Stock Prices and Earnings: A History of Research

- Patricia M. Dechow, Richard G. Sloan, and Jenny Zha

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category!

Abstract:

Accounting earnings summarize periodic corporate financial performance and are a key determinant of stock prices. We review research on the usefulness of accounting earnings, including research on the link between accounting earnings and firm value and research on the usefulness of accounting earnings relative to other accounting and non-accounting information. We also review research on the features of accounting earnings that make it useful to investors, including the accrual accounting process, fair value accounting and the conservatism convention. We finish by summarizing research that identifies situations in which investors appear to misinterpret earnings and other accounting information leading to security mispricing.

Data Sources:

CRSP/COMPUSTAT

Alpha Highlight:

Understanding the relationship between earnings and stock prices can create interesting (but possibly fleeting?) returns.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Strategy Summary:

- Summary paper of research on earnings and stock prices. Here are some highlights from the paper:

- Do earnings convey any information?

- Beaver (1968) finds that trading volume and squared abnormal stock returns double around earnings announcement dates.

- Is the earnings number useful?

- Ball and Brown (1968) find the stock return spread between “good news” and “bad news” is about 30% for the 18 months around the earnings announcement.

- Does it make sense to break out the earnings number?

- Lipe (1986) classifies the income statement line into 6 components. While this decomposition improves forecasts, the improvements are not large and this decomposition is not generally used in future reserarch.

- Also finds that items classified as “other” on the income statement are less persistant than other components of earnings.

- Paper gives good definitions of accruals, conservatism, and fair values.

- Can investors take advantage of the earnings numbers?

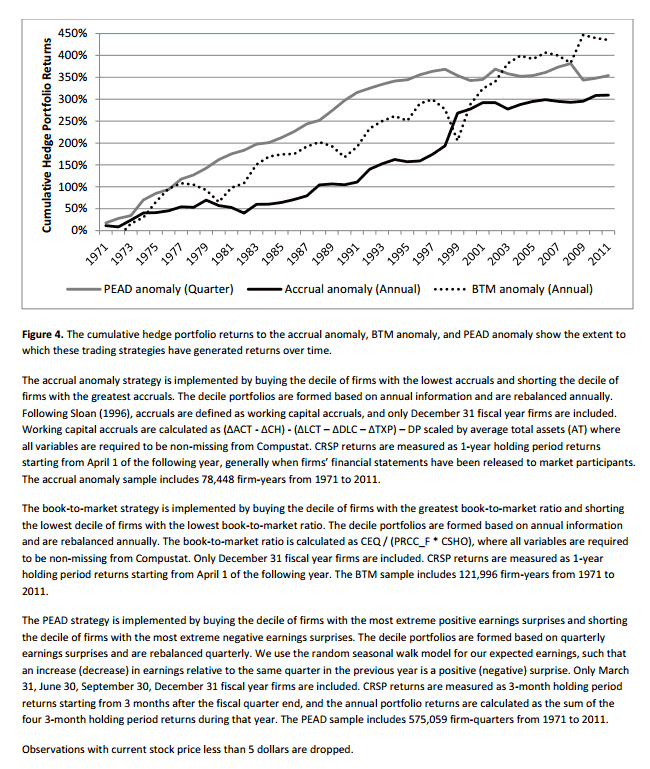

- Foster, Olsen, and Shevlin (1984) document that there is a post-earnings announcement drift (PEAD). Stocks in the highest decile of surprise earnings outperform the stocks in the lowest decile of surpirse earnings by 6% for the 60 trading days after the earnings announcement.

- This L/S strategy would have returned about 4% per year over the past 40 years.

- Sloan (1996) documents the accrual anomaly. Going long stocks in the lowest accrual decile and short stocks in the highest accrual decile would have returned about 3% per year over the past 40 years.

- This anomaly has recently tapered off.

- Foster, Olsen, and Shevlin (1984) document that there is a post-earnings announcement drift (PEAD). Stocks in the highest decile of surprise earnings outperform the stocks in the lowest decile of surpirse earnings by 6% for the 60 trading days after the earnings announcement.

- Do earnings convey any information?

Strategy Commentary:

- Good summary paper which replicates the findings of some of the earlier papers and finds the same results.

Follow the Earnings?

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.