Timely Portfolio has a great post about the magical long-bond.

http://timelyportfolio.blogspot.tw/2012/08/bonds-much-sharpe-r-than-buffett.html

The thesis he presents is clear: long bonds won’t achieve what they’ve achieved over the past 30 years.

I think this thesis is correct, but this statement of presumed fact doesn’t answer the real question: Should we invest in the long-bond over the next 30 years?

Investing is all about opportunity costs. It may be the case that the long bond will not achieve the same sort of Sharpe over the next 30 years, but perhaps it will achieve a higher Sharpe than alternative investment classes.

I don’t know the answer for investing in bonds, but one can look at historical bond data and get some perspective on what is possible.

For a full research report on the subject, Empiritrage has a new report called “The Truth About Bonds.”

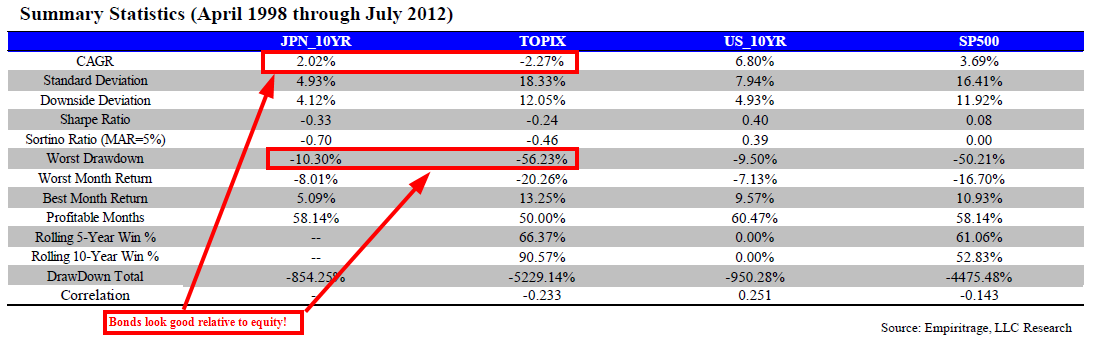

Below is my favorite chart. This chart looks at the performance of JGBs when they first broke 1.80% in April of 1998. The absolute risk/reward isn’t amazing, but relative to equity it is magical.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.