We have discussed market valuations in the past, but the issue of market valuations was recently raised on CNBC, when Robert Shiller suggested he may shift out of the US and buy Europe.

When Shiller speaks, we listen. In the past, his predictions have actually been somewhat predictive–a rare feat!

We reran the numbers to assess the current landscape.

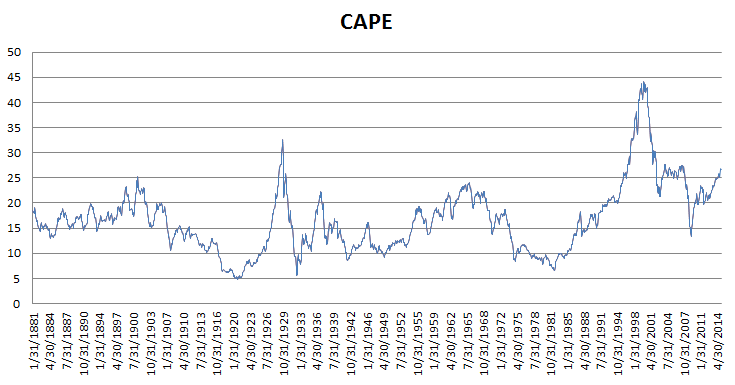

Current CAPE ratio:

Based on a review of the Shiller CAPE index (shown below – data from Shiller’s website and the Federal Reserve website), the market certainly appears to be expensive. As of 1/31/2015 the CAPE index is in the 94th percentile based on the past 133 years of data!

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

But what about alternatives to investing in stocks?

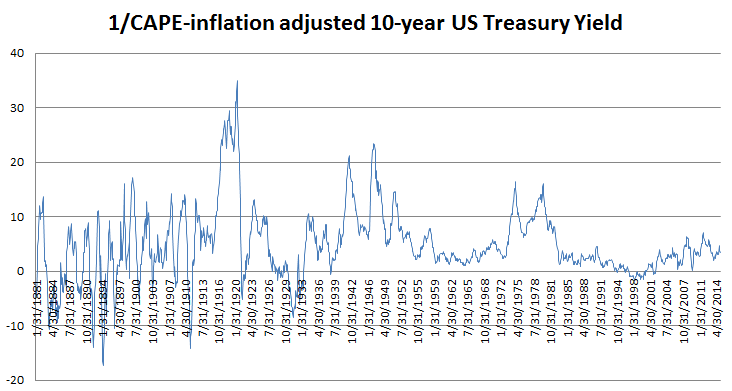

What yields can be had in other asset classes? Bonds seems like a reasonable place to start. Let’s compare our stock market yield versus what we can get on a 10-year treasury bill. To calculate stock market yield we use the inverse of the CAPE index (1/CAPE).

If we take the “stock market yield” (1/CAPE) and subtract the inflation adjusted 10-year U.S. Treasury yield, we can examine how expensive the market is relative to the bond alternative (a stock investor would prefer a higher spread, all else being equal). The inflation adjusted yield is calculated as the 10-year yield minus inflation, where inflation is measured as change in consumer CPI year over year.

The spread between stocks and bond yields is presented below:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The figure above is not screaming overvaluation for stocks. The current “excess” yield over the inflation-adjusted US Treasury rate does not appear too high, when compared to historical excess spreads.

In fact, the current value of 3.37% is slightly below the median value of 3.49%, falling in the 49th percentile. The results are similar if we look at the spread between 1/CAPE and the 10-year U.S. Treasury yield (44th percentile).

So if bonds are your risk-free alternative to stocks, then the market does not appear to be extraordinary expensive on a relative basis. The risk premium for taking on equity risk is roughly the same it has been historically.

Of course, some market participants argue that bond yields don’t represent “market prices” because they are manipulated by governments. The argument is that bond yields should be higher than they currently are priced–a reasonable conjecture. And in this case, perhaps stocks are overpriced. But market participants aren’t price-makers, they are price-takers–especially when it comes to government bonds. So in order to make an argument that the current valuation of stocks relative to bonds is unreasonable because bond prices are “fake,” we have to simultaneous outline an argument that governments will no longer play a role in setting bond prices. This seems unlikely, but as is the standard case, anything is possible!

About the Author: Jack Vogel, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.