It appears Japanese monetary policy is beginning to resemble Kabuki. Kabuki is a form of Japanese theater that involves stylized performances that can appear positively bizarre to the uninitiated. So it goes with the Bank of Japan’s (“BoJ”) attempts to reflate the Japanese economy, which may qualify as drama, although the bond markets don’t seem to entirely understand the performance.

Let’s review some recent history. Japan has been mired in a deflationary spiral since the bursting of credit and real estate bubbles in the early 90s. Shinzo Abe, the recently elected Prime Minister of Japan, announced in December of 2012 a new policy, straight out the Keynsian playbook, to combat deflation. Abe agrees with Keynes who advocated for using public sector policies, such as interest rate easing by central banks, and government spending, to shape macroeconomic outcomes, including inflation.

Japan’s new policy, also known as “Abenomics,” includes fiscal stimulus, structural reforms, and a new target rate of 2% for inflation, which was to be achieved partly through purchases of Japanese Government Bonds (“JGB”), with a goal of doubling Japan’s monetary base, and reflating the Japanese economy. So how have things gone?

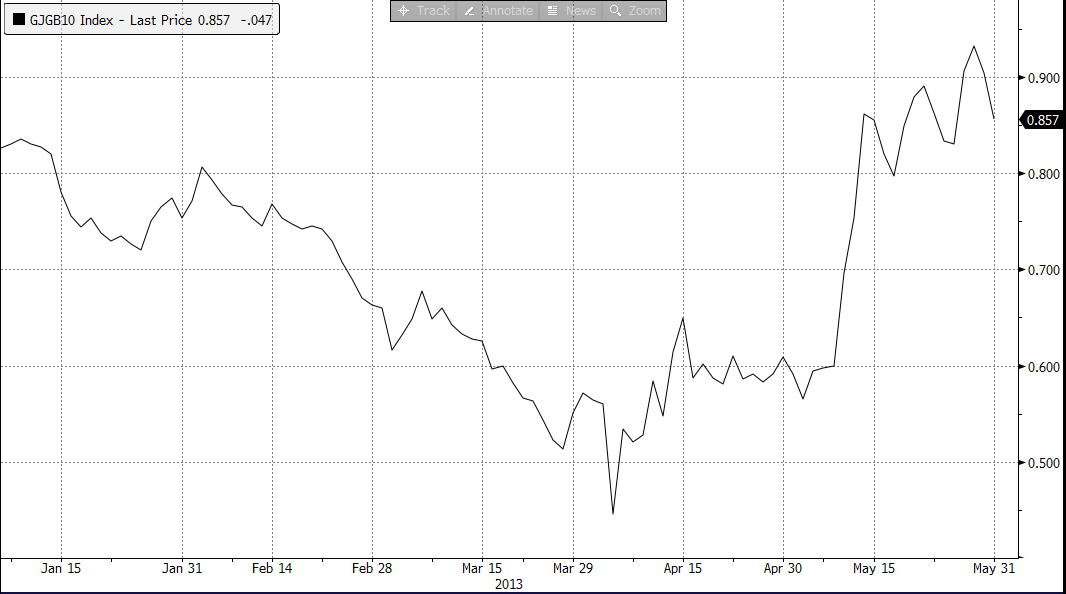

The BOJ announced a policy of easing, and began monthly purchases of Y7tn-Y8tn of JGBs. Normally, this type of stimulus has the effect of depressing bond yields, as it has done in the U.S., and this is indeed what happened. At first. But then something very strange happened: Here’s a graph of yields on the JGB 10-year bond:

Holy snikes!!! The yield on the 10-year JGB hit a low of 0.315% in April, before surging to over 1% in late May. (Though after the BoJ stepped in with additional liquidity, yields have pulled back to 0.857% as of Friday).

Wait a minute. This is the OPPOSITE of what is supposed to happen. Somewhere, Shinzo Abe is probably saying (as we said to our cable provider recently), “this is not the deal that I signed up for.”

When interest rates for a country are higher, there is a greater perceived risk associated with lending to that country. So the JGB market is sending signals that risks are increasing. So what are the risks?

One interpretation is fairly straightforward. Japan’s stated policy goal of 2% inflation would, if achieved, erode the real value of JGB’s fixed payments, and induce bondholders to sell. So perhaps bondholders are pricing in new economic growth and increased inflation expectations. There are reasons to believe this view is playing a role – May consumer prices in Tokyo posted a 0.1% gain, the first gain in several years, although Goldman Sachs recently noted that inflation-indexed JGBs are implying inflation of approximately 1% in 2016, which is below the target.

So are we now on a path to an economic recovery in Japan? BoJ governor Haruhiko Kuroda said just a few months ago that lower JGB rates were an important element of the stimulus, since cheaper money encourages borrowing. Markets can sometimes, however, react more quickly than economies. Consider that, presumably due to higher rates and market volatility, Toyota recently cancelled a Y20bn bond sale, and JFE Holdings, a Japanese steel producer, also postponed its own bond sale. Then again, although JGP yields are up sharply since April, they are still near where they were when Abenomics was announced in December of 2012, so perhaps JGB rates are not so high that they will choke off growth.

Then there is the state of bank lending in Japan. Credit creation accompanies economic expansion, as banks lend to businesses attempting to finance growth. But Japanese banks may be becoming less willing to lend since the spike in JGB yields has hurt their balance sheets. Japanese Banks own on the order of 43% of the $8tn JGB market, and have seen mark-to-market losses on those bonds as yields have climbed. Kuroda has said that banks will be able to offset these losses through additional lending, although it’s also possible that rates will increase and growth will not, which could threaten banks’ capital ratios.

And then there is the elephant in the room: Japan’s massive public debt, which is approaching 250% of GDP, far and away the highest among developed economies. According the Economist, an official at the finance ministry recently said, “So far there is no connection between volatile bond yields and the fiscal position.”

Some certainly disagree with this assessment. Noted Japan bear Kyle Bass attended last week’s Ira Sohn investment conference, where he said, “the beginning of the end has begun” for Japan’s finances. “What they’re doing represents 70% of what the Fed is going here with an economy 1/3 the size of ours.” Bass may be focused on the so-called “Keynsian Endpoint,” when balance sheets are exhausted, and all government revenues are required to finance interest expense associated with the public debt. In Bass’s view, the Japanese government is effectively insolvent; the deficit is financed by money printing as government debt simply moves from the Ministry of Finance (Japan’s Treasury) to the BoJ. Yet perhaps we are not there yet, as Japan’s debt service of Y22tn for 2012 comprised approximately a quarter of government revenues, although again, increasing JGB rates may send that government interest expense higher.

There’s something refreshing about a Texas hedge fund manager who’s not afraid to call it like he sees it. If Japan does approach such an endpoint, it may be that the only options are a default, devaluation, or restructuring (usually a writedown for bondholders). Kyle Bass is betting things will play out this way for Japan.

Alternatively, perhaps there are reasons to be optimistic about the big picture for Japan. The Nikkei is up by over 30% this year, even after a recent pullback. Wealth effects from a sharply higher stock market may boost consumer spending.

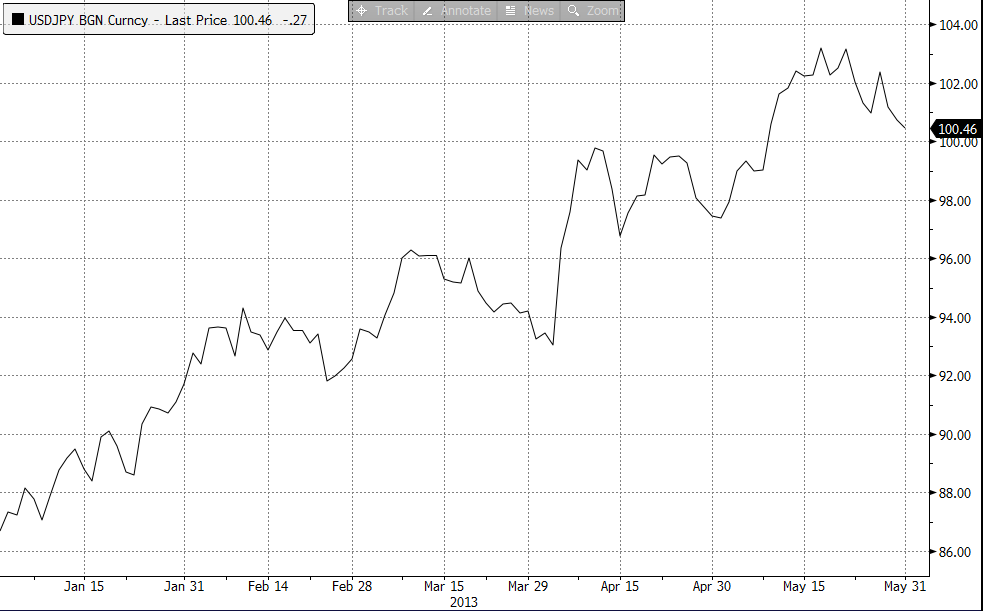

The Yen has also lost about a quarter of its value versus the US dollar since the beginning of the year. A weaker Yen boosts exports, as Japanese goods become less expensive, leading to increased manufacturing and higher earnings for Japanese business. Ready to buy a new Honda Accord or Toyota Corolla?

Public works spending is also accelerating, and the government is undertaking structural reforms which may also have an impact. In short, Abenomics may be awakening animal spirits in Japan, whose GDP grew at a 3.5% rate in the first quarter. Perhaps Japan’s 20+ year deflationary mindset may be finally changing?

Regardless of whether you subscribe to Shinzo Abe’s, or Kyle Bass’s view, we will continue to watch JGB yields for clues about Japan’s ongoing turnaround. It should make for interesting theater going forward.

Deflation, hyperinflation, or something in between–Thoughts?

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.