Stick to the Fundamentals and Discover Your Peers

- Jean Overgaard Knudsen, Simon Kold and Thomas Plenborg

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

When performing multiple-based valuations, which rely on the assumption that perfect substitutes should sell for the same price, it is very important to identify companies that are truly comparable. Most analysts use industry classifications.

Lee et al. (2015) note that industry classifications are at best crude guidelines for identifying comparable companies.

Knudsen et al. study an alternate approach, “sum of absolute rank differences (SARD).” This method selects comparable companies on the basis of the least sum rank difference across a range of variables (i.e return on equity, market capitalization, P/E, P/B etc.) that are expected to affect multiples and ask the following:

- Does SARD generate more accurate valuation estimates than the traditional industry classification approach?

- Does SARD generate more accurate valuation estimates if used in conjunction with the industry classification approach?

What are the Academic Insights?

By studying companies in the S&P1500 from 1995 to 2014 and applying the SARD method on combinations of up to five fundamental variables (ROE, Net Debt/EBIT, Size, Implied Growth, EBIT margin) and four multiples (EV/EBIT, EV/Sales, P/B and P/E), the authors find the following:

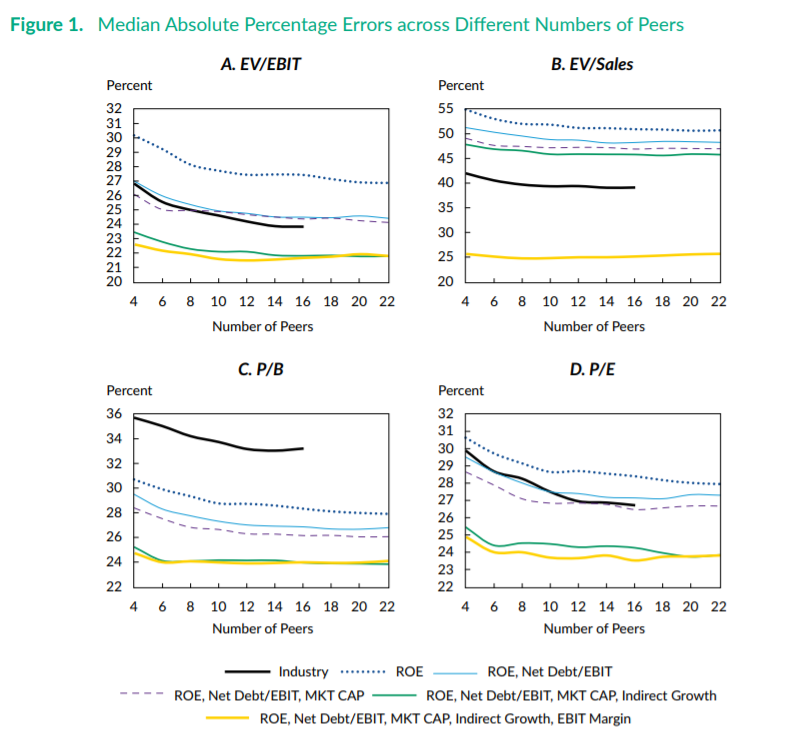

- YES- A comparison of the accuracy of both the industry and the SARD approach shows that the latter yields consistently more accurate valuation estimates. A comparison of the differences in the median ( as well as the mean and interquartile range) absolute valuation error across the four multiples shows that EV/Sales yields the largest difference (0.407 versus 0.254).

- YES- the SARD approach produces an incremental increase in accuracy when used within industries compared to when utilized across industries.

The authors perform robustness checks.

Why does it matter?

The multiples approach relies on the theory that perfect substitutes should sell at the same price. This theory implies that the selection of comparable companies is a crucial step. Most analysts and investors use industry classification as a proxy for company comparability but this relies on the assumption that companies in the same industry share the same economic characteristics.

The SARD approach is not restricted by the number of variables that can be used to identify peers or number of observations available that can be used to identify peers or number of observations available and is independent of industry classifications. Therefore, the approach may be particularly useful outside the United States, where the number of public companies and the number of observations are often less plentiful.

The Most Important Chart from the Paper:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

The use of industry as a criterion for selecting peers for multiples based valuation rests on the notion that companies operating in the same industry are more likely to share fundamental value drivers (i.e., profitability, growth, and risk). However, such companies may not have similar characteristics in terms of these drivers and thus should not be traded at the same multiple. We analyze this issue by developing the sum of absolute rank differences (SARD) approach. The SARD approach can account for an infinite number of proxies for profitability, growth, and risk while remaining independent of industry classifications. Our results indicate that the SARD approach yields significantly more accurate valuation estimates than the industry classification approach.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.