This past week we had the honor of hosting the first annual “Democratize Quant Conference” with our friends at Villanova University (a link to the conference site).

Despite Mother Nature’s best attempts to kill our mojo, we managed to rally a packed room. We also had nearly 30 guests at our house the night prior to the conference. These “hard-chargers” were able to park in our snowmobile lot, which had plenty of parking.

Luckily,although the original dinner was canceled, we had a “sunk cost” in the form of a keg of beer and the local pizza joint was willing to keep operations humming.

The picture below was fairly interesting. Readers should take note of a few interesting items:

- There are a lot of PhDs at the table, except for one individual we picked up off the street named Corey Hoffstein.

- There are equal parts women and equal parts men in the picture. On an IQ-weighted basis, we are certainly overweight females.

- Chris Hempstead and Chuck Bates managed to photobomb our pic. Note the red flip cup in Chris’s hand. Money good.

Dining Table from Left to right: Liquan Ren PhD, Elisabetta Basilico PhD, Corey Hoffstein, Linza Zhang PhD, Wes Gray PhD, and Niki Boyson PhD Photobombers from Left to Right: Chuck Bates and Chris Hempstead

The next morning we kicked off the conference, and to our surprise, over 50 people still showed up!

Eric Balchunas (Bloomberg) kicked things off with an absolutely wonderful discussion of the ETF industry.

His talk “Welcome to the Jungle” was an excellent way to get things rolling.

Ryan Kirlin (Alpha Architect) discussed Eric’s core ideas and added one of his own — ETF fragility as measured by a normalized Herfindahl-Hirschman Index.

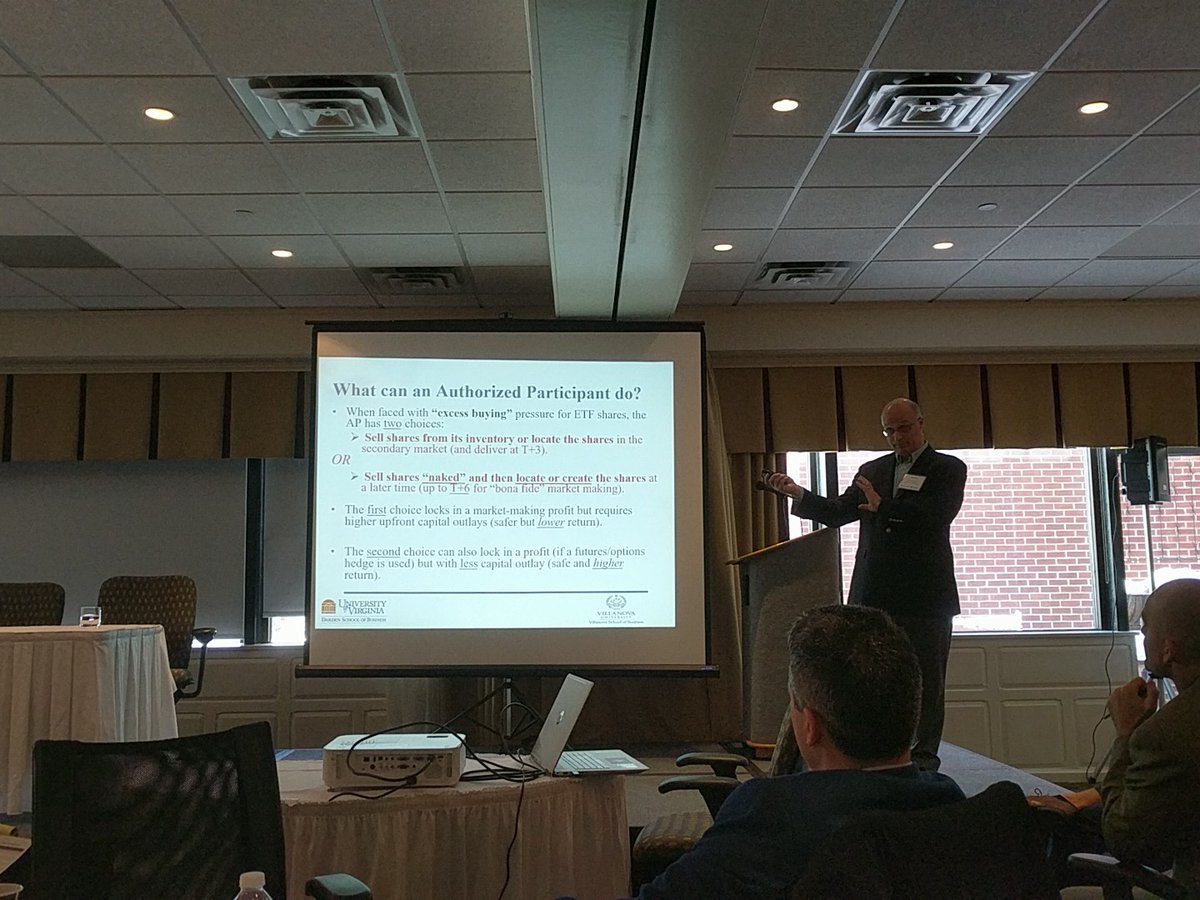

Next up was Mike Pagano, a tenured professor at Villanova and a card-carrying finance professor. Mike did a deep dive describing ETF short interest and failures to deliver. On one hand, FTD are good for ETF liquidity, but there is a remote possibility that they cause systematic risk.

Jack Vogel (Alpha Architect) discussed Mike’s result and stressed how interesting and useful the paper is for those looking to learn more about the nitty-gritty details of ETF trading operations.

We ended the ETF trading discussion with 3 of the world’s experts on the topic — Chris Hempstead (DB), Bryan Johanson (RBC), and Reggie Browne (Cantor) — in a discussion moderated by Mike Pagano.

The weather threw a wrench in our plans and our keynote speaker — Vinay Nair — was stuck in Utah. I attempted to fill-in at the last minute and address the question of “Why do strategies work in the first place?” The crowd was on the tip of the toes hoping I would have the answer…pretty sure I failed, but I gave it a good-faith effort until they kicked me off stage.

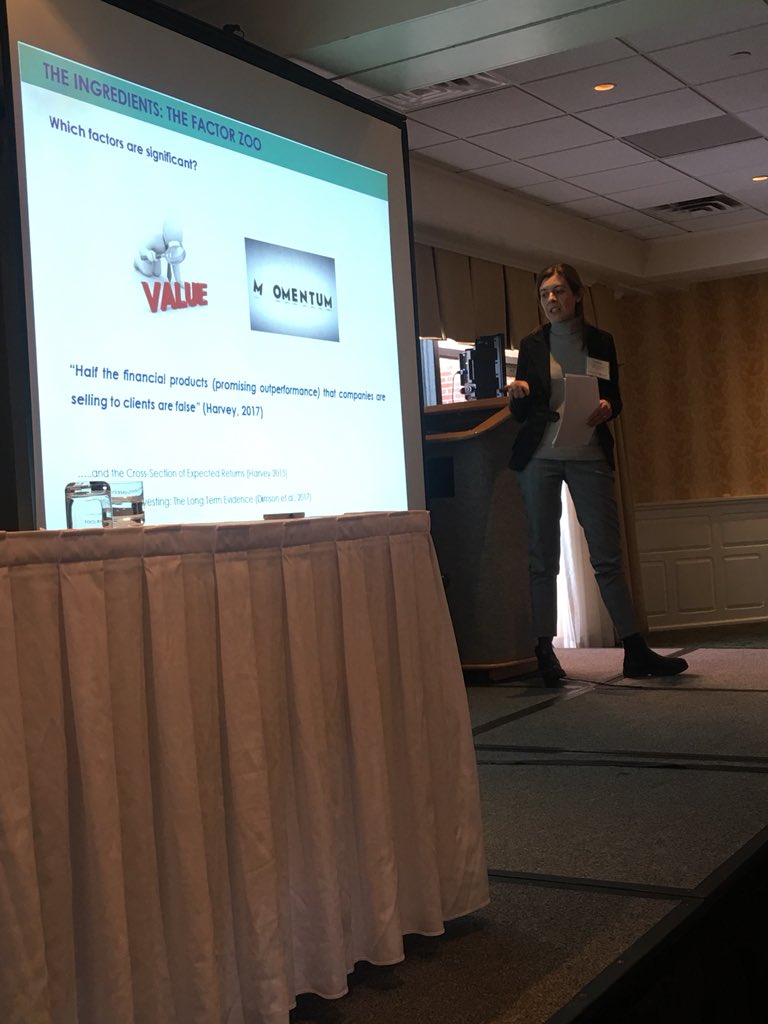

In the afternoon we switched gears to factor investing. Tammira Philippe, the President of Bridgeway, came in with her education guns blazing. We all walked away with a better sense of which factors matter and why.

Next up was Chris Meredith from O’Shaughnessy Asset Management. Talk about a rock-star. Chris did an incredible job complementing the chat from Tammira. A must follow on twitter if you aren’t following him already.

Post factor chat came the always entertaining Corey Hoffstein from Newfound Research. Corey cranked up the brainwaves and started tossing equations at the rapid rate. But the crowd was able to handle the barrage of knowledge and walked away a lot better for it. After describing “timing luck,” this became the topic of discussion for all breaks thereafter!

Elisabetta Basilico, who held the conference record for the most dedicated traveler (she came all the way from Italy!), did an excellent job summarizing Corey’s work and asking important questions about some of the assumptions in Corey’s timing luck model. Excellent stuff, as usual, from Elisabetta.

Next up was Jeremy Schwartz and Jeremy Siegel. Prof. Siegel was stuck in Toronto but we put together some quick IT to make it happen. The Jeremy^2 interview was absolutely incredible. From finding out that Siegel’s mother was a “communist” and “that he didn’t like that too much”, to listening to the fact that this guy has studied under (and alongside) just about every Nobel Prize winner on the planet. Incredible. And his ability to convey complex information and macro forecasts in a simple and easy to understand format is breathtaking. Of course, having a great moderator with Jeremy Schwartz doesn’t hurt!

One problem with the “Jeremy Squared” presentation — we forgot to record the video — so we’ll have to get that fixed for next year!

Finally, we saved the best for last. Barry Ritholtz fought through the blizzard and made his way down to Philly to present some new material on “The Fine Art of Failure.” I was blown away as usual by Barry’s charisma and ability to synthesize so much knowledge into a few key learning points. Thanks, Barry!

To say that the first annual conference was a success would be an understatement — the event went way better than expectations! Thank you to all our presenters and attendees for braving the elements to join us! See you all again next year, minus the blizzard!

| Time | Event | Lead Faculty |

|---|---|---|

| 9:00 | Registration and Coffee Session | N/A |

| 9:40 | Dean’s Welcome and Opening Remarks | Villanova Dean |

| 10:00 | The Future of the ETF Landscape / Discussant Slides | Balchunas/Kirlin |

| 10:50 | Break | N/A |

| 11:15 | Understanding ETF Market Structure / Discussant Slides | Pagano/Vogel |

| 12:05 | Break | N/A |

| 12:20 | Moderated Panel | Pagano & Panelists |

| 12:50 | Lunch/Keynote | Nair (Wes filled in) |

| 2:10 | The Factors that Matter / Discussant Slides | Philippe/Meredith |

| 3:00 | Break | N/A |

| 3:30 | How to Use Factors / Discussant Slides | Hoffstein/Basilico |

| 4:20 | Break | N/A |

| 4:40 | Moderated Panel | Ren & Panelists |

| 5:10 | Break | N/A |

| 5:25 | Fireside Chat (not available) | Siegel/Schwartz |

| 5:55 | Closing Remarks | Gray |

| 6:00 | Reception | N/A |

| 7:00 | Dinner Slides | Ritholtz |

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.