A recent New York Times article examines the story of Joel Greenblatt, author of “The Little Books That Beats the Market.” Joel has leveraged this book and is now managing money using a similar strategy for Gotham Asset Management. Joel is, of course, an investment legend at this point. We have been fans of Joel because he follows the goals of our firm, which is to empower investors through education. All that said, at Alpha Architect there ARE NO SACRED COWS.

Some of his newer mutual funds involve a hedge-fund investment strategy that goes long cheap stocks and short expensive stocks.

Here is the quote from the article:

At a meeting on Oct. 1, with 10 brokers in a cramped conference room in his Madison Avenue office and 40 more listeners on the phone, a tanned and confident Mr. Greenblatt told them, “We buy the cheapest we can find and short the most expensive.” With copies of his book stacked behind him, he said the general methodology had been “back-tested back to 1990” and “has worked for 30 to 40 years, no question.”

While not taking a beta-neutral bet, the largest fund (Gotham Absolute Return Fund) involves having a long exposure of 120%, and a short exposure of 60%.

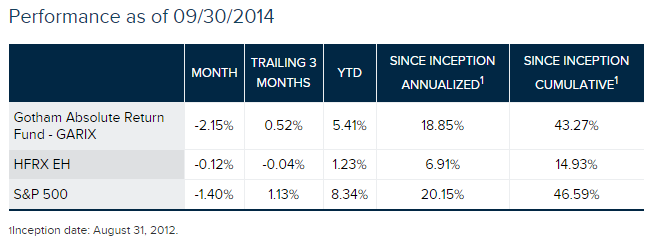

So how has this fund done?

Here are the results:

By any estimation, on a market-exposure adjusted basis this fund has done a great job since its inception.

In expectation, a fund with a 60% net long exposure would expect to return 60% times the market return plus the risk free rate. During this time period (with the market return = 20.15% and risk-free rate essentially equal to 0%), the expected return would have been (60%)(20.15%) + 0% = 12.09%. Gotham Absolute’s 18.85% has after-fee out-performance of over 6.75% on an annualized basis–not bad!

So even after the large management fee (2.00%) in the prospectus, and a 1% redemption fee (within 90 days), is this a free lunch?

Investigating long cheap, short expensive strategies

We decided to do a simple analysis of Mr. Greenblatt’s “magic formula.”

- Variable 1: EBIT/TEV (Total enterprise value)

- Variable 2: EBIT/Total capital

To avoid smaller firms, we eliminate all firms below the NYSE 40th percentile, which was around $1.95 billion on 12/31/2013. On 12/31/13, this leaves a universe of around 1050 firms.

All returns are total returns and include the reinvestment of distributions (e.g., dividends).

We then rank the firms on the two variables, and form quintiles of the average rank. The quintile portfolios are formed on 6/30 each year, held for a year, and equal-weighted.

To replicate the Gotham Absolute Return Fund, we buy the top quintile (~200 firms) with 120% exposure, go short the bottom quintile (60% exposure), assume a management fee of 2.00%, and a short rebate of 0.25%.

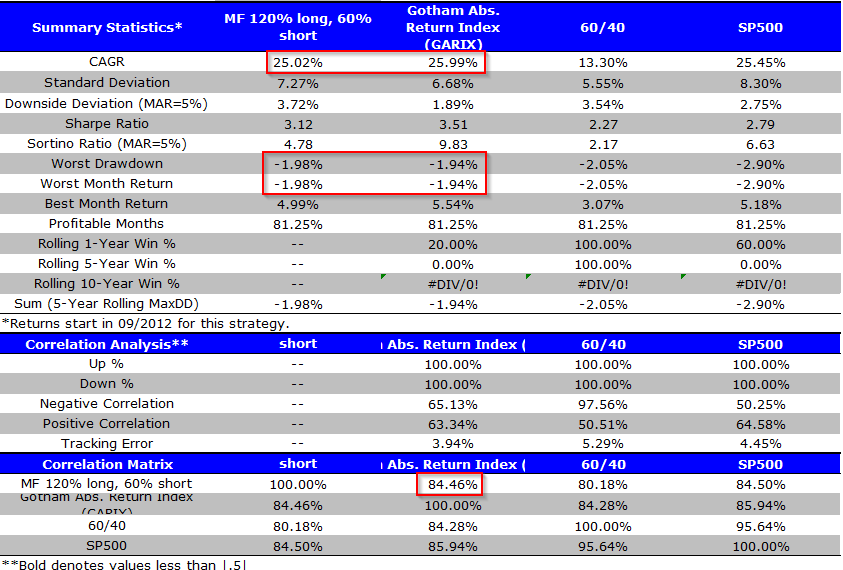

Here is how our replicated strategy compares to the live returns (from 9/1/2012-12/31/2013).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

While the replicated strategy returns are not exactly the same, they are clearly very similar, with nearly identical compound annual growth rates (CAGRs) and a 84.46% correlation over the 16 month period. For such a short time period, this level of similarity suggests a pretty close relationship between the simple magic formula and the version that Gotham claims to be implementing, which is “enhanced” by a team of analysts who make adjustments to account for esoteric valuation considerations such as pension obligations and legal claims.

So what about Greenblatt’s claim this strategy has worked for “30 to 40 years, no question.”

What Happens to Long Cheap, Short Expensive, Historically?

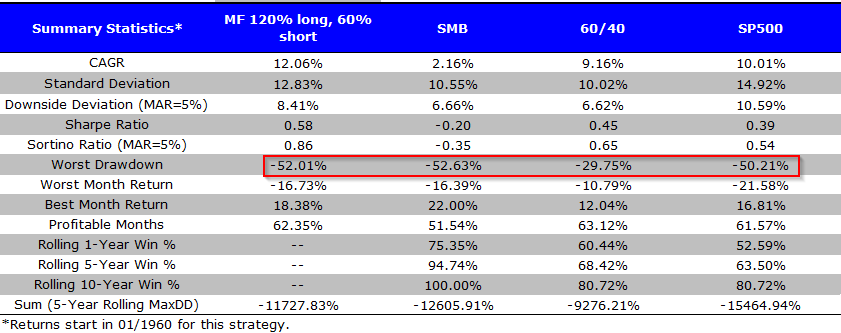

Here are the returns from 1/1/1960-12/31/2013, using the same fee assumptions outlined above:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

As Mr. Greenblatt would say, “gee, that’s interesting.” Long cheap, short expensive works, but you can expect to nearly go bust along the way. As I told my cable guy recently, “that’s not the deal that I signed up for.” So much for the seemingly sophisticated hedging techniques and “hedged” risk. What’s the point of a big short book if it doesn’t protect you from the big drawdowns? A -52.01% drawdown isn’t low-risk on any planet I’m familiar with, and in fact this strategy has an even worse drawdown than long-only market exposure. Wes and I outline just how risky many “anomaly” strategies can be in a long/short context.

The large maximum drawdown occurs during the internet bubble (5/1/1998 – 2/29/2000), which is a bad period to be long value stocks and short growth stocks.

Will there ever be another internet bubble? Who knows? But investors should be aware that if they face similar market conditions, they can expect to lose over half of their money in the long/short strategy proposed by Gotham, or in investments with any manager peddling long cheap, short expensive type strategies.

Is there a way to improve the Long Cheap/Short Expensive strategy?

One suggestion would be to go the cheaper route, and form a DIY portfolio, as opposed to paying 2% management fee.

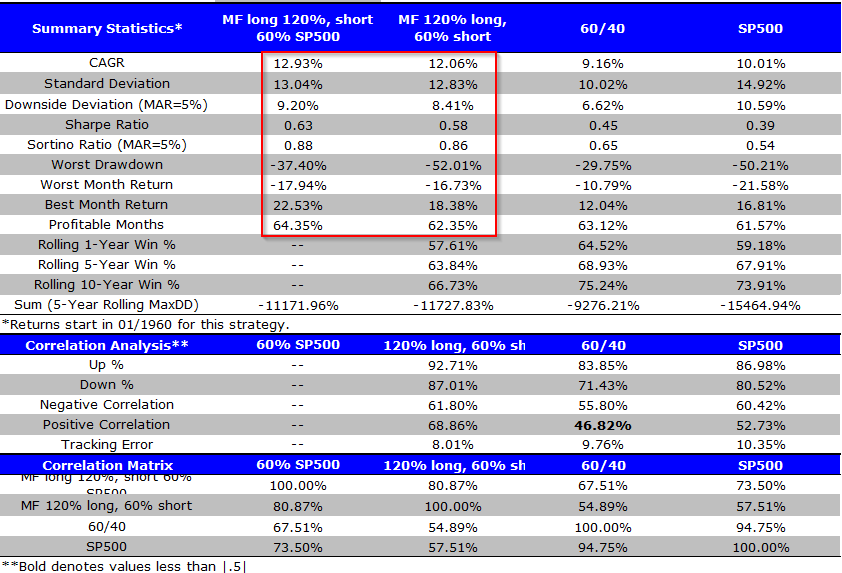

Another option is to simplify the approach and build the portfolio by going long the top quintile of cheap names (120% exposure) and shorting the SP500 (60% exposure). We assume a 0.25% short rebate and a 0.20% annual transaction cost, as we only need to rebalance the long portfolio annually, and shorting with a SP500 future has minimal costs.

Here are the returns from 1/1/1960-12/31/2013:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The simple DIY strategy is better on any performance metric. The DIY approach (first column) has a higher CAGR, Sharpe and Sortino ratios, and a lower maximum drawdown.

Overall, the Magic Formula Long/Short strategy is not bad by any measure, but is by no means a free lunch. In time periods such as the internet bubble, losing half of your money seems quite possible.

The fees (2%) are extremely high, and a simple DIY strategy would seem to give better risk-adjusted returns and has the benefit of being relatively easy to implement.

If additional fees (such as fees from brokerage houses) are added on top of the 2% management fee, the DIY option may be worth the headache of implementing such a strategy.

Last (and maybe most important), the mutual fund setup of Gotham means taxes will be distributed each year, so after-tax returns will, in general, be lower.

About the Author: Jack Vogel, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.