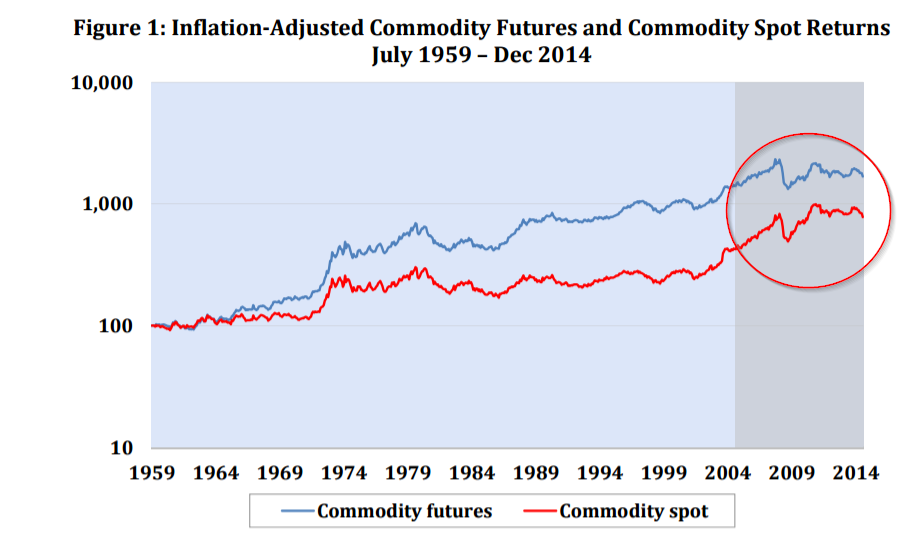

Commodity Futures Investing: Complex and Unique

By Wesley Gray, PhD|December 21st, 2016|

Commodity futures investing is arguably the most misunderstood asset class in the financial marketplace. We want to change that [...]

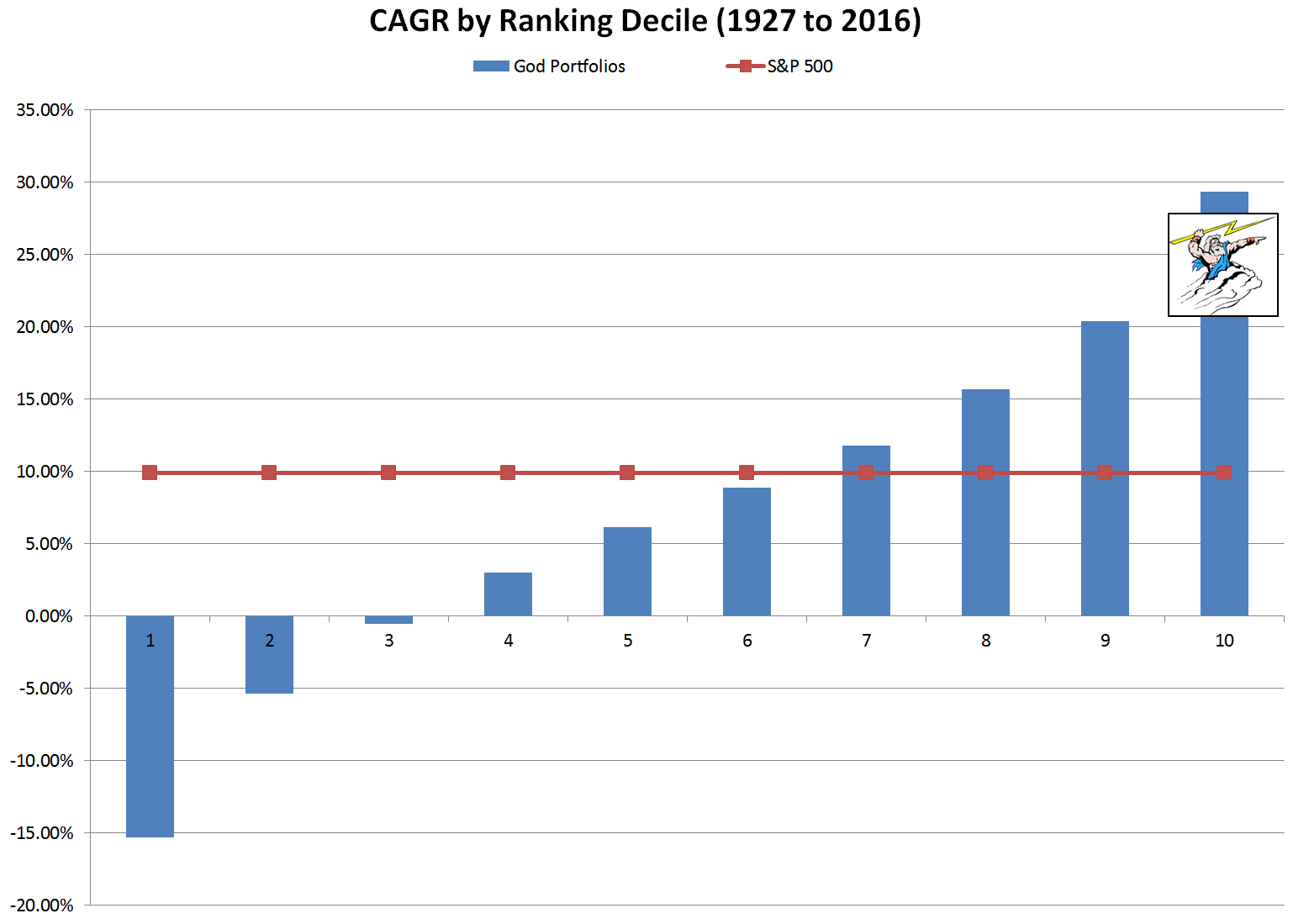

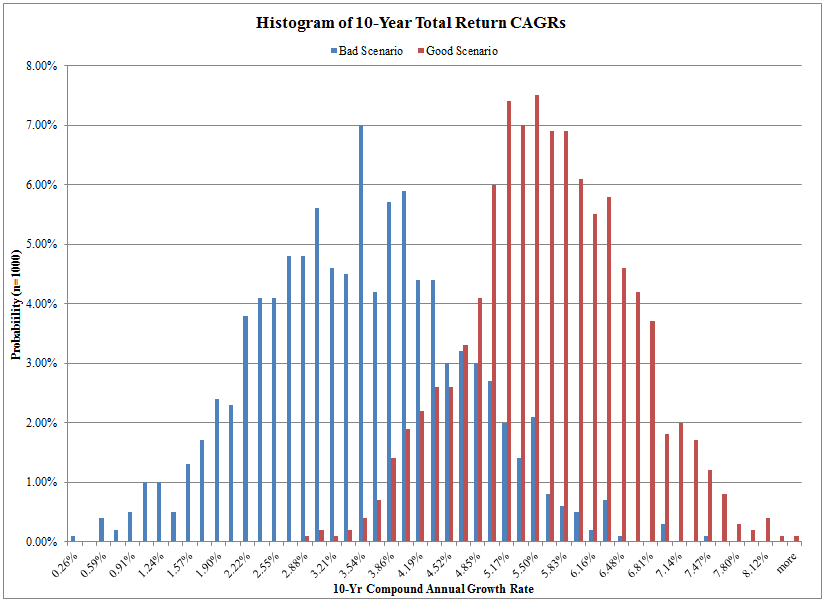

Even God would get fired as an Active Investor

By Wesley Gray, PhD|February 2nd, 2016|

Perfect foresight has great returns, but gut-wrenching drawdowns. In other words, an active investor who was clairvoyant (i.e. [...]

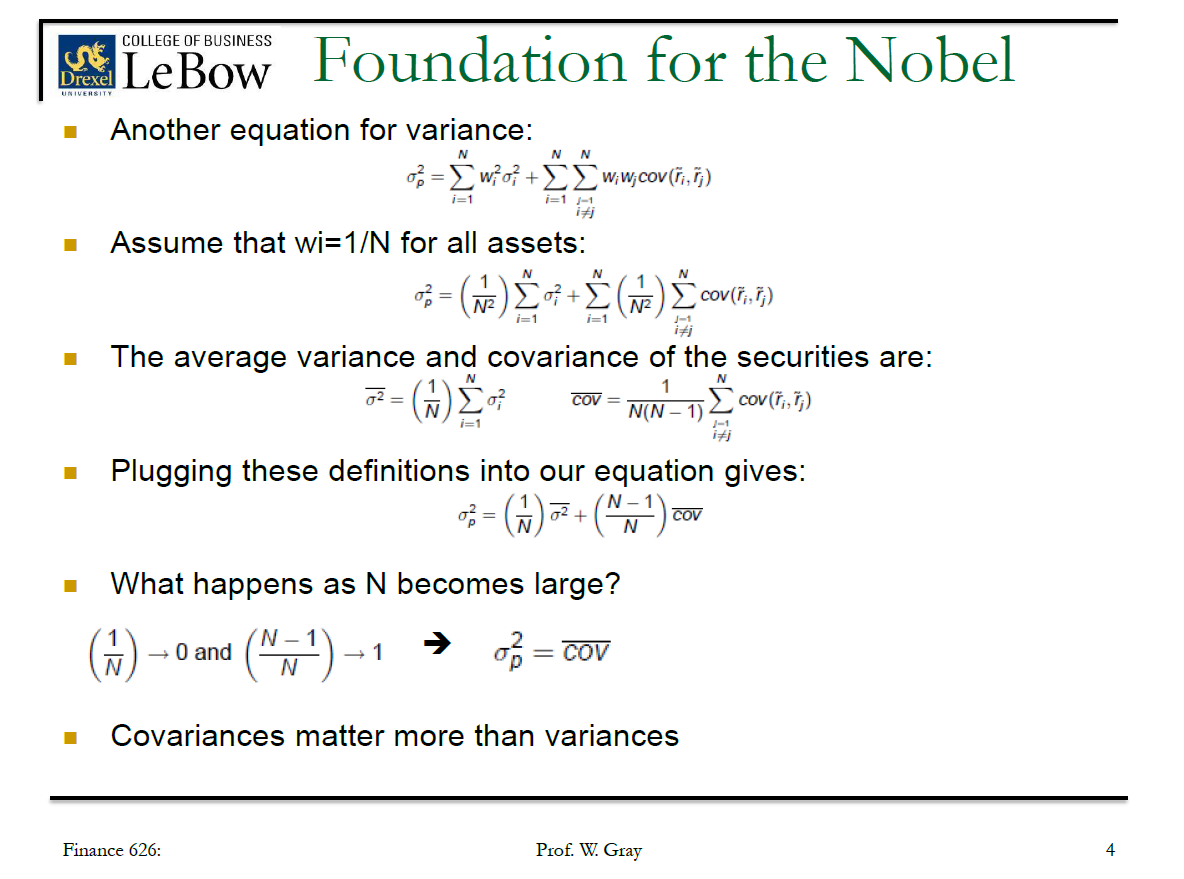

The Quantitative Momentum Investing Philosophy

By Jack Vogel, PhD|December 1st, 2015|

Eugene Fama, the 2014 co-recipient of the Nobel Prize in Economics and father of the efficient market hypothesis, [...]

How to Use Factor Funds in a Diversified Portfolio

By Jack Vogel, PhD|September 30th, 2015|

Active management has been out of favor for a while--high fees, high tax burdens, and poor long-term performance. [...]

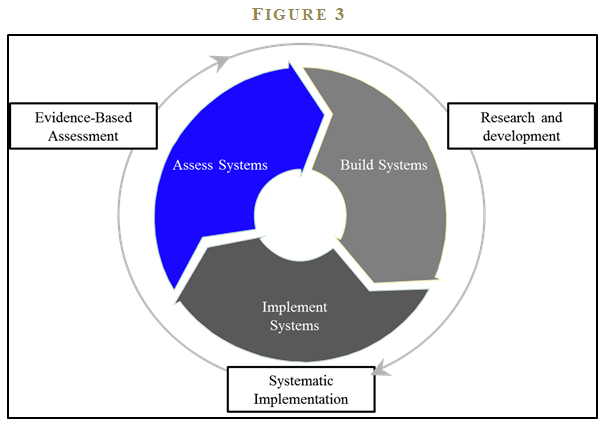

The Sustainable Active Investing Framework: Simple, But Not Easy

By Wesley Gray, PhD|August 17th, 2015|

We cannot overemphasize that identifying sustainable alpha in the market is no cakewalk. More importantly, being smart, having superior stock-picking skills, or amassing an army of PhDs to crunch data is only half of the equation. Even with those tools, you are still only one shark in a tank filled with other sharks. All sharks are smart, all sharks have a MBA or PhD from a fancy school, and all the sharks know how to analyze a company. Maintaining an edge in these shark infested waters is no small feat, and one that only a handful of investors has accomplished. In order to achieve sustainable success as an active investor, one needs not only skill, but also an understanding of human psychology, and an appreciation of market incentives (behavioral finance). We start our journey where mine began: as an aspiring PhD student studying at the University of Chicago. Let the adventure begin... This post is not meant to convert a passive investor into an active investor; however, we do explain why we believe active investing can sustainably beat passive strategies in the long run. Plus, we bring to bear many years of cumulative research and experience to support our arguments. We cannot overemphasize that alpha in the market is no cakewalk. More importantly, being smart, having superior stockpicking skills, or amassing an army of PhDs to crunch data is only half of the equation. Even with those tools, you are still only one shark in a tank filled with other sharks. All sharks are smart, all sharks have a MBA or PhD from a fancy school, and all the sharks know how to analyze a company. Maintaining an edge in these shark infested waters is no small feat, and one that only a handful (e.g., we can count them in one hand) of investors has successfully accomplished. In order too achieve sustainable success as an active investing, one needs both skill and an understanding of human psychology and market incentives (behavioral finance). We start our journey where mine began: as an aspiring PhD student studying under Eugene Fama at the University of Chicago. Let the adventure begin...

Avoiding the Big Drawdown with Trend-Following Investment Strategies

By Wesley Gray, PhD|August 13th, 2015|

Simple timing rules, focused on absolute and trending asset class performance, seem to be useful in a downside protection context. Our analysis of the downside protection model (DPM), applied on various market indices, indicates there is a possibility of lowering maximum drawdown risk, while also offering a chance to participate in the upside associated with a given asset class. Important to note, applying the DPM to a portfolio will not eliminate volatility and the portfolio will deviate (perhaps wildly) from standard benchmarks. For many investors, these are risky propositions and should be considered when using a DPM construct.

From the Frontlines to Finance: How the Marines Shaped Our Investment Philosophy

By Wesley Gray, PhD|May 25th, 2015|

Serving in the Marine Corps was an unforgettable experience. Civilians often tell us “thank you for your service”; however, the real “thanks” is due to the Corps for giving us valuable life lessons. The not-so subtle teachings bestowed upon us by heavily muscled, insanely aggressive Marine Corps Drill Sergeants are still, literally, ringing in our ears: “Listen here, pond scum, you better run faster, shoot straighter, and decide quicker if you are going to win in battle!” Years later, we would test that theory in real-time, battling insurgents in Iraq. As we trade in our flak jackets for laptops and neckties, the lessons learned in combat and are not only relevant, but vital on the battlefield of high finance. Four core lessons apply to frontlines and finance: Humans Are Emotional: Systematic processes beat behavioral bias; Rambo isn't Realistic: Act based on evidence, not on stories; Complacency Kills: Focus on fundamentals and never stop learning; Integrity is Everything: Do things right and do the right thing.

Tactical Asset Allocation: Beware of Geeks Bearing Formulas

By Wesley Gray, PhD|May 19th, 2015|

How Should I Tactically Allocate my Assets? A lot of investors ask this question as their wealth grows and [...]

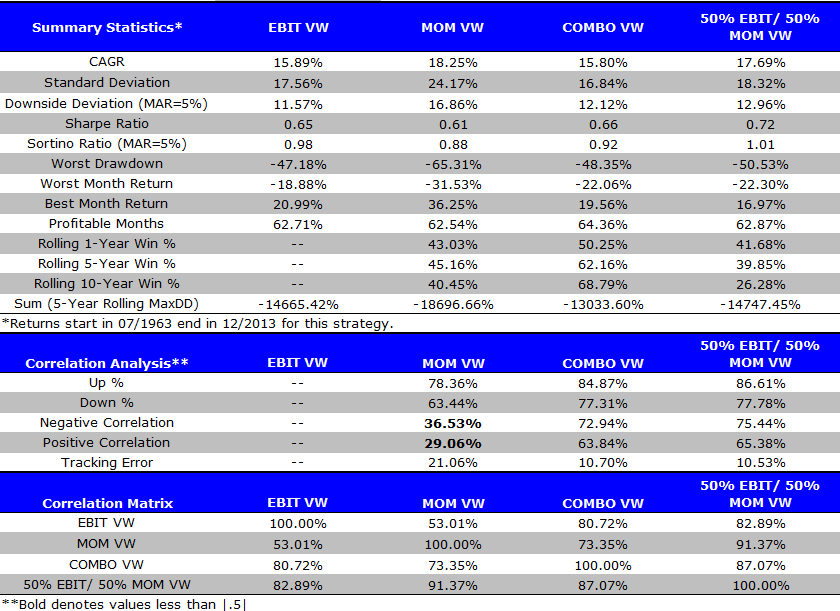

How to Combine Value and Momentum Investing Strategies

By Jack Vogel, PhD|March 26th, 2015|

The evidence suggests that we keep highly active exposures to value and momentum in their purest forms (assuming we are doing high-conviction non-watered down versions of the anomalies). Blending the strategy dilutes the benefit of value and momentum portfolios. The summary of the benefits of a pure value and a pure momentum approach can be summarized as follows: Easier ex-post assessment, stronger portfolio diversification benefits, and stronger expected performance.

Distribution Economics: Understanding Wall Street’s Conflict of Interest Problem

By Wesley Gray, PhD|March 11th, 2015|

The simple matter is that most clients know how to buy groceries, but few know how to purchase financial products. In the murky world of financial services, clients may be buying products for the first time. More importantly, this purchase is the driver of their long-term financial security. Years of hard work, thrift, and responsible life choices, are baked into each and every retirement portfolio that a banker must now serve. In short, the stakes are too high and the cards are stacked too favorably towards one party. Fiduciary responsibility matters in financial services more than in any other product category outside of urgent medical care. Shouldn't this fiduciary have your best interests at heart? Just as you don't want your doctor to receive kickbacks from Pfizer for overdosing you on Oxycodone, why would you want your financial advisor--or their institution--to receive kickbacks for overdosing you on inefficient, overpriced, investment product that probably won't help you achieve your investment goals? Moral of the story: Ask your banker, or bank-affiliated advisor these questions. If you get answers that sound like the ones above, it might be time to buy a car or an airline ticket, because traveling via railroad is a thing of the past.

An Introduction to Investing and How to Use Our Site

By Wesley Gray, PhD|January 3rd, 2015|

What We Do? We are a research-intensive asset management firm with a focus on high-conviction value and momentum factor exposures, [...]

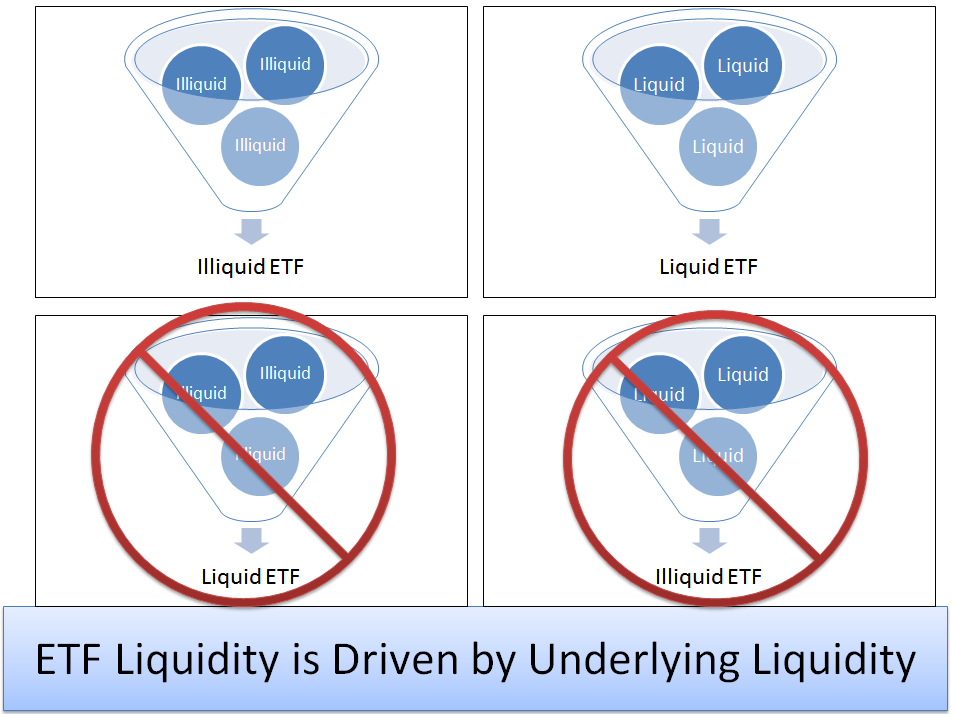

Understanding How ETFs Trade in the Secondary Market

By Wesley Gray, PhD|December 3rd, 2014|

An ETF's liquidity has everything to do with the underlying liquidity of the positions the ETF holds. This has a few implications: Pay attention to the liquidity on the holdings of your ETF--this will explain the spreads in the secondary market; Trade ETFs when the underlyings are liquid--avoid trading ETFs at the open or when overall market volume is lackluster; Avoid huge market orders, and stick to limit orders; Moreover, for huge trades, communicate directly with the market maker or your ETF trading desk.

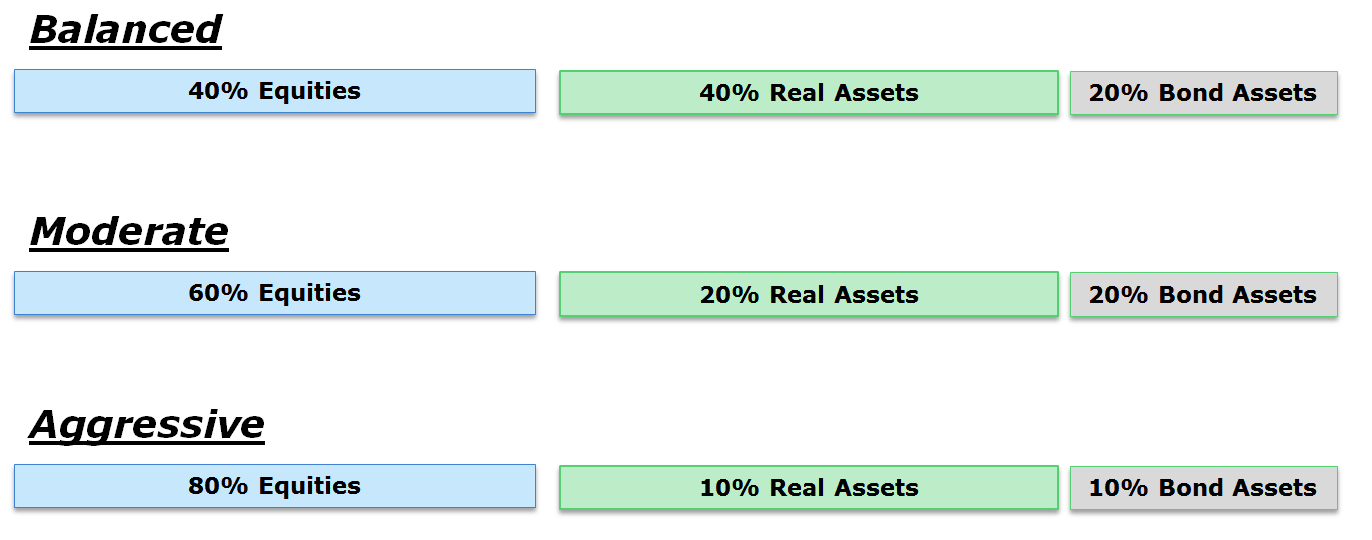

The Robust Asset Allocation (RAA) Index

By Wesley Gray, PhD|December 2nd, 2014|

Robust asset allocation solutions should be relatively simple, minimize complexity, and be robust across different market regimes. Simultaneous to these requirements, the solution must be affordable, liquid, simple, tax-efficient, and transparent, otherwise, many of the benefits of the solution will flow to the croupiers and Uncle Sam. We recommend that investors explore our robust asset allocation framework and go for the do-it-yourself solution. You'll be paying yourself 1%+ a year via saved RIA fees. Is this the only solution? No. But any solution must be robust, simple, tax-manageable, and low-cost. This is our best effort to develop a simple model. Developing a complicated model is easy; simple is difficult.

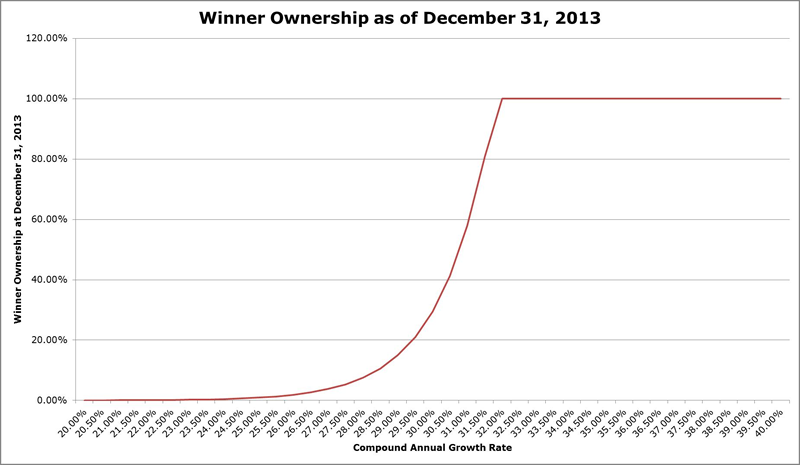

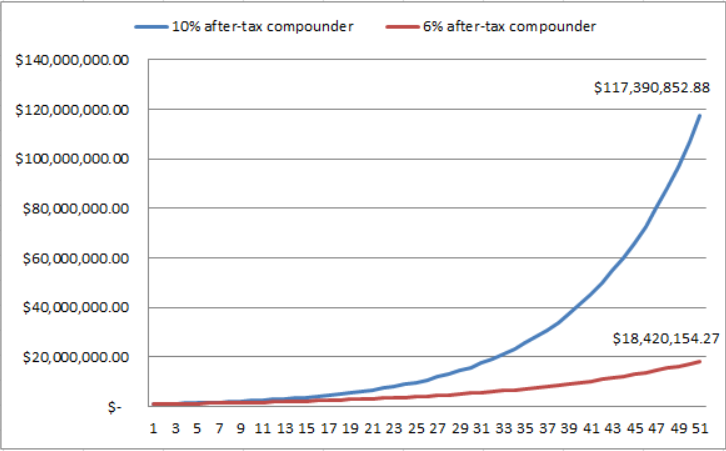

Mission Impossible: Beating the Market Forever

By Wesley Gray, PhD|November 18th, 2014|

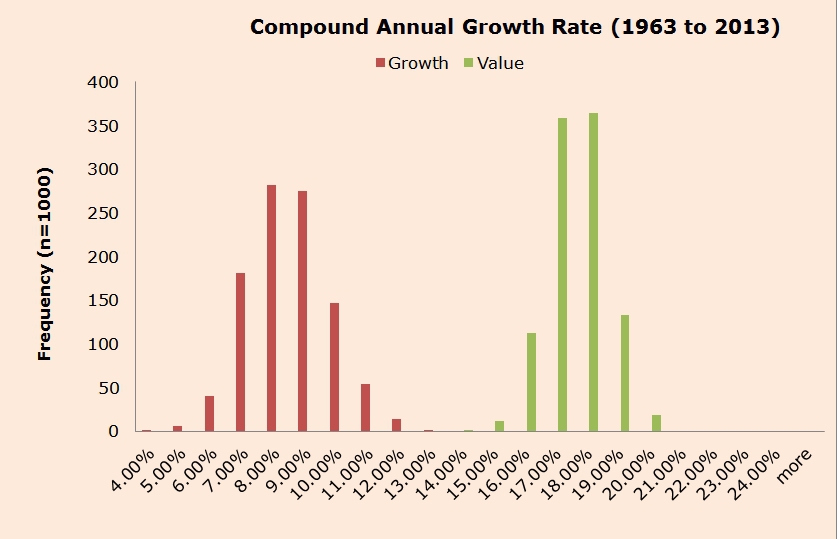

A quick glance at the most recent Berkshire Hathaway annual report (PDF) highlights an amazing data point: Warren Buffett has compounded at 19.7% a year from 1965 through 2013; the S&P 500 Total Return Index has compounded at 9.8% a year from 1965 through 2013. The immediate reaction to these figures is predictable: “Warren Buffett is an investing god, so we should buy Berkshire Hathaway and throw away the keys.” The gut reaction is that Buffett can continue to beat the market forever. Unfortunately, as this post highlights, this is an impossible feat.

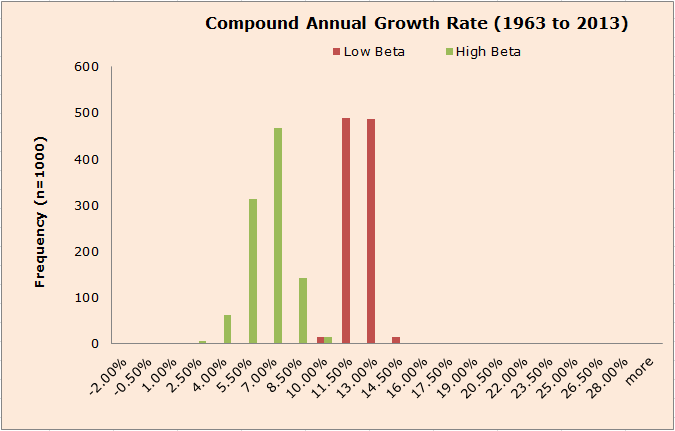

Low-Volatility Investing: Avoid High Beta Stocks. Period.

By Wesley Gray, PhD|October 9th, 2014|

We've posted simulation and research-based studies on value and momentum. The evidence was pretty clear: never buy expensive [...]

The Quantitative Value Investing Philosophy

By Wesley Gray, PhD|October 7th, 2014|

Benjamin Graham, who first established the idea of purchasing stocks at a discount to their intrinsic value more than 80 years ago, is known today as the father of value investing. Since Graham’s time, academic research has shown that low price to fundamentals stocks have historically outperformed the market. In the investing world, Graham’s most famous student, Warren Buffett, has inspired legions of investors to adopt the value philosophy. Despite the widespread knowledge that value investing generates higher returns over the long-haul, value-based strategies continue to outperform the market. How is this possible? The answer relates to a fundamental truth: human beings behave irrationally. We are influenced by an evolutionary history that preserved traits fitted for keeping us alive in the jungle, not for optimizing our portfolio decision-making ability. While we will never eliminate our subconscious biases, we can minimize their effects by employing quantitative tools.

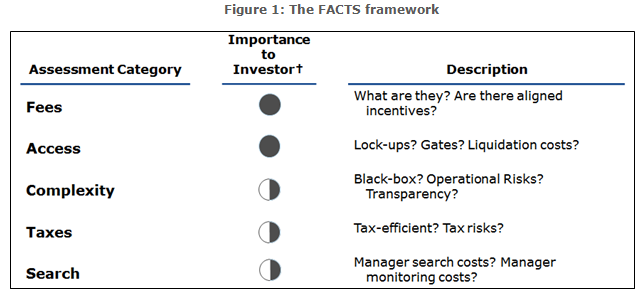

A Framework for Investment Manager Selection: Stick to the FACTS

By Wesley Gray, PhD|September 16th, 2014|

Used car salesmen types are everywhere, especially in the asset management business. What defines the used car salesman? Used car salesmen are often focused on selling something—anything on their lots that has four wheels—rather than identifying the right vehicle for the client. The same holds true with the asset management business. Some asset management salesmen just want to sell something—anything, regardless of its suitability. Alpha Architect’s experience working with family offices in the dual role of consultant and investment manager has given us the opportunity to see a lot of indecipherable marketing materials and esoteric investment strategies over the years, neither of which appear to be in the best interest of the investor. We’ve always sought a simple framework that would facilitate a quick evaluation of any strategy that came through the door, but nothing really existed. Necessity is indeed the mother of invention: We developed our own framework for determining strategy selection and assessment. Our method is based on a few simple concepts, which should be clearly understood within the context of any investing approach, regardless of objective. In the end, choosing investment opportunities simply comes down to the FACTS.

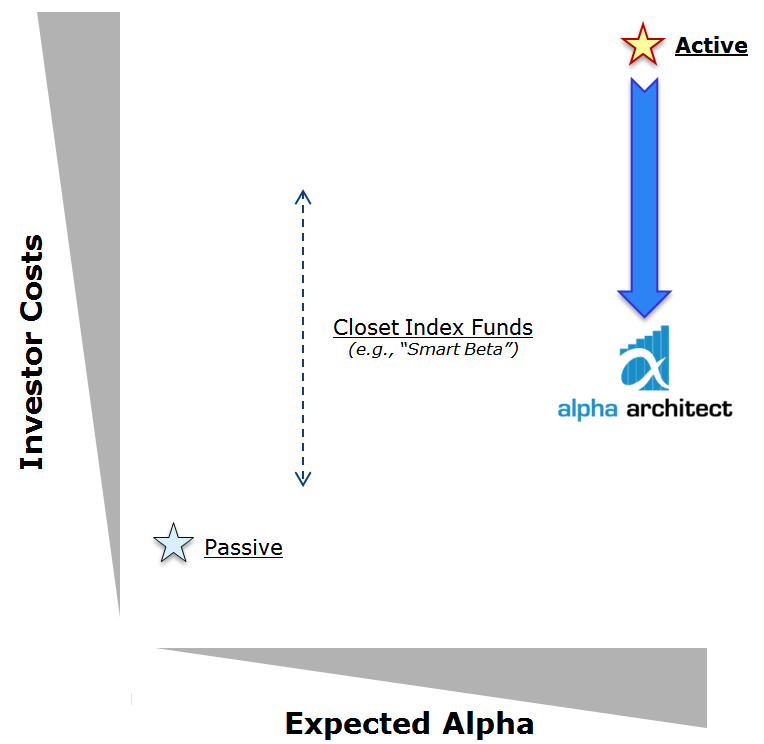

Our Value Proposition: Affordable Alpha

By Wesley Gray, PhD|September 16th, 2014|

Our mission is to empower investors through education. This mission is our passion and what drives us to go to work everyday. But this mission is not our product. Our product is Affordable Alpha: We seek to delivers alpha (highly differentiated risk/reward profiles) at low costs, thereby giving sophisticated (taxable) investors a higher chance of winning net of fees and taxes.

A Simulation Study on Simple Moving Average Rules

By Wesley Gray, PhD|July 28th, 2014|

The mention of technical analysis in the halls of academia can cause serious angst. The disdain for technical analysis [...]

Momentum Investing: Ride Winners and Cut Losers. Period.

By Wesley Gray, PhD|July 16th, 2014|

Momentum has historically been a great strategy. Although counter-intuitive to many value investors, buying stocks with rising prices has been a great investment approach--arguably better than value investing. Moreover, the approach is robust between the 2 samples analyzed. The lesson is clear: Let your winners ride and cut your losers short.

How to Build Expected Return Forecasting Models

By Wesley Gray, PhD|July 14th, 2014|

Investors are enamored with various investment houses and personalities who claim insight into the prospects for long-term expected market returns. Some classic examples include Nouriel Roubini, John Hussman, David Rosenberg, or Jeremy Grantham. All really smart people. But have you ever asked "How" these folks came to their conclusions? In most cases, the answer is probably "No" and the reason is because there is a lack of transparency from the author(s) and/or a lack of knowledge/understanding on behalf of the reader. We also want to highlight that one can develop incredibly complex return forecasting models -- super sexy, super interesting, super compelling, etc. -- but that still doesn't mean they are any good at forecasting much of anything.

Value Investing: Never Buy Expensive Stocks. Period.

By Wesley Gray, PhD|July 1st, 2014|

We did a recent internal simulation study on the performance of cheap and expensive stocks based on a [...]

Behavioral Finance and Investing: Are you Trying Too Hard?

By Wesley Gray, PhD|May 13th, 2014|

Everyone makes mistakes. It’s part of what makes us human. Because humans understand their actions are sometimes flawed, it was perhaps inevitable that the field of psychology would develop a rich body of academic literature to analyze why it is that human beings often make poor decisions. Although insights from academia can be highly theoretical, our everyday life experiences corroborate many of these findings at a basic level: “I know I shouldn’t eat the McDonalds BigMac, but it tastes so good.” Because we recognize our frequent irrational urges, we often seek the judgment of experts, to avoid becoming our own worst enemy. We assume that experts, with years of experience in their particular fields, are better equipped and incentivized to make unbiased decisions. But is this assumption valid? A surprisingly robust, but neglected branch of academic literature, has studied, for more than 60 years, the assumption that experts make unbias decisions. The evidence tells a decidedly one-sided story: systematic decision-making, through the use of simple quantitative models with limited inputs, outperforms discretionary decisions made by experts. This essay summarizes research related to the “models versus experts” debate and highlights its application in the context of investment decision-making. Based on the evidence, investors should de-emphasize their reliance on discretionary experts, and should instead approach investment decisions with systematic models. To quote Paul Meehl, an eminent scholar in the field, “There is no controversy in social science that shows such a large body of qualitatively diverse studies coming out so uniformly in the same direction as this one [models outperform experts].”

Why ETFs are more tax-efficient than mutual funds

By Wesley Gray, PhD|April 1st, 2014|

The ETF structure is often regarded as being "tax-efficient." However, many investors -- even sophisticated professionals -- often [...]