Trading on Noise: Moving Average Trading Heuristics and Private Investors

- Etheber, Hackethal and Meyer

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

We use a comprehensive dataset from a German discount brokerage firm to investigate both the prevalence and effects of moving average trading heuristics among individual investors. We document an abnormal increase of 30% in individuals’ trading volume on signal days. More than one in 10 investors repeatedly places trades according to these heuristics. However, abnormal returns from technical trades are found to be insignificant. Hence, our results are consistent with the interpretation that some individual investors — contrary to the factual evidence — believe in these signals and to that extent trade on noise.

Alpha Highlight:

At the mention of technical analysis, some market observers will start yelling “heretic!” Despite the hate and discontent surrounding technical rules, technical analysis has been widely used by both professional and individual investors for decades. These investors believe technical signals can predict future prices by extrapolating past price patterns. Technical methods also give investors the illusions of knowledge, control, and objectivity in their trading decisions (Barber and Odean, 2002).

One simple technical rule is the Moving Average. This paper re-examines a popular question:

Does the MA trading signal contain exploitable value-relevant information, or just noise?

To answer this puzzle, the authors divide their research into addressing two specific questions:

- Do individual investors apply the MA rule?

- Does the MA rule help individual investors make better trades?

The samples in this paper are approximate 2.7m transactions made by more than 35,000 investors from 01/2004 to 11/2011. Data come from a German discount brokerage dataset. Each investor’s detailed trading history can be tracked in this dataset.

The paper groups investors into “chartist” and “non-chartist” using two approaches: Binomial classification and simulation-based classification. Binomial classification is based on investors’ real transaction records. To be specific, those investors who are more likely to systematically use MA rules for their trading decisions are classified as “chartist.” Simulation-based methods are a little bit more complex (we omit the details here). If you are interested, please refer to Section 4.1 in the paper.

Key Findings:

On signal days, individuals’ trading activity is about 30% higher than usual. This shows that private investors do trade on MA rules as if these signals contained value-relevant information.

A substantial amount of individual investors trade on behalf of MA heuristics. Based on their actual transaction records, 10-15% of sample investors are classified as “chartists.” The paper also finds that these “chartists” share some typical characteristics in common:

- They trade substantially more often and hold less diversified portfolios than other investors do;

- Investors with lower levels of investment experience and education are more likely to rely on MA rules.

Table below presents the performance differences (measured by intercepts of Carhart 4-factor regressions) between “chartists” and “non-chartist.” We can see that “Chartists“seem to be more skilled at stock trading over shorter horizons, but their performances are not statistically better over longer horizons.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

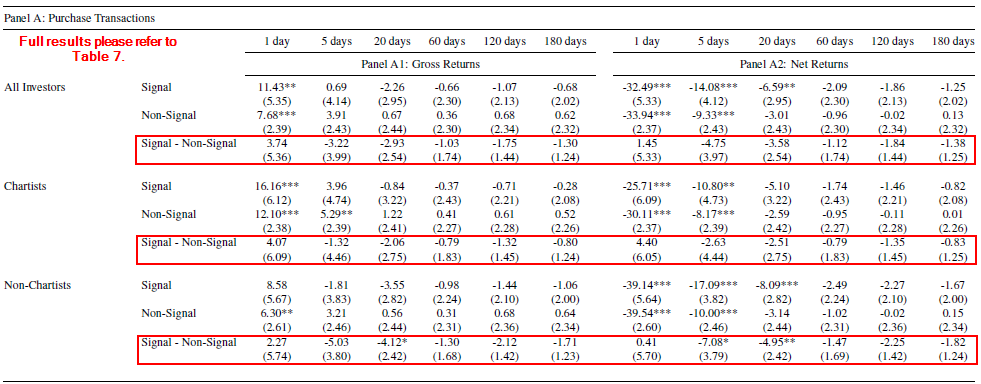

In this next step, the paper investigates whether the skills of “chartists” are associated with their tendency to systematically trade on MA trading signals. The paper examines the performance differences of “signal” transactions and “non-signal” transactions (“signal” transactions are trades on the signal days).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The table above shows that trading based on MA rule does not give individual investors distinguishable benefits. This is likely due to the increased trading, which is associated with higher transaction costs. Results further show that after taking brokerage commissions into account, “chartists” earn significantly lower returns than “non-chartists” (about 0.1% per month).

Also of interest is the examination of how “chartist” follow buy and sell signals from trend-following rules. Not surprisingly, many investors don’t religiously follow their models. A quote from the paper:

Overall, our results indicate that private investors put more decision weight on heuristics’ sell signals than on heuristics’ buy signals…

In other words, the so-called chartists don’t actually follow the model. They pick and choose. Selling is the easy decision, but buying back into the market becomes a “gut” decision. And of course, when lizard brain gets involved, the system no longer works. No surprise there…

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.