Risk parity asset allocation systems seem to be all the rage these days.

If you are unfamiliar with the strategy, Mebane Faber has some great videos outlining how risk parity works.

Here is a source paper with the details on all the returns and information on a risk parity strategy:

Leverage Aversion and Risk Parity” by Asness, Frazinni, and Pederson (2012).

We have a nice research summary and a spreadsheet entitled “Risk Parity for Dummies”, which outlines the mechanics of risk parity and levered risk parity.

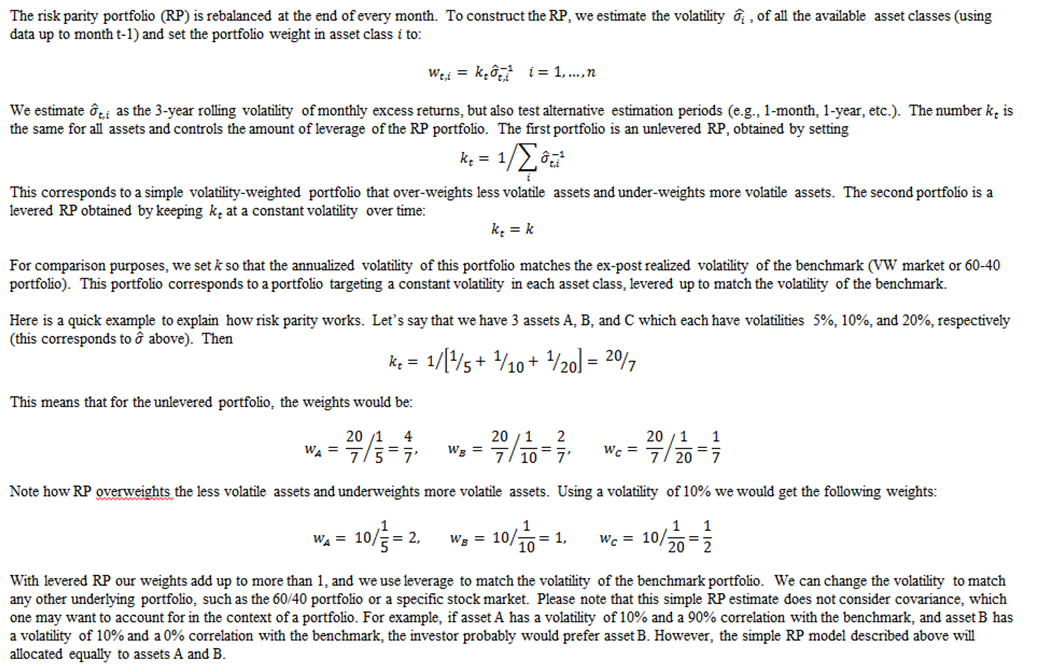

Here is quick outline of the most basic risk parity strategy (click to expand):

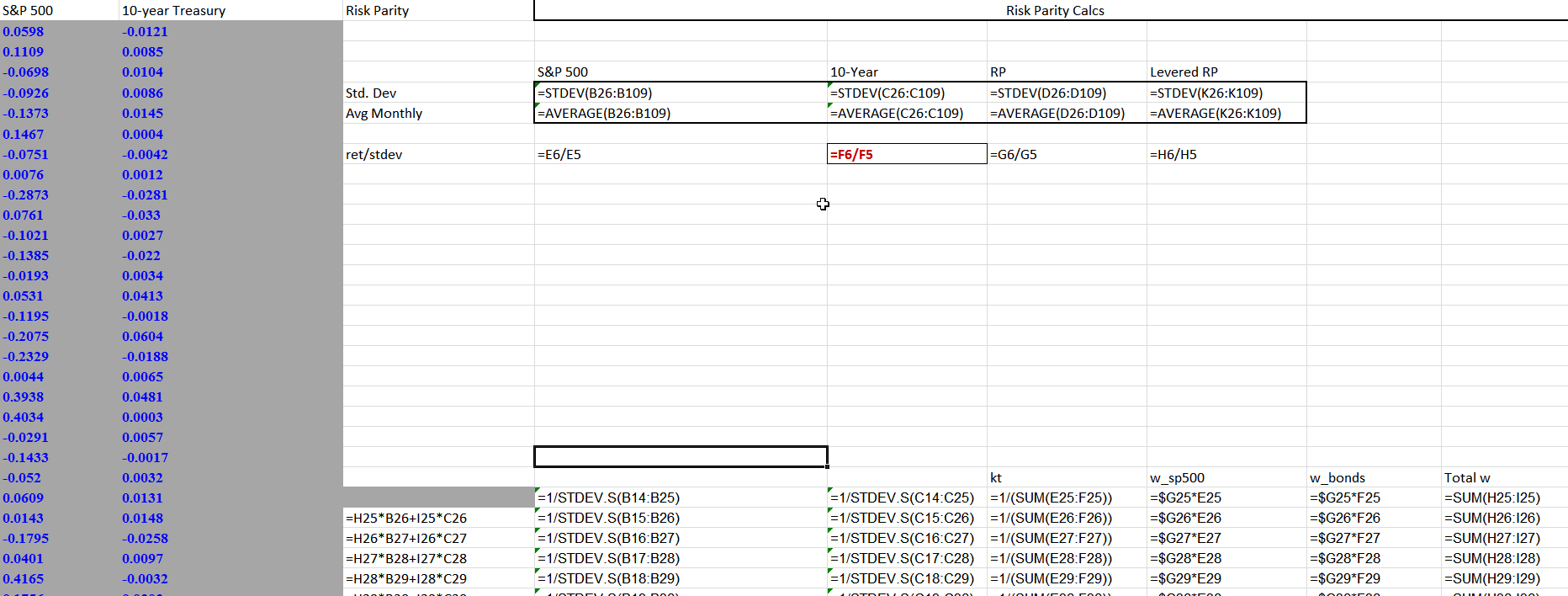

Here is the excel spreadsheet that shows you how to actually create a risk parity portfolio (click to expand):

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.