The Investment Performance of Art and Other Collectibles

- Elroy Dimson, Christophe Spaenjers

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

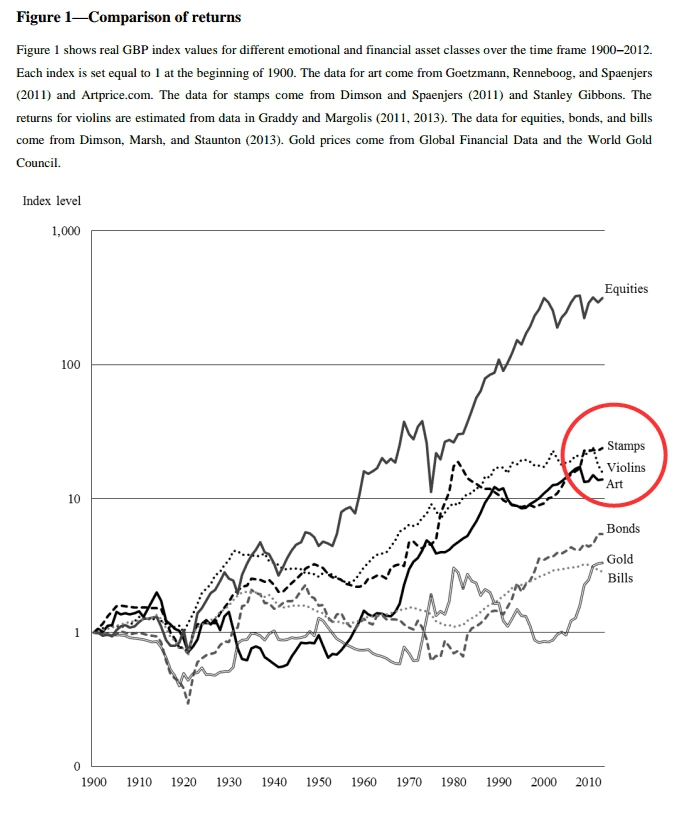

We assess the long-term financial returns from high-quality collectible real assets, and review the unique risks that are associated with such investments. Over the period 1900-2012, art, stamps, and musical instruments (violins) have appreciated at an average annual rate of 6.4%-6.9% in nominal terms, or 2.4%-2.8% in real terms. Despite the similarity in long-term returns, short-term trends can vary substantially across these different types of emotional assets. Collectibles have enjoyed higher average returns than government bonds, bills, and gold. However, it is important to recognize the quantitative importance of transaction costs in collectibles markets. In addition, price volatility is larger than is suggested by conventional measures of risk, and these assets are also exposed to fluctuating tastes and potential frauds. Yet, despite the large costs and many pitfalls, investment in emotional assets can pay off, because of the non-financial yield they provide.

Data Sources:

1900-2012–long time series!

Alpha Highlight:

High volatility returns!

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Paper first reviews the long-term investment performance of three important categories of “emotional assets”—stamps, art and musical instruments (violins) and compares with the performance of other financial assets (Equities, Bonds, Bills, Gold).

- Table 1 reports returns from 1900-2012.

- Collectibles had higher returns than bonds, bills and gold.

- Annualized real returns from high to low: Equities: 5.2%, Stamps: 2.8%, Violins: 2.5%, Art: 2.4%, Bonds: 1.5%, Gold: 1.1%, Bills: 0.9%.

- Table 1 reports returns from 1900-2012.

- Paper then discusses the costs and risks of investing in “emotional assets”.

- High Costs:

- Transaction costs: can be as high as 25%, including auction house fees, dealer mark-ups, tax and so on. The impact of such costs on net annualized returns is inversely related to the holding period.

- Illiquidity: auction houses do not hold sales continuously, and searching for potential buyers can be time-consuming and costly.

- Other expenses: storage and insurance costs.

- High Risks:

- Return volatility: Standard deviation tends to underestimate the true volatility of collectibles.

- Difficult to diversify risks, since it’s not affordable for most investors to buy a set of artworks.

- Changes in tastes and wealth pattern: Demand is hard to predict, since tastes and wealth distributions change over time.

- Other risks such as fads and bubbles, forgeries and frauds, and problems with indirect investment.

- High Costs:

Strategy Commentary:

- Without a large amount of capital, it may be difficult to build a diverse portfolio of emotional assets.

- This market may be interesting to investors who already have a diversified portfolio of financial assets, who have a long investment horizon, and who can sit out periods of high illiquidity and low demand for luxury consumption.

Stamps, Art, and Musical Instruments–Who’s Ready to Add them to the Portfolio?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.