Investment Restrictions and Fund Performance

- Clifford, Fulkerson, Hong, and Jordan

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

We examine why mutual funds appear to underperform hedge funds. Utilizing a unique panel of mutual fund contracts changes, we explore several possible channels, including: alternative investment practices (e.g., short sales and leverage), performance-based compensation, and the ability to restrict the funding risk of fund flows. We document that over our sample period, mutual funds were more likely to shift their contracting environment closer to that of hedge funds. However, this shift provided no benefit to mutual funds and we find no causal link between these contract changes and improvements in performance. Rather, our results cast doubt on the binding nature of investment restrictions in the mutual fund industry.

Alpha Highlight:

The evidence from academic research shows that mutual funds have no gross of fee alpha, but hedge funds, on average, may have gross-0f-fee alpha (the HF database is questionable). There is a lot of debate surrounding these findings, but that is the general takeaway. A natural question academics have asked is, “Why do hedge funds outperform?” One hypothesized advantage for hedge funds is the contracting environment. For example, hedge funds have an ability via the limited partnership structure to lock-up capital, charge performance fees, short-sell, trade exotic contracts, and so forth.

The authors in this paper look at a quasi-natural experiment where mutual funds go from a plain-vanilla operating structure and change their operating environment such that it more resembles a hedge fund.

The authors then test the following hypothesis:

Do mutual fund managers that adopt “hedge-fund-like” features improve performance?

In short, the answer is no. Performance on mutual funds that adopt hedge fund characteristics actually perform the same–and sometimes worse–than they did operating in a plain vanilla environment.

The authors come to the following conclusions:

Our evidence is not consistent with the idea that investment constraints prevent mutual fund managers from performing at the same level as their hedge fund counterparts.

The legal environment in the United States places heavy restrictions on mutual funds that attempt to implement hedge fund strategies…[but] it is unclear why we find no evidence that mutual fund performance improves following the change.

Our results are consistent with a growing body of literature pointing to the fact that mutual fund and hedge fund performance may not be as dissimilar as previously thought.

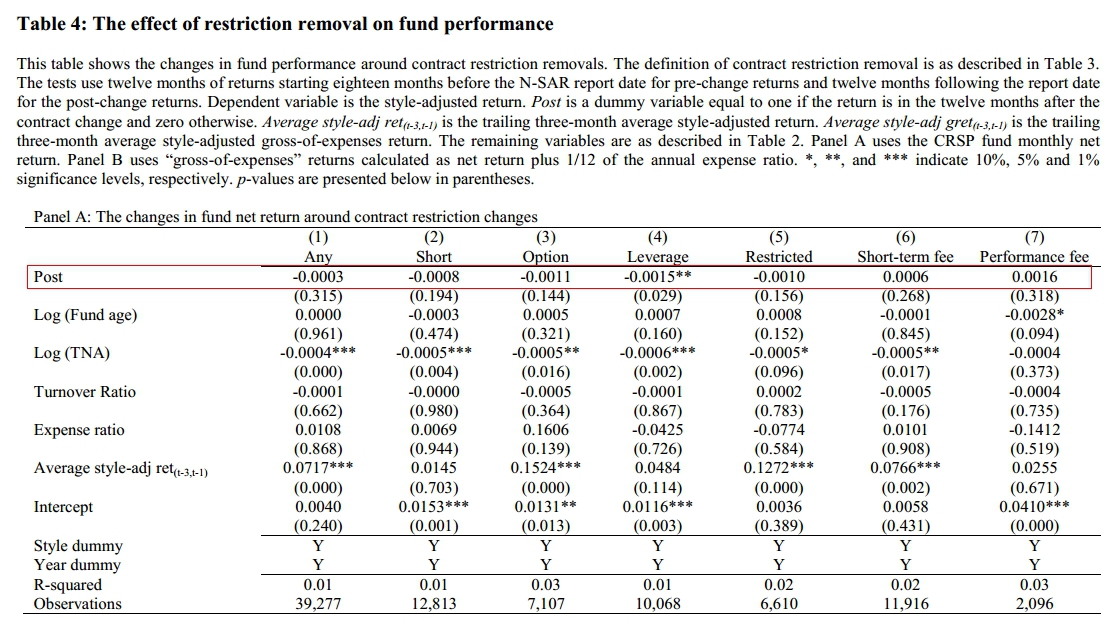

Here is the key chart from the paper. The “Post” variable is the key variable of interest. A positive value indicates a positive relationship between performance and hedge fund characteristics; a negative value indicates the opposite. The evidence highlights that the contracting environment can’t save the lame-duck nature of mutual fund performance net of fees.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

What do you think? Time to become a day-trader?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.