distance using data on a large sample of equity mutual funds domiciled in 26 countries over the period from 1997 to 2010. The sample includes funds investing in domestic, foreign, regional, and global stocks and covers the large majority of actively managed funds worldwide.

There are two main variables under analysis:

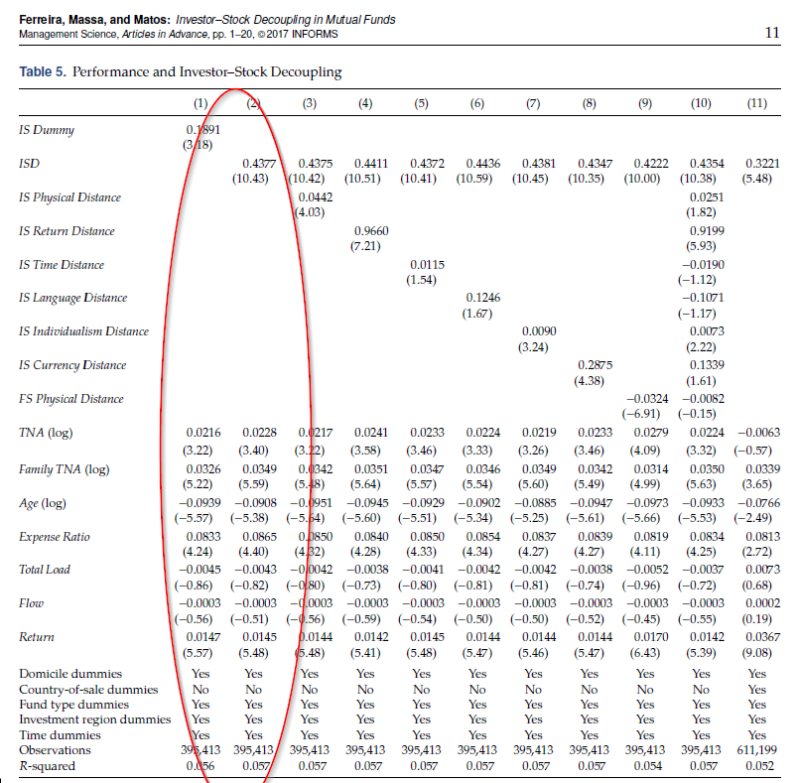

- A proxy of investor–stock decoupling, which is a dummy variable that takes a value of one if the fund is sold to investors that are not located in the same country as the stocks in which the fund invests (IS Dummy).

- A proxy of investor–stock decoupling capturing how flows react to shocks to the stock markets in which the fund invests. It captures the sensitivity versus the stickiness of fund flows. More specifically, it consists of the negative of the correlatio between the aggregate fund flows of funds in the countries where the fund is registered for sale and the stock market returns of the countries in which the fund invests (ISD Dummy)

What are the Academic Insights?

The authors find:

- Having foreign investors is good for your fund. In line with the decoupling hypothesis, there is a negative association between a fund’s ISD and the slope of the flow– performance relationship. Additionally, there is lower sensitivity of flows to bad performance (i.e., decoupled investors tolerate better losses) and a lower sensitivity of flows to good performance (i.e., decoupled investors do not chase winners as aggressively).

- There is a positive and significant association between fund ISD and fund performance. A one standard deviation increase in ISD is associated with a 17 basis point (per quarter) improvement in four-factor alpha. Moreover, the authors show that the positive impact on fund performance is stronger in periods of market stress. The authors provide evidence that decoupled funds have a competitive advantage especially when the market return is weak, when market volatility spikes, and during the 2007–2008 financial crisis.

- There is also a negative association between ISD and risk-taking as well as fund managers with decoupled investors deviate more from their benchmarks using the Amihud and Goyenko (2013)’s R-squared measure

- Finally, for a sample of funds for which they have detailed portfolio holdings, the authors perform additional tests and find that funds with high ISD invest more in small and illiquid stocks.

The authors perform a series of robustness tests. For example, they control for the distance between the location of the fund manager and the location of the assets (fund–stock physical distance) as well as the distance between investors and the location of the assets (investor–stock physical distance) and include domicile and country-of-sale fixed effects that control for unobserved sources of time-invariant heterogeneity (e.g., the regulatory environment). They also control for proxies of behavioral/cultural distance between investors and investment portfolios in terms of time zone, language, and culture since investors may overweight stocks with which they are more familiar.

Why does it matter?

This study examines whether mutual fund behavior is affected by the behavior of investor flows from the markets in which the fund sells its shares. Funds characterized by a higher investor–stock decoupling experience a competitive advantage, in particular during periods of asset fire sales. Specifically, the higher the degree of decoupling, the more a fund is shielded from withdrawals during bad times, allowing the fund manager to engage in more active management, invest in more illiquid assets, and deliver higher performance.

In other words, diversifying funding sources internationally can have a positive impact on mutual fund performance.

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

We investigate whether mutual funds whose investors and stocks are decoupled (i.e., investor location does not coincide with that of the stock holdings) benefit from a natural hedge as they have fewer outflows during market downturns and fewer inflows during upturns. Using a sample of equity mutual funds from 26 countries, we find that funds with higher investor–stock decoupling exhibit higher performance, and this is more pronounced during the 2007–2008 financial crisis. We also find that decoupling allows fund managers to take less risk, be more active, and tilt their portfolios toward smaller and less liquid stocks.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.