The remarkable fact is that nobody can beat the market forever — not even Warren Buffett.

A quick glance at the most recent Berkshire Hathaway annual report (PDF) highlights an amazing data point: Warren Buffett has compounded at 19.7% a year from 1965 through 2013; the S&P 500 Total Return Index has compounded at 9.8% a year from 1965 through 2013. The immediate reaction to these figures is predictable: “Warren Buffett is an investing god, so we should buy Berkshire Hathaway and throw away the keys.” The gut reaction is that Buffett can continue to beat the market forever. Unfortunately, as this post highlights, this is an impossible feat.

A PDF version of this is available here.

These Strategies Are Everywhere

Active fund managers like Buffett are not the only ones showing they can outperform the market over the long term. Academic research is littered with investment strategies that purport to generate anomalous returns that almost double the market’s return each year. A few examples follow:

- “Value Investing: The Use of Historical Financial Statement Information to Separate Winners from Losers“: 23% annual return from 1976 to 1996.

- “The Asset Growth Effect in Stock Returns“: 26% annual return from 1968 to 2006.

- “Analyzing Valuation Measures: A Performance Horse Race over the Past 40 Years“: 17.66% annual returns from 1971 to 2010.

But Markets Are Efficient . . . Right?

I am continually haunted by a note I received from Eugene Fama, one of my dissertation advisers while I was finishing my PhD at the University of Chicago. Professor Fama went on to win the Nobel Prize in Economic Sciences for his work on market efficiency, so when Fama speaks, you listen. Fama wrote a response on an early draft of my paper on the performance of stock picks submitted to Value Investors Club. In the early manuscript I sent him, I stated proudly: “. . . this paper shows value investors outperform the market.”

Here was his response:

Your conclusion must be false. Passive value managers hold value-weight portfolios of value stocks. Thus, if some active value managers win, it has to be at the expense of other active value managers. Active value management has to be a zero-sum game (before costs).

To my chagrin, Fama’s comments were technically correct. I did not show that “value investors outperform the market” — far from it. I showed that a “select group of investors participating in Value Investors Club outperformed the market.” My evidence did not support the notion that value investors as a group outperform the market. I was broken from a fresh whipping by a market efficiency expert, but I learned a great lesson in arithmetic: Value-weight market returns have to be representative of the collective investor experience because the value-weight market return represents the return to all investors in the stock market. And for every active winner who outperforms the market, there necessarily must be a loser somewhere along the line. (Debatable if you go deep geek, but in the ballpark of reasonable as a first approximation).

How Long Can We Beat the Market?

If value-weight market returns reflect a binding constraint on the collective investor experience, how long can an individual investor “beat the market” before they actually becomes the market? As it turns out, compound growth prevents skilled investors from beating the market forever. This result is counterintuitive but follows the established behavioral bias that humans have a hard time understanding the implications of compound growth. Al Bartlett, professor emeritus in nuclear physics at the University of Colorado at Boulder, states this bias succinctly:

The greatest shortcoming of the human race is our inability to understand the exponential function.

To identify just how long a skilled investor can beat the market, I perform a study on the time series of value-weighted return (including all distributions) for the entire CRSP universe from 1926 through 2013 (representing all stocks traded on the NYSE, AMEX, and NASDAQ). If you are unfamiliar with CRSP, think of the database as the closest thing researchers have to the “total US market.” The Wilshire 5000 Index is the best “practitioner” analogy.

With a large amount of monthly return data extending back to 1926, I conduct the following experiment:

- Start a guaranteed “winner” portfolio on 1 January 1926 and invest at an above-market rate through 31 December 2013. This portfolio represents the experience of a highly skilled investor.

- Start a “loser” portfolio that represents the ownership of the rest of the market, approximately $28 billion. The loser portfolio returns the overall value-weighted market return minus the return it “lost” to the “winner” portfolio. This portfolio represents the experience of a passive investor who simply holds the market.

An example highlights how my experiment works. The winner portfolio starts off owning 0.00001% of the entire market as of January 1926 and grows consistently at a market-beating rate of return. This initial ownership percentage amounts to a very modest sum of $2,804 billion because that is the market cap of all securities as of January 1926; the loser portfolio starts off owning the remaining 99.99999%. Consider the January 1926 CRSP value-weight market return (with distributions included), which was 0.7405%. This 0.7405% gain grows the total market value of all securities from $2,804 billion to $2,824 billion. The “winner” portfolio — assuming a 30% compound annual growth rate — was 2.5% (30%/12). The winner portfolio grows from $2,804 billion to $2,866 billion. The “loser” portfolio, which represents the return remaining after the winner portfolio takes its outsized returns out of the market, decreases to $2,824 billion. In the end, the winner portfolio earns 2.50%, the loser portfolio earns 0.7404999%, and the entire market return earns 0.7405% (by construction, the value-weighted returns of the “winner” and the “loser” portfolios must equal the actual value-weighted market return).

With this in mind, I decided to investigate answers to the following questions:

- When does the “winner” portfolio own over half of the stock market?

- What percentage of the stock market does the “winner” portfolio own at the end of 2013?

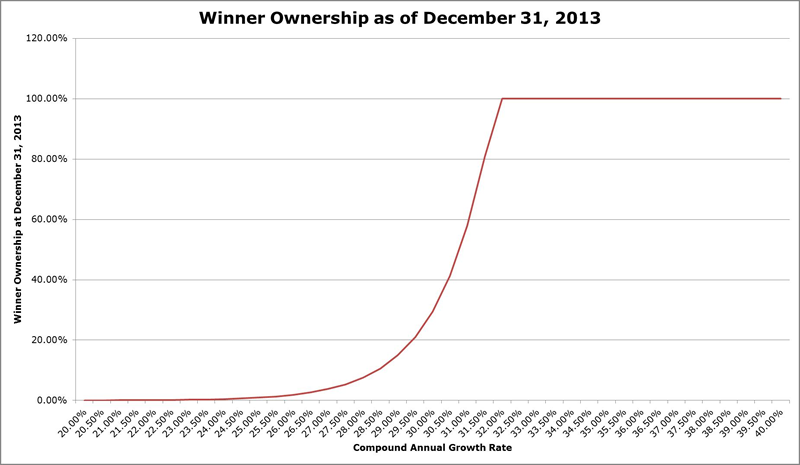

The following graph examines ownership percentage for various annual compounding rate assumptions and highlights why amazing compound annual growth rates must mean revert over time. With high levels of compounding, an investor quickly becomes the entire stock market. For example, at a 30% compound annual return, an investor owns 29.48% of the entire stock market at the end of 2013 — approximately $7.5 trillion of the $25.6 trillion in total market wealth as of 31 December 2013.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

At even higher rates of compounding, say 32% and higher, an investor would eventually own the entire stock market. This result is impossible on many levels. The harsh mathematical reality is that all great investors eventually manage a portfolio with massive scale. Earning a high return eventually forces a skilled investor to own a larger and larger percentage of the stock market (i.e. Warren Buffett).

We Can’t Beat the Market Forever

The point of this thought experiment is clear: No investor can continuously outperform the market over long periods of time. Eventually, this “genius” would own all wealth in the economy. And by definition, if you own the market, you can’t outperform the market. Accordingly, we are left with the following:

- Earning 25% — or more — compound annual returns over long horizons is virtually impossible.

- Investors earning 32% or higher returns end up owning the entire stock market.

- A “doable” 20% a year implies that an investor will own 0.026% of the market at the end of 2013. With a $25.6 trillion total market value as of 31 December 2013, this implies a personal stock portfolio worth $6.6 billion — not a bad retirement plan.

- Warren Buffett — and perhaps a select handful of others — has been able to achieve 20%+ returns over very long time periods. These individuals represent some of the richest people on the planet because of the phenomenon described in this experiment.

- Great investors might have an epic run of 20%+ returns for five, 10, maybe even 15 or 20 years, but as an investor’s capital base grows exponentially, the capital base slowly becomes the market, and the market cannot outperform itself.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.