Jason Hsu of Research Affiliates has some easily accessible research on the so-called investor return gap (we refer to this as the Behavioral Investor Gap and have covered the concept here).

- Here is the white paper on the subject

- And here is the accompanying webinar

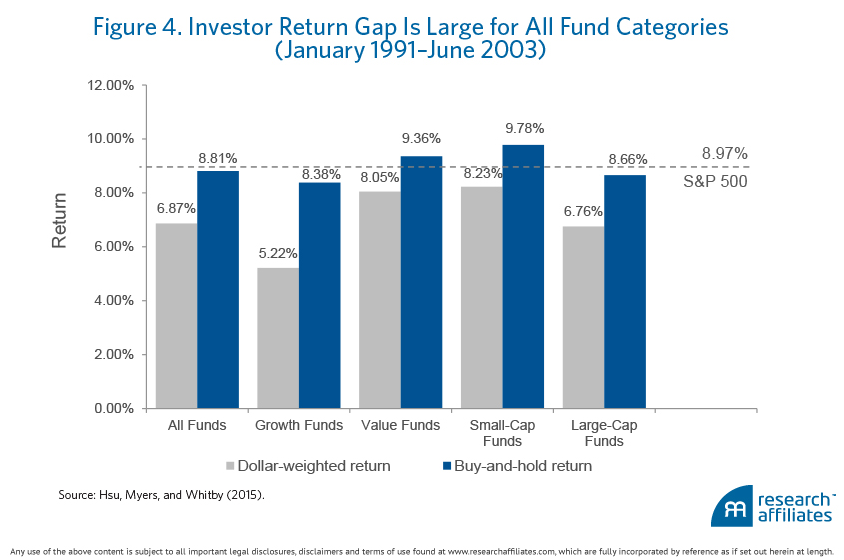

Hsu’s “investor return gap” is the difference in returns between buy-and-hold returns and dollar-weighted returns. In other words, the spread between what one would theoretically earn if one were a long-term investor and what one would actually earn from investing in the same strategy after accounting for the timing of fund flows in/out of the strategy.

Below is a graphic from their site highlighting the empirical evidence on the investor return gap:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The chart highlights that investors shoot themselves in the foot by trying to “time” various investment styles.

A few great quotes from Jason’s writeup

On delegated investment decisions:

The manager could be doing exactly the right thing by tilting the investor’s portfolio toward value stocks. But by redeeming the allocation to value managers, the investor is able to more than offset the manager’s insight and effort.

Insititutionalized behavioral biases:

What started as behavioral biases—that we confuse short-term performance as vital information on manager skill, and that we enjoy blaming others and holding them accountable for random bad outcomes—have been institutionalized.

High fee managers are not the biggest problem–by a long shot!

We are our own worst enemy, placing high-fee managers a distant second on the list of people contributing to our wealth destruction.

Why individuals have an edge over the so-called professional investors:

Investors who have the courage to be a contrarian will earn a handsome “fear” premium for taking the other side of the industry’s trades, counter to those who seek to avoid uncomfortable client conversations.

Conclusion

I enjoy Jason’s research and I think his latest insights on short-termism and its negative effects on investor outcomes is incredibly important and under appreciated. We highlight this in our own research and Jason’s ideas are in line with our discussions on sustainable active investing.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.