How do your feelings affect your decisions?

“Humans perceive and act on risk in two fundamental ways. Risk as feelings refers to individuals’ instinctive and intuitive reactions to danger. Risk as analysis brings logic, reason, and scientific deliberation to bear on risk management. Reliance on risk as feelings is described as “the affect heuristic”. —- Paul Slovic and Ellen Peters (2006).

And another quote:

“All perceptions contain some affect. We do not just see ‘a house’: We see a handsome house, an ugly house, or a pretentious house”. —- Zajonc.

When we make a decision, we consider not only how we think about it analytically, but also how we feel about it, which can skew how we assess its risks. If we have positive or favorable feelings about an activity, we tend to magnify its benefits in our minds and reduce its perceived riskiness. Conversely, if we have negative or unfavorable feelings, we tend to ascribe higher risks to it and lower benefits. This is known as the “affect heuristic.” While we often feel we are being rational in making our judgments, the affect heuristic influences us in profound ways that are directly related to our feelings, and not our rationality.

In “The Affect Heuristic in Judgments of Risks and Benefits,” by Finucane, et al., (a copy can be found here), the authors discovered some interesting ways we can be manipulated by our affect. The study includes an experiment relating to nuclear power.

We all know that there are benefits to using nuclear power, including that it does not rely on a diminishing supply of fossil fuels, or oil imports, and can be produced almost without limit. We also know that there are risks to using nuclear energy, including health risks, the risk of accidents, nuclear waste storage issues, and the production of fissionable material for power could also be used for nuclear weapons. Now the benefits and risks of nuclear power are two separate issues. For example, the fact that nuclear power has these various risks is completely unrelated to the benefits described. They are independent, distinct concepts. Yet due to the affect heuristic they can become linked.

The study (which I simplify here to illustrate the point of the research) describes how subjects were asked, preliminarily, to evaluate the benefits and risks of nuclear power, on a scale of 1 to 10. Next, the subjects were given vignettes about nuclear power. A vignettes might highlight, for example, the high-benefit attributes of nuclear power. Then subjects were again asked to rates the benefits and risks.

For purposed of discussion, let’s say Subject A awarded a 6 for benefits, and a 5 for risks. Next, he reads a vignette extolling the high benefits of nuclear power. As expected, Subject A responded to the vignette by bumping his initial benefit assessment from a 6 up to, say, an 8. Now you would hope that, since the risks of nuclear power are, as discussed, a completely separate issue, that the his initial risk assessment of 5 should stay a 5, since there was no new information provided relating to risks. But that’s not what happened.

Subjects experienced the affect heuristic, and Subject A awarded a lower risk score (a 3, say). Additionally, the study showed how, in general, judgments related to benefits and risks were inversely correlated. Thus, as with the example above, as the benefits increased, the perceived risks decreased. The affect heuristic cuts both ways: it influences both perceived benefits as well as perceived risks.

In studies conducted by Paul Slovic et al., the researchers showed how high risks promoted and propagandized by the media contributed to a reduction in the public’s perception of the benefits of nuclear power.

Seymour Epstein, a professor at U. Mass, describes the mechanism of how our affect drives our behavior:

The experiential system is assumed to be intimately associated with the experience affect…which refer[s] to subtle feelings of which people are often unaware. When a person responds to an emotionally significant event…the experiential system automatically searches its memory banks for related events, including their emotional accompaniments…If the activated feelings are pleasant, they motivate actions and thoughts anticipated to reproduce those feelings. If the feelings are unpleasant, they motivate actions and thoughts anticipated to avoid the feelings.

The affect heuristic kicks and leads us to conclusions that seem obvious at first, but which can appear surprising when we pause to think carefully.

Would you rather be injured by lightning or a downed power line?

This is a variation of the affect heuristic at work and is actually the title of a paper by Rudski et al. (a copy can be found here), which describes our preference for natural over artificial (unnatural?”) options, and how we tend to minimize the risks associated with natural hazards, even when these may not accord with the objective probabilities. We automatically judge the power line to be “bad,” and the lightning to be, by comparison, relatively “good.” We are primed by our innate emotional preference for the natural event, versus the artificial.

Game 1: Which unpleasant option do you prefer? Would you rather:

- Break a leg A) hiking, or B) in a car accident?

- Get food poisoning at A) an organic restaurant, or B) in a fast food restaurant?

- Contract lung cancer A) due to genetic influence, or B) from smoking?

- Get severe sunburn A) during a day at the beach, or B) in a tanning bed?

- Get a severe rash from A) poison ivy, or B) from formaldehyde?

- Get a puncture wound from A) a dog bite, or B) stabbing?

- Experience a municipal evacuation due to A) a volcano, or B) a power plant accident?

- Have 30 elderly deaths occur due to A) a heat wave, or B) CO poisoning?

- Experience paralysis from A) a dart frog, or B) nerve gas?

If you’re a human being, like we are, you probably chose option A in almost every question above.

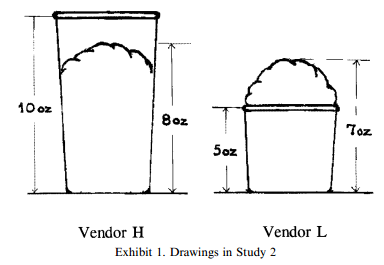

Game 2: Which cup of ice cream is more appealing?

Hsee (1998): Less is Better: When Low-value Options Are Valued More Highly than High-value Options

Here is an interesting game designed by Hsee(1998). Imagine that you are lying on a beach, and you want to buy an ice cream. There are two vendors selling ice cream nearby. Vendor H fills the ice cream in a relatively larger-capacity cup and the ice cream is under-filled. Vendor L fills the ice cream in a relatively smaller-capacity cup and the ice cream is over-filled (as per the diagrams below). The survey results demonstrated that an over-filled ice cream container with 7 oz of ice cream was valued more highly (as measured by willingness to pay) than an under-filled container with 8 oz of ice cream. The cup size is a reference point and the over-filled ice cream cup gives people more positive feeling and satisfaction, generating the affect heuristic.

Applications in Finance:

In the two examples above, you have seen how the affect heuristic, as manifested by some emotional underlying state or association, can influence how we make decisions. As you might expect, our stock picking is significantly influenced by the same effect.

In “the Effect of Corporate Image as an Affect Heuristic on Investors’ Decision Making,” byu Hung-Jen et al. (a copy can be found here), the authors recruited groups of students to participate studies that explored how they were affected by corporate image.

First, a number of students were divided into two groups (Group 1 and Group 2) and given “positive” and “negative” information about a corporation. Group 1 was presented with 1) positive images: descriptions of a corporation with high quality, low cost products with innovative designs, with good customer service and focused on social responsibility; Group 2 was presented with 2) negative images: a corporation with low quality, overpriced products with old designs, poor customer service, and a profit-oriented philosophy.

The students were asked whether they would purchase shares in the company. The results? Within Group 1, presented with positive images, 85% said they would buy shares. Within the Group 2, presented with negative images, only 9% said they would buy shares.

This demonstrates that when investors have a positive view of a company, they are more likely to purchase the stock.

Next the researchers wanted to see how the addition of “positive”” and “negative” financial information affected the decision to buy stock. “Positive” financial information included seasonal outperformance, an upwards EPS revision, or a reduction in overhead costs. “Negative” financial information included seasonal underperformance, a downwards EPS revision, or an increase in overhead costs.

A new group of students were divided into four sub-groups, each getting different combinations of corporate image and financial information. Below are the results:

- “Positive” corporate image, and “Positive” financial information: 91% chose to buy stock

- “Positive” corporate image, and “Negative” financial performance: 13% chose to buy stock

- “Negative” corporate image, and “Positive” financial performance: 9% chose to buy stock

- “Negative” corporate image, and “Negative” financial performance: 3% chose to buy stock

Two things to note here:

First, note that the addition of financial information was not enough to offset the effect of a positive corporate image. More students chose to buy stock in a company with positive corporate image and negative financial information (13%) than chose to buy stock in a company with negative corporate image and positive financial information (9%). Corporate image, as influenced by the affect heuristic, appears to be a strong predictor of stock purchase intentions.

Second, note that the addition of negative information, consistent with prospect theory, tended to moderate the effect of the affect heuristic. The addition of negative financial information for companies with a positive corporate image cause students to desert the stock in droves: the percentage choosing to buy plummeted, from 91% to 13%.

Game 3: Which company would you rather own? A company that:

- A) makes fresh dairy products, yogurts, and baby foods, or B) produces coal from surface and underground mines

- A) operates a bakery-cafe, offering fresh baked goods, made-to-order sandwiches, soups and salads, or B) operates petroleum refineries

- A) sells athletic footwear, apparel, and accessories, or B) offers electrical and industrial components, and hazardous duty electrical equipment

- A) sells specialty coffee, hot cocoa, teas and other beverages, or B) manufactures and sells chemicals, plastics, and fluids.

What if all these companies all had positive financial news? What if they all had negative financial news?

Reference:

- Slovic, P., Finucane, M.L., Peters, E., MacGregor, D.G., 2002. The affect heuristic. European Journal of Operational Research 177,1333–1352.

- Hsee, C.K., 1998. Less is better: when low-value options are valued more highly than high-value options. Journal of Behavioral Decision Making 11, 107–121.

- Yoav Ganzach (2000), Judging Risk and Return of Financial Assets, Organizational Behavior and Human Decision Processes, Vol. 83, No. 2, pp. 353–370

- Risk Perception and Affect, file:///C:/Users/Tian/Desktop/Tian’s%20folder/riskperceptionandaffect.pdf

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.