Thematic Indexing, Meet Smart Beta! Merging ESG into Factor Portfolios

- Jennifer Bender, Xiaole Sun, and Taie Wang

- Journal of Index Investing, 2017

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

- Is the relationship between ESG and factor stable over time?

- How should blended ESG-factor portfolios be constructed? In particular, should ESG be incorporated as an additional factor or used to screen the universe?

What are the Academic Insights?

By studying the MSCI World universe, 5 risk premia ( value, momentum, size, quality and low volatility) and MSCI ESG ratings, the authors suggest the following:

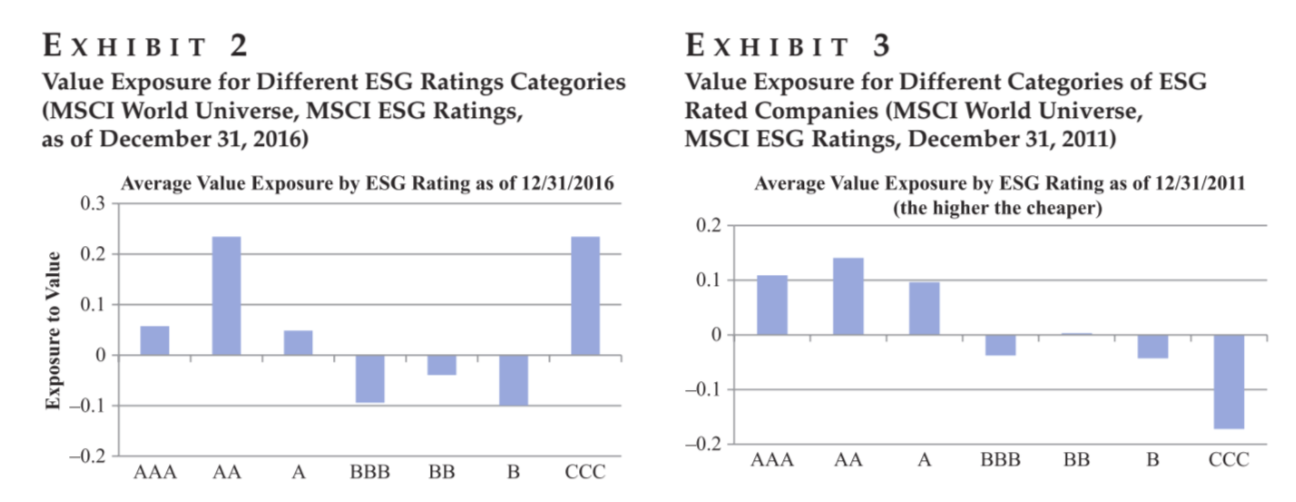

- NO- the relationship between ESG and factor characteristics is likely to change over time and particularly for factors like value and momentum, which are cyclical.

- There are mainly two approaches:

- rules-based or heuristic portfolio construction

- optimization based portfolio construction, which is most effective when the objective is to maximize factor exposures while minimizing risk and controlling for other objectives

The authors suggest that, in case of ESG integration, solution b is preferable. With regards to the question on whether to screen the universe of treat ESG as an additional factor, the authors show that each approach has its pros and cons. The screening approach is the most straightforward and the one with the best performance because it is the one with the least constraints. Its cons are that it may not yield a positive ESG portfolio exposure. The optimization approach maximizes the exposures but if ESG metrics don’t have additional alpha, it will tend to detract from absolute risk-adjusted performance.

Why does it matter?

This article argues that the correct way to integrate ESG and factor exposures depends on the investor’s investment rationale and, in particular, his or her desired exposure, performance expectations, and preference for conceptual consistency.

The Most Important Chart from the Paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Many investors are starting to explore ways to integrate environmental, social and governance (ESG) considerations into their portfolios. Factor portfolios and indices which integrate ESG allow investors to capture both the long-term durable factor premia while allowing them to invest in companies with attractive ESG attributes. Traditional factors and ESG both have strong investment rationale for investors with long horizons. But how should blended ESG-factor portfolios be constructed? This paper discusses several ways in which to integrate ESG in factor portfolios. We show that the choice of which approach depends on the investor’s investment rationale behind integrating ESG, desired exposure, performance expectations, and preference for conceptual consistency.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.