The Quality Factor—What Exactly Is It?

By Larry Swedroe|January 28th, 2021|Quality Investing, Factor Investing, Research Insights, Larry Swedroe, Value Investing Research|

The existence of a quality premium in stocks that has [...]

A Review of Ben Graham’s Famous Value Investing Strategy: “Net-Nets”

By Gaurang Merani, CPA|January 26th, 2021|Factor Investing, Research Insights, Guest Posts, Academic Research Insight, Value Investing Research|

Benjamin Graham, often considered a strong candidate for "the father [...]

Mutual fund investments in private firms

By Tommi Johnsen, PhD|January 25th, 2021|Private Equity, Research Insights, Basilico and Johnsen, Academic Research Insight, Active and Passive Investing|

Mutual fund investments in private firms Sungjoung Kwon, Michelle Lowry, [...]

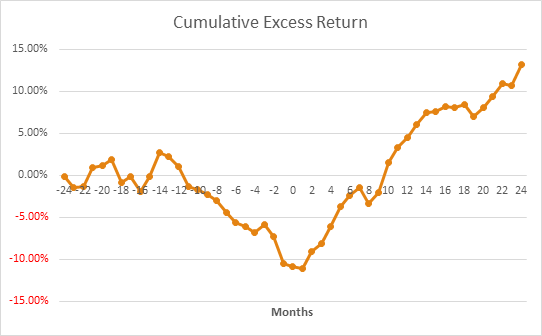

Is the Market Getting more Efficient?

By Larry Swedroe|January 22nd, 2021|Research Insights, Factor Investing, Larry Swedroe, Academic Research Insight, Active and Passive Investing|

Another Alpha Opportunity Bites the Dust In 1998, Charles Ellis [...]

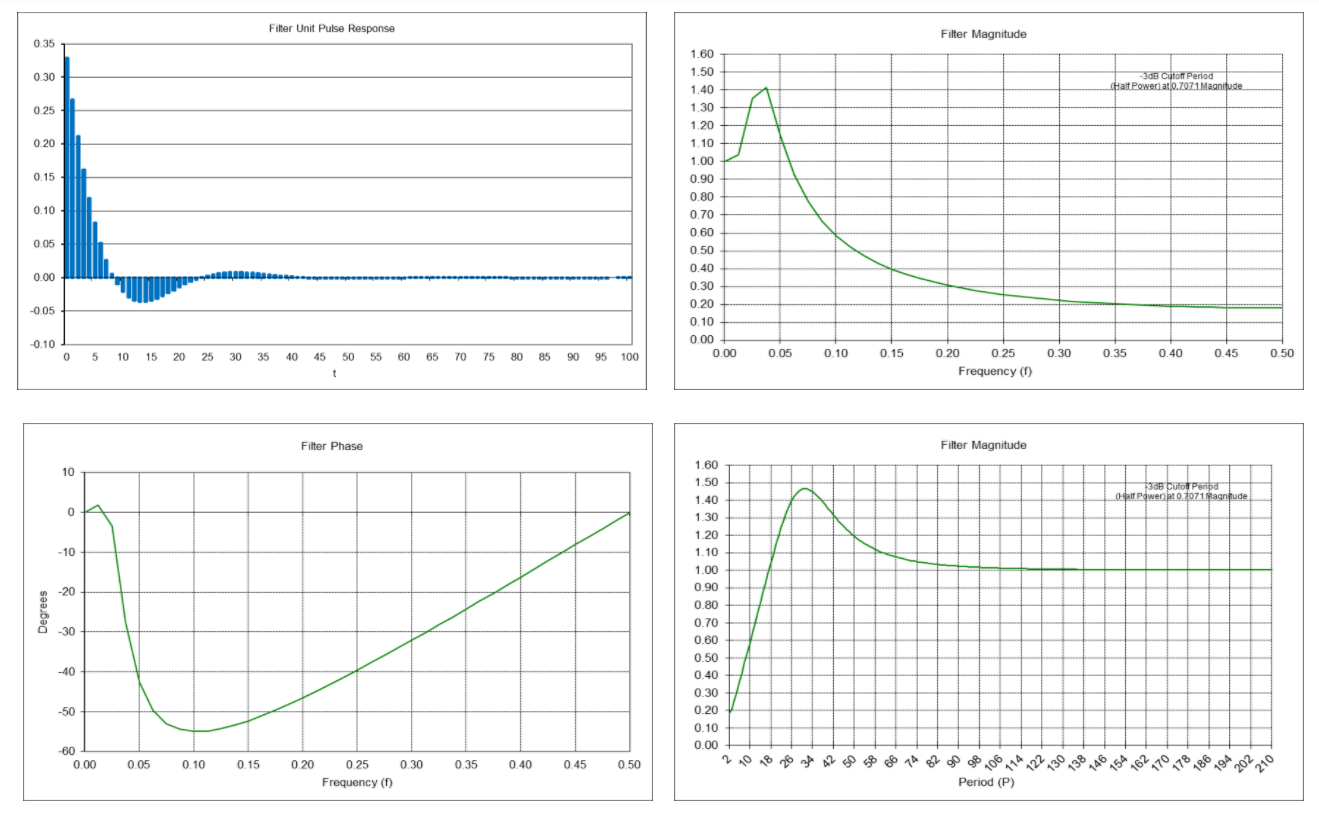

Trend-Following Filters – Part 2/2

By Henry Stern|January 21st, 2021|Factor Investing, Research Insights, Trend Following|

1. Introduction Part 1 of this analysis, which is available [...]

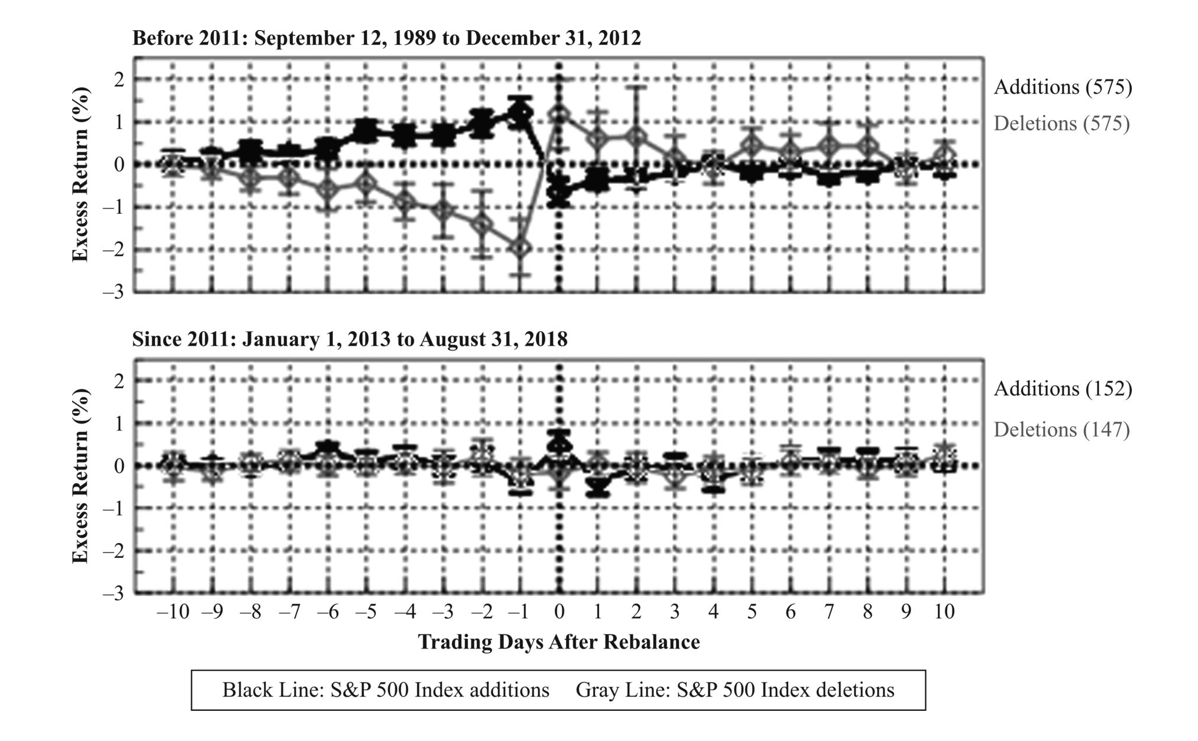

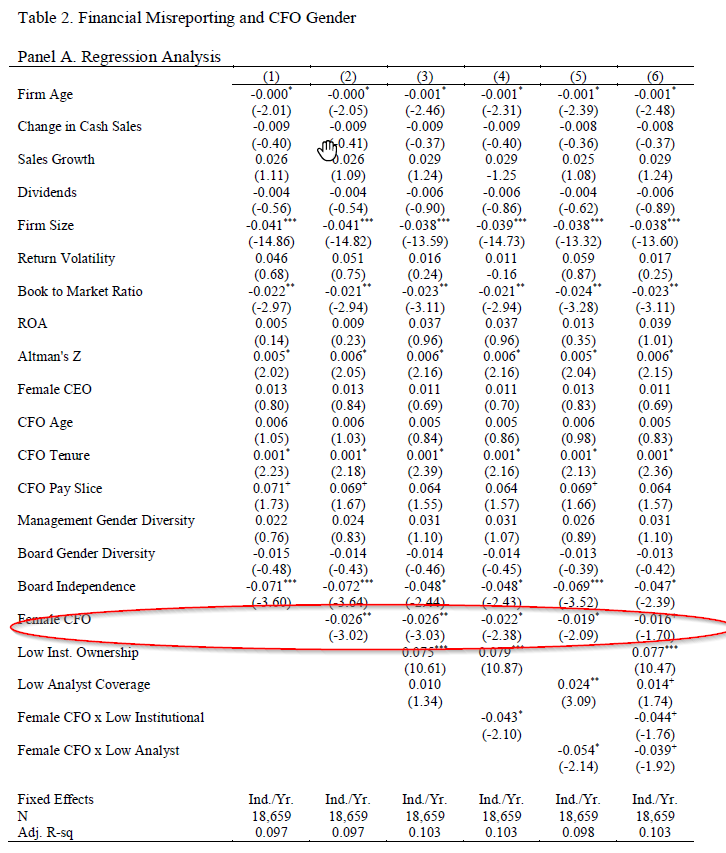

Battle of the Sexes, Who’s Better at Fudging the Numbers?

By Wesley Gray, PhD|January 19th, 2021|Women in Finance Know Stuff, Research Insights, Basilico and Johnsen, Investment Advisor Education, Academic Research Insight, AI and Machine Learning|

CFO Gender and Financial Statement Irregularities V.K.Gupta, S. Mortal, B. [...]

Global Factor Performance: January 2021

By Wesley Gray, PhD|January 12th, 2021|Index Updates, Factor Investing, Research Insights, Tool Updates, Tactical Asset Allocation Research|

The following factor performance modules have been updated on our Index [...]

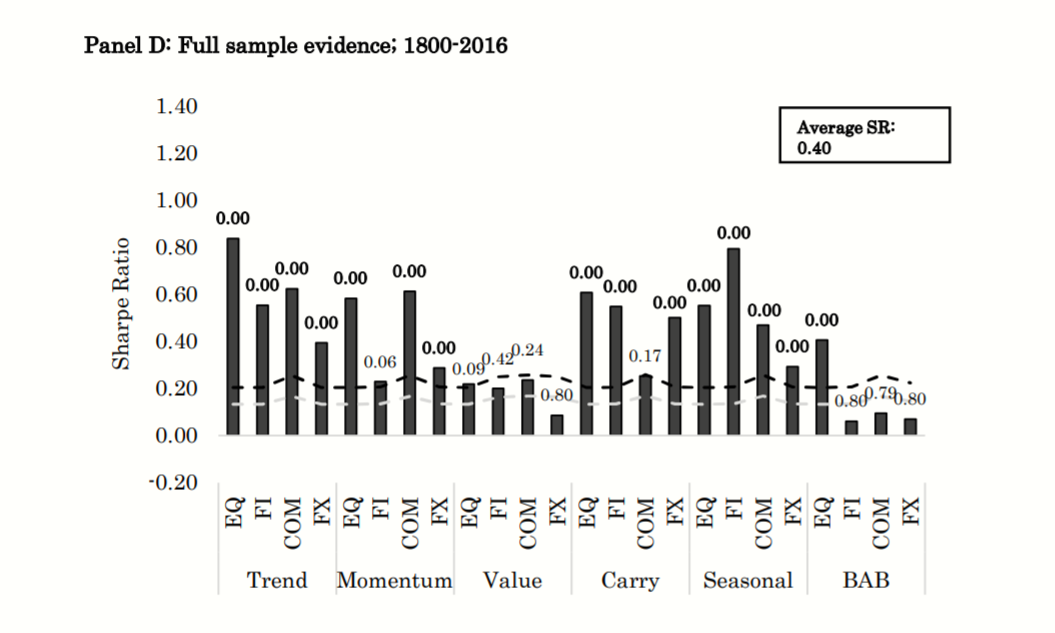

The Definitive Study on Long-Term Factor Investing Returns

By Wesley Gray, PhD|January 12th, 2021|Factor Investing, Research Insights, Academic Research Insight|

Global Factor Premiums Baltussen, Swinkels, VlietJournal of Financial Economics, forthcomingA [...]

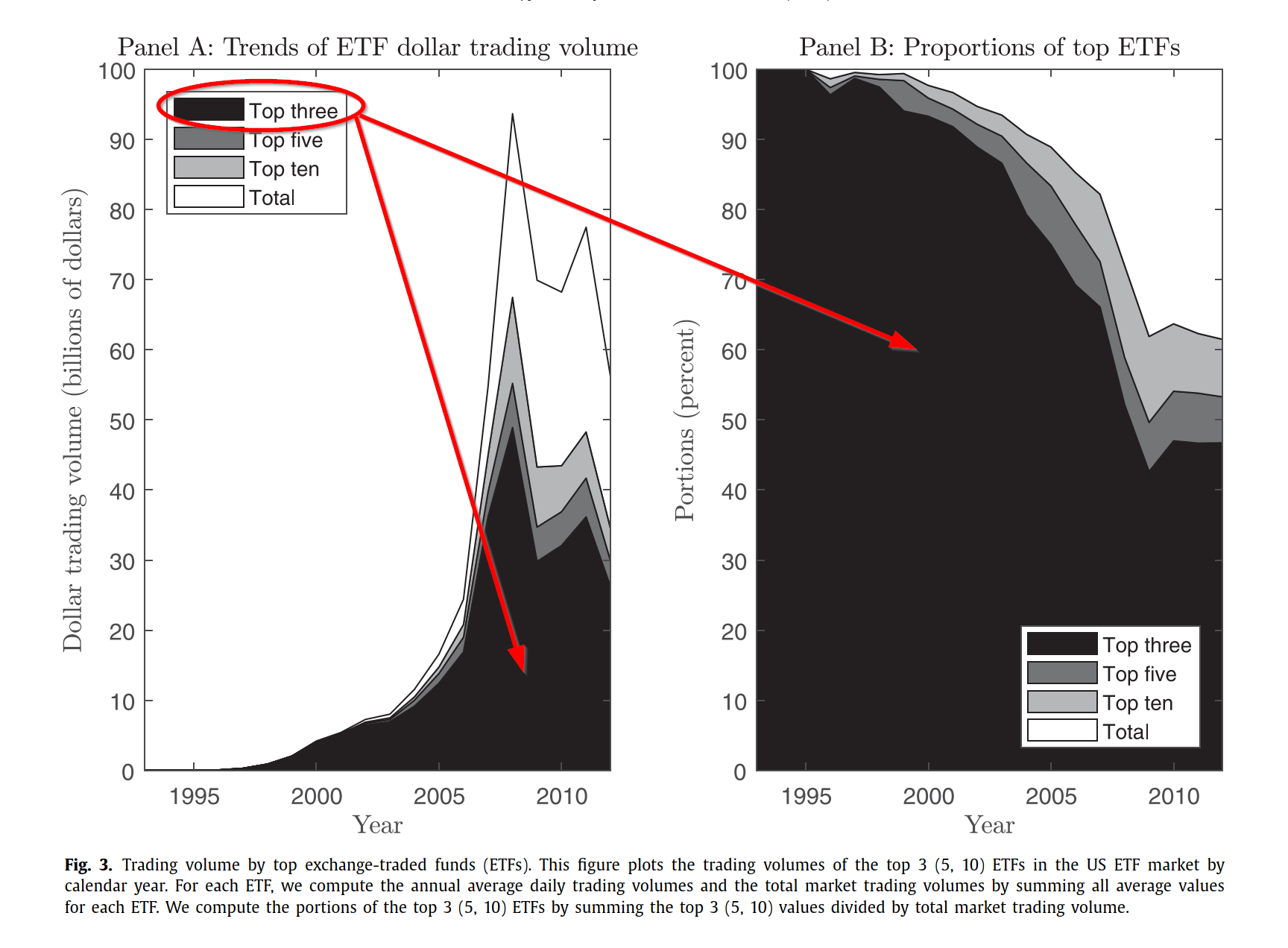

How Does ETF Liquidity Affect ETF Returns, Volatility, and Tracking Error?

By Tommi Johnsen, PhD|January 11th, 2021|Transaction Costs, Research Insights, Basilico and Johnsen, Academic Research Insight, ETF Investing|

Liquidity risk and exchange-traded fund returns, variances, and tracking errors [...]

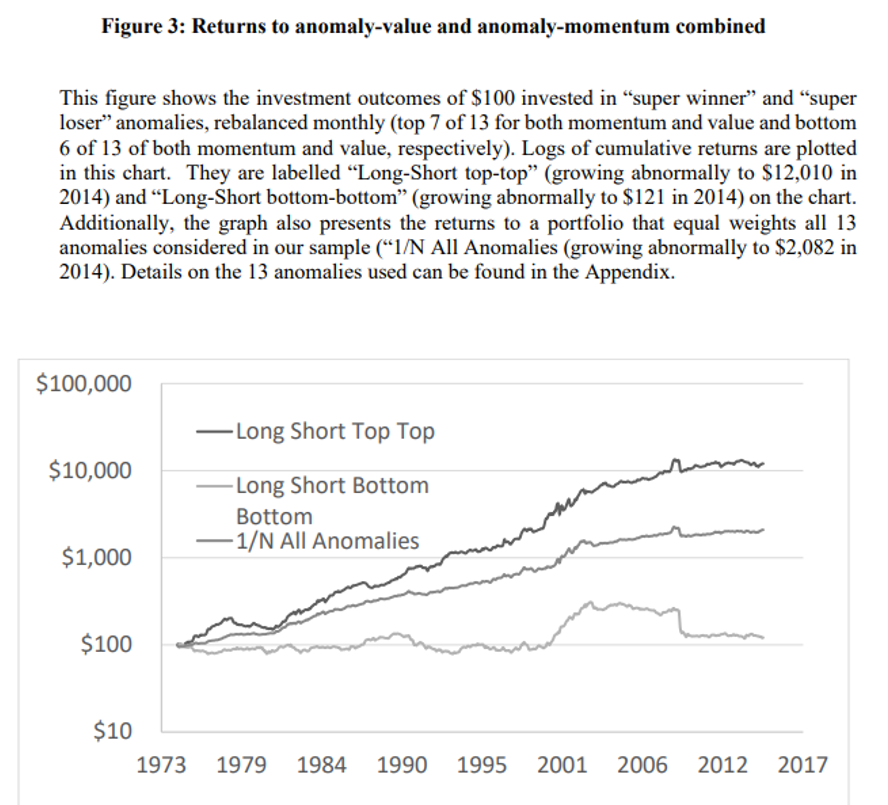

Value and Momentum and Investment Anomalies

By Larry Swedroe|January 7th, 2021|Research Insights, Factor Investing, Larry Swedroe, Value Investing Research, Momentum Investing Research|

The predictive abilities of value and momentum strategies are among [...]