Leveraged ETFs: Are you prepared for the Volatility Jumps?

- Linda Zhang

- Journal of Index Investing, Summer 2018

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the Research Questions?

- What has the absolute risk behavior of leveraged products been historically? Did they behave as intended by design?

- Is the leverage multiple a reliable indicator of the volatility multiple?

- Is the leverage multiple a reliable indicator over shorter horizons?

What are the Academic Insights?

By studying the empirical evidence of the top 10 largest products from 2012 to 2016, the author finds the following:

- YES- The top 10 largest levered products appear to deliver magnified gains and losses, as intended, over the entire sample period

- YES- The leverage multiple appears to be a reliable indicator of the volatility multiple. For instance, the largest ETF ProShares two-times-short S&P 500 had the volatility of 1.64% over the entire five-year period while its 1X product SPY’s volatility was of 0.83%. The ratio over the five-year period is roughly 2, just as the leverage multiple suggested

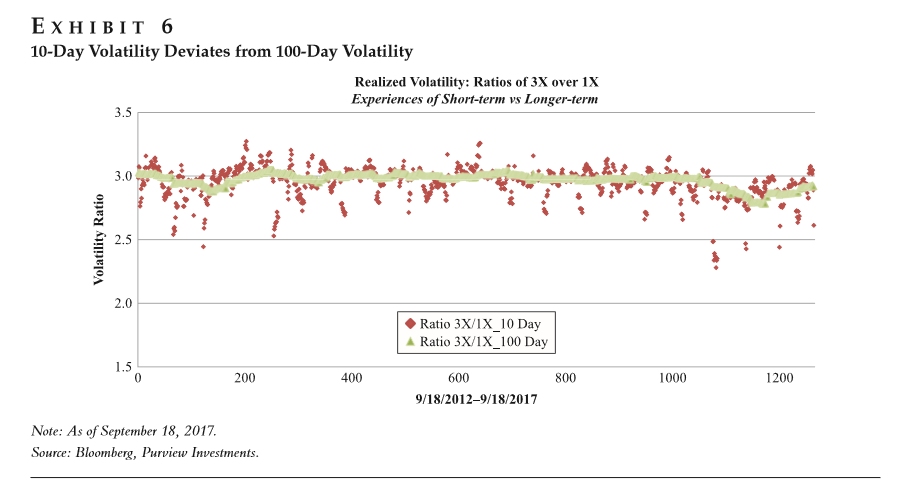

- NO-By analyzing the 3X ETF (UPRO), versus the 1X ETF (SPY), over the shorter 10-day period, the volatility ratio can deviate significantly from the indicated leverage multiple. The 3X product’s volatility can be as high as 3.3 times that of the 1X product. Among the many rolling windows, the volatility ratio has exceeded the leverage ratio many times. In fact, the author estimates that about 30% to 33% of the time, investors experienced higher volatility with leveraged ETFs than they were designed to have. Despite that, most high-volatility ratios fall within a reasonable two-standard-deviations range

Why does it matter?

This study provides an updated look at the leveraged and inverse global ETFs offerings. It alerts investors on the risk and return characteristics of these products, which are riskier than their one-time long-only counterparts. Specifically, their short-term risk characteristics can be even more volatile than the leverage multiple suggests.

Investors must grasp a full understanding of the complex risk behaviors of these instruments for effective use in their investment strategies. They need to be prepared for the jump in volatility in leveraged ETFs that may arise at the moment when they most need to avoid it.

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Leveraged and inverse ETFs represent one of fast growing areas in the ETF industry, with the global AUM breaking $60 billion. The regulatory bodies in many countries are approving the listing of these products. The recent financial market turmoil in February 2018 has exposed the risk behavior of these ETFs in the time of market stress, which are often misunderstood by investors and can catch them by surprise. In this study, we analyze leveraged ETFs risk profiles in both short-term and long-term periods. As leveraged ETFs and inverse ETFs are often used for short-term trading purposes, understanding the nature of short-term volatility is highly critical. We also survey the landscape of the major markets with listed leveraged ETFs outside the U.S., including Asia Pacific and Canada. We examined the volatility behavior of leveraged products in these markets and came to the same conclusion. The near-term volatility jumps more than what the leverage ratio suggested. We’ve also noticed the degree of jumps vary from market to market. Globally, leveraged and inverse ETFs are growing at a healthy pace, led by a faster growth in Asia in 2016. After Japan, South Korea, and Taiwan, Hong Kong became the latest market, allowing both inverse and leveraged products on Hong Kong and China stock indexes. It is in the great interest of global investors to fully understand the nature of these instruments to use them effectively in portfolio management.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.