- Title: FACTOR BASED INVESTING: THE LONG TERM EVIDENCE

- Authors: ELROY DIMSON, PAUL MARSH, AND MIKE STAUNTON

- Publication: THE JOURNAL OF PORTFOLIO MANAGEMENT, 2017, SPECIAL ISSUE (version here)

What are the research questions?

- Is there out-of-sample (OOS) evidence for factor investing?

What are the Academic Insights?

By studying a data set including 23 countries and over a long time frame (1926 for the US and 1955 for the UK and on average 43 years for other countries), the authors find:

- The concept of the size effect was introduced by Banz (1981) documenting a monthly 1% premium of small cap stocks compared to large cap stocks. The authors find a diminished premium: 0.32% monthly for the longest average period and 0.45% monthly from 2000 to 2016.

- The concept of the value effect was introduced by Rosenberg et al. (1985) documenting a yearly 4% premium of value stocks compared to growth stocks. The authors find a diminished premium: 2.1%% yearly for the longest average period and 2.5% yearly from 2000 to 2016. Additionally, they warn that the value premium can come in erratic patterns. (see here for more info)

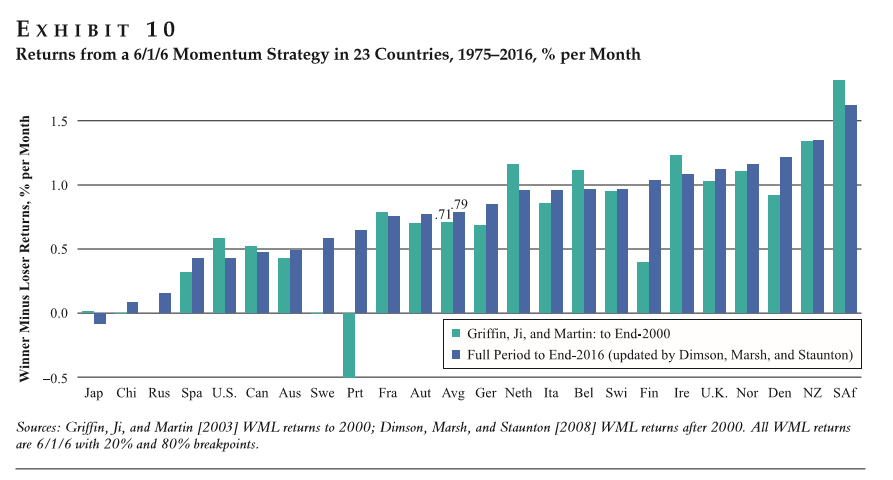

- The concept of the momentum effect was introduced by Jegadeesh and Titman(1993) documenting a monthly 1% premium of past winning stocks compared to past losing stocks. The authors find a fairly consistent premium: 0.71% monthly for the longest average period and 0.79% monthly from 2000 to 2016.

Why does it matter?

In general, the issue of data-mining may contaminate the statistical results from backtesting that underlie factor investing. The use of out-of-sample universes to test results obtained with US-only data sets is an important advance in testing the robustness of various factors and the associated return performance.

- Based on this research, the size premium is lower than originally thought. However, after considering the risks, illiquidity and transaction costs of investing in small-cap stocks, there at least seem to be no case to underweight them.

- The value premium has been lower in the US than originally documented. Outside the US, it is stronger and more persistent.

- With the caveat that momentum premium can go through periods of substantial underperformance and drawdowns, it (in the words of the authors) “can generate a disturbingly large abnormal return.”

The Most Important Chart From the Paper:

Elisabetta Basilico, Ph.D., CFA, (@ebasilico) is an independent investment consultant. With co-author Tommi Johnsen, PhD, she is writing an upcoming book on research backed investing. You can learn more at http://academicinsightsoninvesting.com/

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.