Earnings Yields, Market Values, and Stock Returns

- Jaffe, Keim and Westerfield

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Core Idea:

At this time, there was significant dispute in academia as to whether the value premium was perhaps due to the size effect.

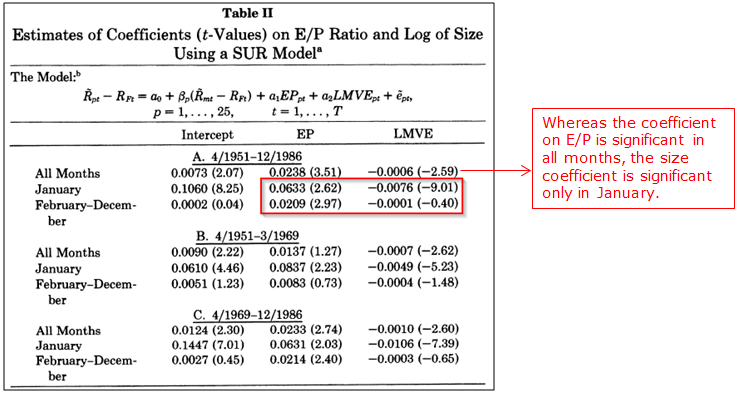

The paper attempts to disentangle the anomaly of earnings to price ratio (or “P/E”) from that of firm size; it examines the relation between the stock returns and E/P and size effects, using a longer sample (from 1951 to 1986) than previous research and investigating January and non-January months separately.

Alpha Highlight:

- The core finding is that size is primarily a seasonal effect, and thus that the E/P effect was not fundamentally driven by size.

- Note below how the coefficients on both E/P and size are significant in January, but only the E/P coefficient was significant outside of January.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.