Political Risk Spreads

- Bekaert, Harvey, Lundblad, and Siegal

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

We introduce a new, market-based and forward looking measure of political risk derived from the yield spread between a country’s U.S. dollar debt and an equivalent U.S. Treasury bond. We explain the variation in these sovereign spreads with four factors: global economic conditions, country-specific economic factors, liquidity of the country’s bond, and political risk. We then extract the part of the sovereign spread that is due to political risk, making use of political risk ratings. In addition, we provide new evidence that these political risk ratings are predictive, on average, of future risk realizations using data on political risk claims as well as a novel textual-based database of risk realizations. Our political risk spread measure does not make the mistake of double counting systematic risk in the evaluation of international investments as some conventional measures do. Furthermore, we show how to construct political risk spreads for countries that do not have sovereign bond data. Finally, we link our political risk spreads to foreign direct investment. We show that a one percent point reduction in the political risk spread is associated with a 12 percent increase in net-inflows of foreign direct investment.

Data Sources:

ICRG, OPIC, CO, and a few others.

Alpha Highlight:

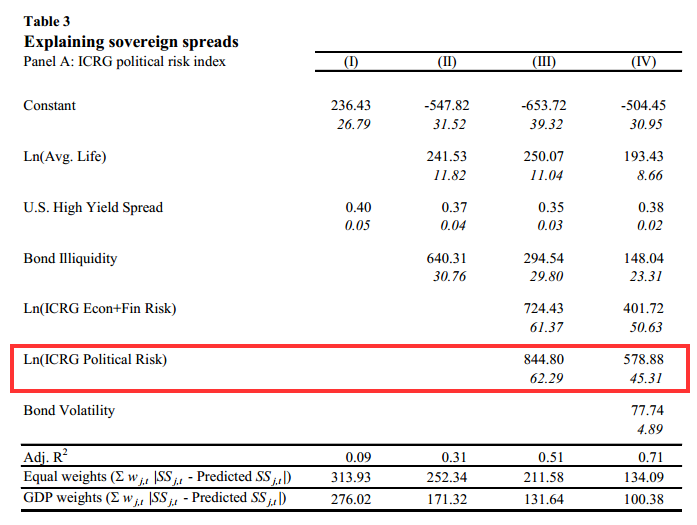

One of the formal regression tests to show that political risk matters for sovereign spreads:

Commentary:

- An interesting “technique” paper to identify a way to pinpoint political spread.

- Political spread means taking on additional risk–this isn’t a free lunch!

- Watch out for crazy dictators.

Which readers love Zimbabwe bonds?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.