Similar to some better-known factors like size and value, time-series momentum is a factor that historically has demonstrated above average excess returns. Time-series momentum, also called trend-momentum or absolute momentum, is measured by a portfolio long assets that have had recent positive returns and short assets that have had recent negative returns. Compare this to the traditional (cross-sectional) momentum factor that considers recent asset performance only relative to other assets. The academic evidence suggests that inclusion of a strategy targeting time-series momentum in a portfolio improves the portfolio’s risk-adjusted returns. Strategies that attempt to capture the return premium offered by time-series momentum are often called “managed futures,” as they take long and short positions in assets via futures markets — ideally in a multitude of futures markets around the globe. This article dives into time-series momentum and examines some of its specific qualities that make a managed futures strategy a good portfolio diversifier.(1)

In general, an asset that has low correlation with broad stocks and bonds provides good diversification benefits. Low or near-zero correlation between two assets means that there is no relationship in their performance: Asset A performing above average does not tell us anything about Asset B’s expected performance relative to its average. The addition of a low-correlation asset to a portfolio will, depending on the specific return and volatility properties of the asset, improve the portfolios risk-adjusted returns either by improving the portfolio’s return, reducing the portfolio’s volatility, or both.

An Introduction to Time Series Momentum

My colleague, Sean Grover, and I review the literature on times-series momentum beginning with the May 2012 Journal of Financial Economics article “Time Series Momentum.” The authors, Tobias Moskowitz, Yao Hua Ooi and Lasse Pedersen, showed that times-series momentum exhibits low correlation with broad bond markets and near-zero correlation with broad stock markets over the sample period from January 1985 through February 2017. This means that the returns of a trend-following strategy are nearly independent of the returns of traditional stock and bond portfolios. But the time-series momentum factor also has diversification benefits beyond these simple correlations. The historical evidence demonstrates that time-series momentum also provides a good hedge against bear equity markets.

The figure below, taken from the original paper, highlights this point:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

The chart above showcases the unique nature of time-series momentum strategies (or “trend-following managed futures”). When the equity market is taking a dive, time-series momentum strategies generally move higher. These results cover the 1985 to December 2009 period.

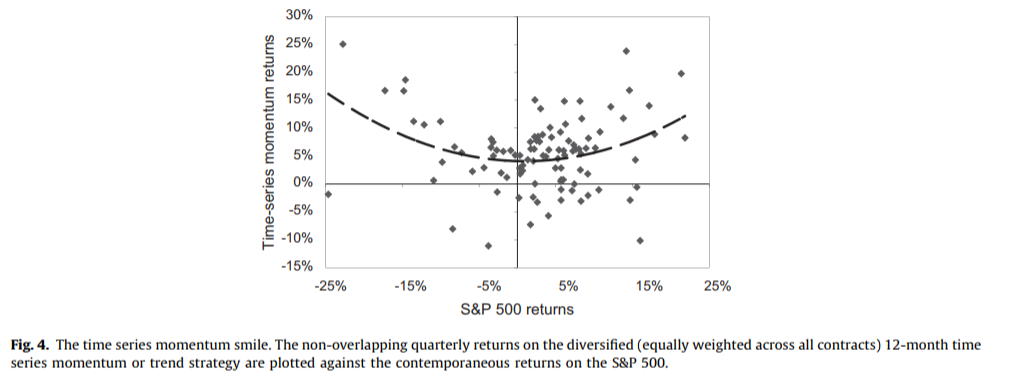

The next paper we’ll review is the 2014 study “A Century of Evidence on Trend-Following Investing.” (updated version here). The authors, Brian Hurst, Yao Hua Ooi and Lasse H. Pedersen, constructed an equal-weighted combination of one-month, three-month and 12-month time-series momentum strategies for 67 markets across four major asset classes (29 commodities, 11 equity indices, 15 bond markets and 12 currency pairs) from January 1880 to December 2013.

Their results include implementation costs based on estimates of trading costs in the four asset classes. They further assumed management fees of 2 percent of asset value and 20 percent of profits, the traditional fee for hedge funds. The key takeaway from the paper is similar to the prior paper discussed — time series momentum strategies provide a unique diversification opportunity. This core result can be visualized via the time-series momentum smile. However, this time around the authors identify the same unique pattern over a much longer time period, 1880 to 2013.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

In addition to the chart above, the following is a summary of the AQR researchers’ findings:

- The performance was remarkably consistent over an extensive time horizon that included the Great Depression, multiple recessions and expansions, multiple wars, stagflation, the global financial crisis of 2008, and periods of rising and falling interest rates.

- Annualized gross returns were 14.9 percent over the full period, with net returns (after fees) of 11.2 percent, higher than the return for equities but with about half the volatility (an annual standard deviation of 9.7 percent).

- Net returns were positive in every decade, with the lowest net return being the 5.7 percent return for the period beginning in 1910. There were also only five periods in which net returns were in the single digits.

- There was virtually no correlation to either stocks or bonds. Thus, the strategy provides strong diversification benefits while producing a high Sharpe ratio of 0.77. Even if future returns are not as strong, the diversification benefits would justify an allocation to the strategy.

The researchers at AQR observed that “a large body of research has shown that price trends exist in part due to long-standing behavioral biases exhibited by investors, such as anchoring and herding [and we would add to that list the disposition effect and confirmation bias], as well as the trading activity of non-profit-seeking participants, such as central banks and corporate hedging programs. For instance, when central banks intervene to reduce currency and interest-rate volatility, they slow down the rate at which information is incorporated into prices, thus creating trends.”

AQR’s researchers continued:

The fact that trend-following strategies have performed well historically indicates that these behavioral biases and non-profit-seeking market participants have likely existed for a long time.” Why is this the case? They explain: “The intuition is that most bear markets have historically occurred gradually over several months, rather than abruptly over a few days, which allows trend followers an opportunity to position themselves short after the initial market decline and profit from continued market declines.”

Importantly, from a portfolio perspective, looking only at years when equity markets are negative, time-series momentum’s correlation with stocks is around -0.5. The result is that it has tended to perform particularly well in extreme up or down years for the stock market, including the most recent global financial crisis of 2008. In fact, they found that during the 10 largest drawdowns experienced by the traditional 60/40 portfolio over the past 135 years, the time-series momentum strategy experienced positive returns in eight of these stress periods and delivered significant positive returns during a number of these events. This indicates that time-series momentum tends to perform well at the exact time when a portfolio needs it most.

AQR also noted that these results were achieved even with a “2-and-20” fee structure. Today, there are funds that can be accessed with much lower, although still not exactly cheap, expenses (including AQR’s own Managed Futures Strategy I Fund, AQMIX, which has an expense ratio of 1.21 percent, as well as the R6 version of the fund, AQMRX, which has a lower expense ratio of 1.13 percent). (Full disclosure: My firm, Buckingham Strategic Wealth, recommends AQR funds in constructing client portfolios.)

Additionally, in the study, “Trading Costs of Asset Pricing Anomalies,” by Andrea Frazzini, Ronen Israel and Tobias Moskowitz, AQR found that its actual trading costs have been only about one-sixth of the estimates used for much of the sample period (1880 through 1992) and approximately one-half of the estimates used for the more recent period (1993 through 2002). (a summary on the trading costs paper is here).

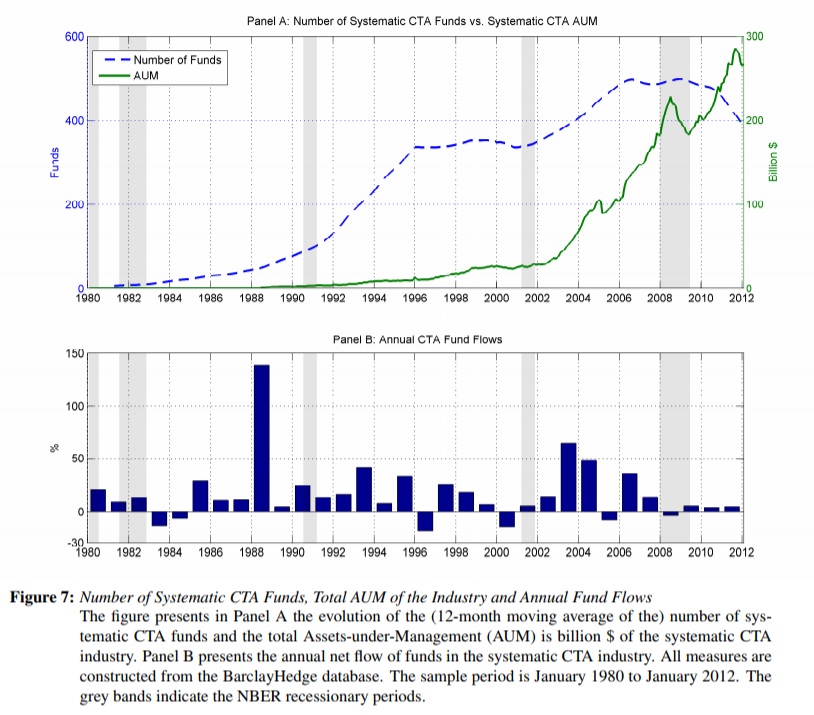

Further evidence on time-series momentum comes from Akindynos-Nikolaos Baltas and Robert Kosowski, authors of the 2013 study “Momentum Strategies in Futures Markets and Trend-Following Funds.” The authors studied “the relationship between time-series momentum strategies in futures markets and commodity trading advisors (CTAs), a subgroup of the hedge fund universe that was one of the few profitable hedge fund styles during the financial crisis of 2008, hence attracting much attention and inflows in its aftermath.” The authors noted that following inflows over the subsequent years, the size of the industry had grown substantially, and CTA funds exceeded $300 billion of the total $2 trillion assets under management invested in hedge funds by the end of 2011. Their study covered the period from December 1974 through January 2012 and included 71 futures contracts across several assets classes, specifically 26 commodities, 23 equity indices, 7 currencies, and 15 intermediate-term and long-term bonds.

Here is a chart highlighting the key findings regarding the industry’s growth:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

And here is a summary of their findings:

- Time-series momentum exhibits strong effects across monthly, weekly and daily frequencies.

- Strategies with different rebalancing frequencies have low cross-correlations and therefore capture distinct return patterns.

- Momentum patterns are pervasive and fairly robust over the entire evaluation period and within sub-periods.

- Different strategies achieve annualized Sharpe ratios of above 1.20 and perform well in up and down markets, which renders them good diversifiers in equity bear markets.

- Commodity futures-based momentum strategies have low correlation with other futures strategies. Thus, despite the fact that they have a relatively low return, they do provide additional diversification benefits.

Importantly, the authors found that momentum profitability is not limited to illiquid contracts. Rather, momentum strategies are typically implemented by means of exchange-traded futures contracts and forward contracts, which are considered relatively liquid and have relatively low transaction costs compared to cash equity or bond markets. In fact, they found that “for most of the assets, the demanded number of contracts for the construction of the strategy does not exceed the contemporaneous open interest reported by the Commodity Futures Trading Commission (CFTC) over the period 1986 to 2011.” They also found that the “notional amount invested in futures contracts in this hypothetical scenario is a small fraction of the global OTC derivatives markets (2.3% for commodities, 0.2% for currencies, 2.9% for equities and 0.9% for interest rates at end of 2011).” Thus, they concluded:

Our analyses based on the performance-flow regressions and the hypothetical open interest exceedance scenario do not find statistically or economically significant evidence of capacity constraints in time-series momentum strategies.

What Does the CTA World Tell Us About Time-Series Momentum?

However, following strong performance in 2008, the aggregate performance of trend-following CTA funds has been relatively weak. For example, from January 2009 to June 2013, the annualized return of the SG CTA Trend Sub-Index (formerly the Newedge Trend Index) was -0.8 percent, versus 8.0 percent over the prior five-year period. This occurred during a period of slow recovery in the United States and prolonged crisis in the Eurozone. Relatively poor performance, combined with large inflows following the strong performance, leads investors to question both whether the trend-following strategy has already become too crowded and if it will work in the future.

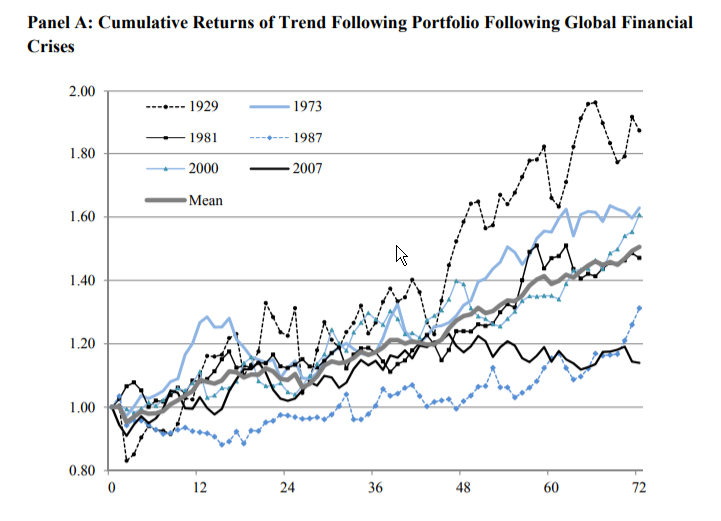

The final paper we’ll review is the 2014 study, “Is This Time Different? Trend Following and Financial Crises.” Using almost a century of data on trend-following, the authors, Mark C. Hutchinson and John O’Brien, investigated what happened to the performance of the strategy subsequent to the U.S. subprime and Eurozone crises, and whether it was typical of what happens after a financial crisis. They note: “Identifying a list of global and regional financial crises is problematic.” Thus, they chose to use the list of crises from two of the most highly cited studies on financial crises, “Manias, Panics, and Crashes: A History of Financial Crises” (originally published in 1978) and “This Time Is Different: Eight Centuries of Financial Folly” (originally published in 2009). The six global crises studied were: the Great Depression in 1929, the 1973 Oil Crisis, the Third World Debt crisis of 1981, the Crash of October 1987, the bursting of the dot-com bubble in 2000 and the Sub-Prime/Euro crisis beginning in 2007.

Here is a chart that highlights the performance of trend-following portfolios following crises:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Note the strong positive performance across all crises, which are often periods when broad equity markets are suffering from large losses.

The authors don’t limit their analysis to major global crises. The regional crises studied (with year of inception in parentheses) were: Spain (1977), Norway (1987), Nordic (1989), Japan (1990), Mexico (1994), Asia (1997), Colombia (1997) and Argentina (2000). The start date for each crisis was the month following the equity market high preceding the crisis. Because neither of the two aforementioned studies provided guidance on the length or end date of each crisis, rather than attempting to define when each individual crisis finished, the authors instead focused on two fixed time periods: 24 months and 48 months after the prior equity market high.

Hutchinson and O’Brien’s dataset for the global analysis consisted of 21 commodities, 13 government bonds, 21 equity indices and currency crosses derived from nine underlying exchange rates covering a sample period from January 1921 to June 2013. Their results include estimates of trading costs as well as the typical hedge fund fee of 2 percent of assets and 20 percent of profits.

The following is a summary of their findings:

- Time-series momentum has been highly successful over the long term. The average net return for the global portfolio from 1925 to 2013 was 12.1 percent, with volatility of 11 percent. The Sharpe ratio was an impressive 1.1 (a finding consistent with that of other research).

- There is a breakdown in futures market return predictability during crisis periods.

- In no-crisis periods, market returns exhibit strong serial correlation at lags of up to 12 months.

- Subsequent to a global financial crisis, trend-following performance tends to be weak for four years on average. This lack of time-series return predictability reduces the opportunity for trend-following to generate returns.

- Comparing the performance of crisis and no-crisis periods, the average return in the first 24 months following the start of a crisis (4.0 percent) is less than one-third of the return earned in no-crisis periods (13.6 percent). Performance in the 48 months after a crisis starts (6.0 percent) was well under half the return in that of no-crisis periods (14.9 percent).

- Across stocks, bonds and currencies, the results were consistent. The exception was commodities, where returns were of similar magnitude in pre- and post-crisis periods.

- They found a similar effect when examining portfolios formed of local assets during regional financial crises.

The authors noted that behavioral models link momentum to investor overconfidence and decreasing risk aversion, with both leading to return predictability in asset prices. Under these models, overconfidence should fall and risk aversion should increase following market declines, so it seems logical that return predictability would fall following a financial crisis. It is also important to note, as the authors did, that “governments have an increased tendency to intervene in financial markets during crises, resulting in discontinuities in price patterns.” Such interventions can lead to sharp reversals, with negative consequences for trend-following.

Hutchinson and O’Brien concluded:

The performance of these types of strategies [trend-following] is much weaker in crisis periods, where performance can be as little as one-third of that in normal market conditions. This result is supported by our evidence for regional crises, though the effect seems to be more short lived. In our analysis of the underlying markets, our empirical evidence indicates a breakdown in the time series predictability, pervasive in normal market conditions, on which trend following relies.

Summary

As an investment style, trend-following has existed for a long time. The data from the aforementioned studies provide strong out-of-sample evidence beyond the substantial evidence that already existed in the literature. It also provides consistent, long-term evidence that trends have been pervasive features of global stock, bond, commodity and currency markets.(2)

Addressing the issue of whether we should expect trends to continue, AQR researchers concluded in their aforementioned paper:

The most likely candidates to explain why markets have tended to trend more often than not include investors’ behavioral biases, market frictions, hedging demands, and market interventions by central banks and governments. Such market interventions and hedging programs are still prevalent, and investors are likely to continue to suffer from the same behavioral biases that have influenced price behavior over the past century, setting the stage for trend-following investing going forward.

The bottom line is that, given the diversification benefits and the downside (tail-risk) hedging properties, a moderate portfolio allocation to trend-following strategies merits consideration. Note, however, that the generally high turnover of trend-following strategies renders them relatively tax inefficient. Thus, there should be a strong preference to hold them in tax-advantaged accounts.

References[+]

| ↑1 | Here is an introductory piece on managed futures if you are unfamiliar with the strategy. |

|---|---|

| ↑2 | A new paper in the Journal of Financial Markets suggests that the results are driven by volatility scaling, however, Alpha Architect has a nice rebuttal to this argument. |

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.