John Bogle did a tremendous service to humanity when he launched the first index fund in 1975. By providing people with a passive, low-cost way to invest in the entire stock market, Bogle enabled generations of investors to get cheap beta exposure, and avoid the high fees, commissions, taxes, and other costs associated with active management approaches. Clearly, consumers thought this was a good idea. The firm he founded, the Vanguard Group, now manages approximately $2.75 trillion.

Writing about the formation of his first index fund, started with $11.4 million, and his initial thoughts on costs, he has stated, “…[I] projected the costs of managing an index fund to be 0.3% per year in operating expenses and 0.2% per year in transaction costs.” Since those days, indexing has only gotten cheaper and much more popular, since it makes so much sense. The Vanguard 500 Index Fund Investor Shares fund currently has an expense ratio of 17 bps (Admiral Shares are cheaper) and, as of the end of 2013, had net assets of approximately $160 billion. This has spawned a host of imitators. Firms like Fidelity, BlackRock and Invesco have all jumped into the game, and provide a range of indexing products.

More recently, there has been a new wave breaking over the asset management business: “smart beta.” While the idea behind smart beta, and its promise of higher risk-adjusted returns, is compelling, investors should beware and understand what exposure they are buying. Incidentally, if you’re looking for additional commentary on smart beta, this post was inspired by momentum guru Gary Antonacci, who has some choice words for the smart beta approach in an upcoming book on momentum investing.

What is Smart Beta?

Smart beta likes to bill itself as an improvement over Bogle’s indexing approach, which smart beta might describe as “dumb” since it is purely passive. For example, while a traditional index fund might weight its holdings based on market capitalization, a smart beta fund might invest using equal weights. Such an equal weighting approach might tend to tilt a portfolio towards value stocks, which have tended to beat the market averages over long time frames. Other smart beta approaches might include a weighting scheme based on fundamental attributes, such as sales, earnings, or dividends.

Before providing analysis, we want to be clear on how we define different strategies in the marketplace. We see the world in three general buckets: index, closet index, and active.

- Index: large portfolios (50+ stocks, typically 100s), very low tracking error with common benchmarks. “Dumb” allocations that aren’t trying to “beat” the market by outsmarting the world.

- S&P 500, Russell 2000

- Closet-index: large portfolios (50+ stocks, typically 100s), very low tracking error with common benchmarks. These allocations are “smart”, in the sense that they claim to be marginal improvements upon the “dumb” allocations described by the “index” category above.

- S&P 500 Value, Russell 2000 Growth

- Active: concentrated portfolios (<50 stocks), high tracking error with common benchmarks. These strategies are “going for it” and trying to beat passive benchmarks by taking on true selection risk.

- Hedge funds, concentrated mutual funds (Legg Mason Value Trust is an example).

We consider smart beta to be a closet-index product and nothing more, however, smart beta pretends to be something special.

Unfortunately, from a statistical standpoint, smart beta and closet-indexing have the exact same characteristics, save one: fees. Closet index products are much cheaper than “smart beta” products.

What’s in a name? That which we call a rose by any other name would smell as sweet.

— William Shakespeare, Romeo and Juliet

Shakespeare’s point is that the only thing you should care about is what something actually is, not what you call it. And the problem for smart beta is that it is often just another name for something that you can already get more cheaply via various index funds.

And so the growing fear in the asset management world is that smart beta is basically a marketing gimmick, used by sponsors who trot out marginally more expensive closet-index products that customers can get elsewhere for less.

Is Smart Beta really Closet Indexing?

We think smart beta is expensive closet indexing. Let’s take an example to see why. The Guggenheim S&P 500 Equal Weight ETF would seem to be a “smart” way to achieve exposure to the S&P 500, since you are using equal weights. For the privilege of getting such exposure, you can pay 40 bps, which is the gross expense ratio of this ETF.

This is more than you would expect to pay for an index fund. But Guggenheim would say that that’s okay, because this is a product that, in theory anyway, should provide investors with some kind of “smart” exposure, which is worth paying for. Let’s do a more critical examination of what exposure we are actually getting.

Consider the components of the Guggenheim S&P 500 Equal Weight ETF. In general, the S&P 500 contains many more small-cap stocks than large cap stocks. Thus, due to the equal weighting regime, a large proportion of the total dollars in the portfolio are invested in small cap stocks. In a sense then, we are effectively investing heavily in small-caps.

But what would happen if you simply bought small cap stocks via a generic small-cap index fund? We should expect its performance to be different from our Guggenheim product, right?

So how different? What would you expect to be the performance difference between a small-cap index, which selects stocks only on the basis of their size characteristics, and the stocks from among the entire market as selected by our “smart” weighting approach?

Is there a big difference? A small difference?

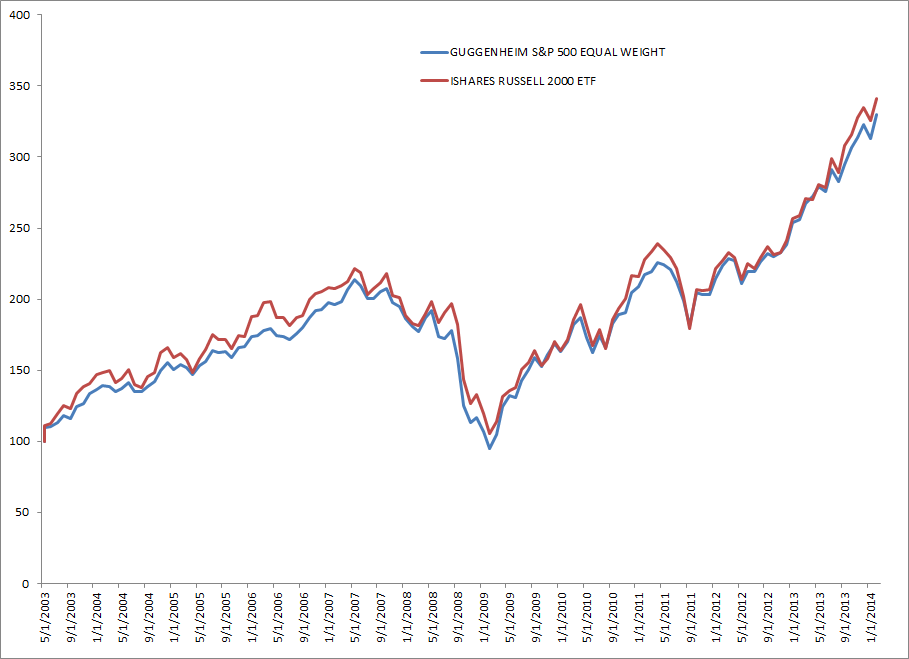

In order to answer this question, we compare the “smart” Guggenheim S&P Equal Weight ETF, with a small-cap index, the iShares Russell 2000 ETF, which can give us passive small-cap exposure:

Note: This example is from Gary Antonnaci. All credit for this specific example should be given to Gary. The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

There is very little difference. These two ETFs track each other almost exactly, except that the small cap index actually appears to outperform the equal weighted smart beta product. What might account for this difference?

The expense ratio on the iShares Russell 2000 ETF is 24 bps, yet as discussed earlier we pay 40 bps for the “smart” product. It may be that it is the spread between these expense ratios that drives the differences in performance reflected in the graph above.

At the end of the day, it’s hard to get excited about such forms of “smart beta.” These products are trying to capture the benefits of being an active manager, but end up being “closet indexes,” since they provide the exposure of an index fund–but at a higher cost!

Is All Lost?

If you really believe in “smart beta” factors you should buy them in concentrated form via a serious active management product (that doesn’t charge an arm and a leg, of course). Seek high tracking error and concentrated portfolios, focused on stock characteristics that you believe are mispriced (e.g., value)–you’ll actually get the beta and some projected “alpha.” Don’t pay for a wishy-washy exposure to value or momentum via a smart beta product–you achieve the beta, but at high cost. To be fair, we have seen reasonable arguments made that weighting schemes can provide a unique exposure that is different from characteristics tilts. The key thing to think about as an investor is in differentiating the value-add from a weighting scheme and a factor tilt. Ideally, an investor would identify a weighting schema and a factor tilt that add complementary value.

Smart beta is smart marketing, but doesn’t seem to be smart investing…at least in its present form and present costs…

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.