Public Hedge Funds

- Lin Sun and Melvyn Teo

- Journal of Financial Economics, forthcoming

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

In recent years, there have been a few public listings by mega asset management firms including Amundi Group, Man Group, Fortress Investment Group, Och-Zi Capital Management Group, Blackstone Group, and KKR. These publicly listed mega asset managers together managed an impressive US$2.38 trillion in 2017.

The authors investigate the following research question:

- How does the transition to public equity markets impact investment performance of hedge funds?

What are the Academic Insights?

The authors shed light on a number of potential agency issues (the conflicts between management and fund investors and those between shareholders and fund investors) by investigating the impact on hedge fund performance when asset management firms go public. The potential for agency problems is greater for hedge funds than for mutual funds because of the more complexity and lower levels of transparency and disclosure associated with hedge funds.

They find the following:

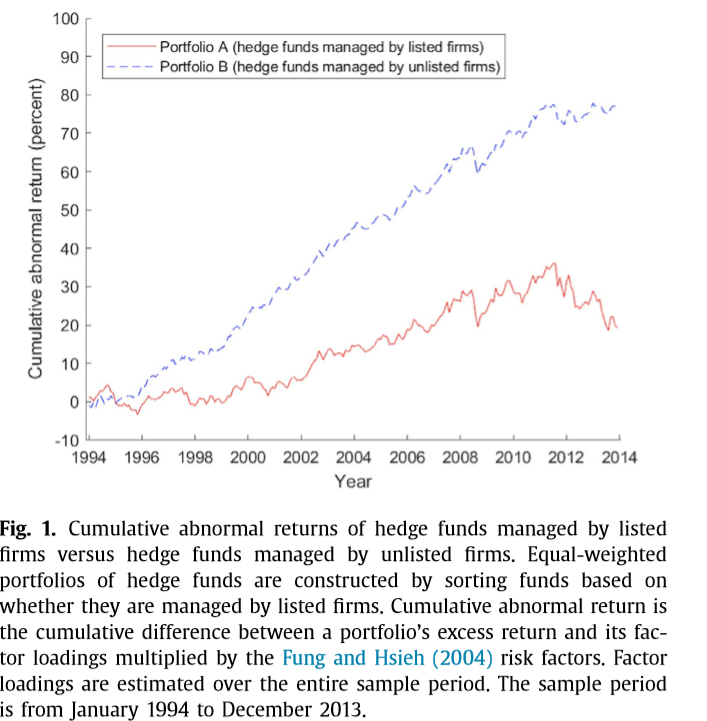

- There are substantial differences in expected returns on the portfolios of hedge funds sorted by fund management company listing status that are unexplained by the Fung and Hsieh (2004) seven factors. Hedge funds managed by listed firms underperform hedge funds managed by unlisted firms by 2.89% per year (t-statistic = 4.73) after adjusting for co-variation with the Fung and Hsieh (2004) seven factors. The results are not confined to the smallest funds in our sample and cannot be explained by differences in share restrictions and illiquidity, incentives, fund age, fund size, return smoothing behavior, backfill and incubation bias, and manager manipulation of fund returns. Additionally, using a difference-in-differences analysis, the authors find that relative to the five-year pre-IPO period, average fund risk-adjusted performance deteriorates by an annualized 8.40% while average firm alpha wanes by an annualized 7.20% during the five-year post-IPO period. Despite the post-event underperformance, public firms harvest annual fee revenues that are US$17.28 million or 54.96% greater than do comparable private firms. This is because relative to the control group, public firms are able to grow their assets under management (henceforth AUM) by US$617.62 million or 77.52% during the same period.

Why does it matter?

The results in this paper challenge the view that asset management firms list to enhance investment performance. Asset allocators should take note.

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

Hedge funds managed by listed firms significantly underperform funds managed by unlisted firms. The underperformance is more severe for funds with low manager deltas, poor governance, and no manager co-investment, or managed by firms whose prices are sensitive to earnings news. Notwithstanding the underperformance, listed asset management firms raise more capital, by growing existing funds and launching new funds post listing, and harvest greater fee revenues than do comparable unlisted firms. The results are consistent with the view that, for asset management firms, going public weakens the alignment between ownership, control, and investment capital, thereby engendering conflicts of interest.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.