In this article, we examine the research on investing during inflationary regimes such as deflation, inflation, and stagflation. Factors perform relatively well in all regimes on a real basis.

Investing in Deflation, Inflation, and Stagflation Regimes

- Baltussen, Swinkels and Pim van Vliet

- Working paper, 2022

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Spikes in inflation and fear of stagflation prompted this study which answers the following question:

1. How do risk premiums and investment strategies behave across inflationary regimes like periods of high inflation, deflation, or stagflation?

What are the Academic Insights?

By utilizing the deepest sample available for a relatively broad cross-section of asset class and factor portfolio starting in 1875 (147 years sample) and by analyzing four different regimes (1) below 0%, or deflation, (2) between 0% and the current central bank target of 2%, (3) a mild inflation overshoot, between 2% and 4%, and (4) high inflation, above 4%, the authors find the following:

1. The global equity return has been, on average, 8.4% (in arithmetic terms) between 1875 and 2021, while the global bond market return (currency risk hedged) has been 4.5%. In comparison, global inflation has been on average 3.2% per annum over the same period. Value, Momentum, Low risk or Quality/Carry factors also returned attractive and significant returns above 4%, with the average multi-factor combination delivering significant alphas on top of asset returns with t-values above 7.9 over this full sample period.

2. Equity, bonds, and global factor premiums are generally consistently positive across inflationary regimes, generally displaying no significant variation across. At the same time, they enhance nominal and real asset class returns in (approximated) long-only asset class implementations. Further, equity returns tend to be relatively low in nominal terms in periods of deflation but average in real terms. Equities and bonds on average yield lower nominal returns during periods of high inflation, causing negative real returns. These results are robust across different definitions of inflationary regimes, including a 3% or 5% (instead of 4%) high inflation cutoff, the use of annual changes in inflation (or unexpected inflation), the use of only U.S. (instead of global) inflation, or the use of 3-years (instead of 1-year) horizons

3. Periods of stagflation are truly bad times. For example, nominal equity returns average -7.1% per annum, yielding double-digit negative returns in real terms. During the bad times, equity, bond, and global factor premiums remain consistently positive. As such, factors help to offset some, but not all, of the negative impact of high inflation in recessionary times

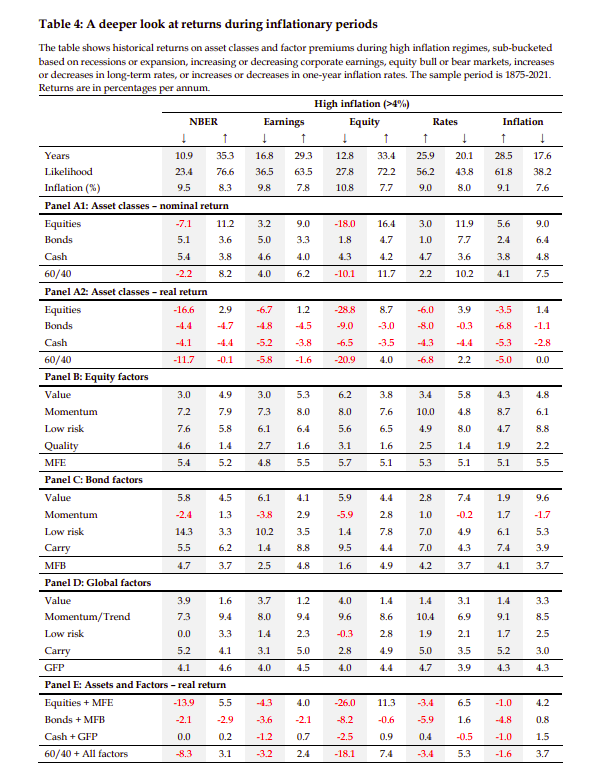

The authors further study the terrible times and analyze the following sub-regimes: (1) recession or

expansion, (2) falling or rising earnings growth, (3) bear or bull equity markets, and (4) increasing

or decreasing interest rates, and (5) increasing or decreasing inflation. The findings are summarized in Table 4 below.

Why does it matter?

First, for investors, times of high inflation (and especially stagflation and inflationary) bear markets are challenging, which suggests asset class returns may partly provide compensation for bearing risks during these bad times.

Second, as equity, bond, and global factor premiums are generally consistent across inflationary regimes, they provide consistent value add for traditional portfolios. These premiums provide diversification but, at the same time, are also not a perfect hedge against inflation, as their returns do not substantially increase during the worst times.

Finally, our results suggest factor premiums in equities, bonds, and across asset classes are not compensation for bearing inflationary risks.

The Most Important Chart from the Paper:

Abstract

We examine asset class and factor premiums across inflationary regimes. As periods of high inflation and deflation are relatively uncommon in recent history, we use a deep sample starting in 1875. Moderate inflation scenarios provide the highest returns across asset class and factor premiums. During deflationary periods, nominal returns are low, but real returns are attractive. By contrast, real equity and bond returns are negative during a high inflation regime, and especially so during times of stagflation. During these ‘bad times’ factor premiums are positive, which helps to offset part of the real capital losses.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.