The tax benefits of the new Opportunity Zone program are potentially phenomenal. However, when you dig into the details of the program you quickly realize that many of the investment options are typically higher-risk and pretty limited (new hotels and greenfield real estate developments).

Many Opportunity Zone (“OZ”) investors are faced with a problem: they’d love to take advantage of the tax benefits, but they don’t want to jeopardize their hard-earned wealth via high-risk OZ fund investments. OZ investments will always involve a level of risk, but in an ideal world there would be less risky options available.

Why are there a lack of lower risk OZ investments? Long story short, the OZ program doesn’t allow for debt or bond investments – only equity investments. Also, many Opportunity Funds being pitched are targeting a 15%+ rate of return – something that is probably unrealistic without taking on excessive leverage and risk.

But all is not lost. In this article, I outline potential ways to structure lower-risk OZ investments, while also generating pass-through tax depreciation for investors (something bonds can’t do). Finally, I include an example that illustrates these methods.(1)

Turning Equity into Debt

The OZ program only allows for equity — and not debt — investments. However, by working within the program’s rules, we can get really close to generating bond-like risk/return profiles with an equity investment.

The first thing we need to do is improve the credit worthiness of the investment project’s counter party. For many real estate development projects, the counter party is usually the general retail public or simply the real estate market (i.e. there really isn’t a counter party).

For example, there are no guarantees that after a developer builds a new hotel, it will have a given occupancy rate or generate the projected revenues, or that an investor will buy the asset back later at an attractive price. The local economy and the overall real estate market will determine these returns — no one can guarantee them. Although much analysis goes into these projections, at the end of the day, there is still some ‘crystal ball’ financial forecasting involved. And that’s OK, but this introduces risk that some investors would prefer to avoid.

What if we have a credit-worthy business or municipality as our counter party or project “Sponsor”? What if the Sponsor agrees to pay the investor a near-guaranteed rate of return for the use of their money under the OZ program? What if the Sponsor agrees to buy back the investor’s interest in the Opportunity Fund at a predetermined price in the future — thereby providing a near guaranteed exit? This scenario can greatly reduce the risk of an OZ investment and create bond-like returns.

Here are the 4 Steps to potentially turn OZ Equity Investments into more Bond-Like Investments (but with depreciation):

- Step 1: A credit-worthy Sponsor (i.e. a business or municipality) needs financing for a new construction project, such as a manufacturing plant, wastewater treatment plant upgrade, municipal firehouse or police station. In this scenario, an OZ investor, through an OZ Fund, would purchase the asset from the Sponsor and finance the new construction or renovations.

- Step 2: The Sponsor leases the facility back from the OZ Fund for a term of 10 years (or more).

- Step 3(a): The OZ Investor can choose to receive bond-like coupons (lease payments) from the Sponsor over the 10 years or they can choose to forego lease payments and take a larger buyout at the end of the investment period. This second option is similar to a zero-coupon bond and maximizes the capital gain tax benefits under the OZ program.

- Step 3(b): The OZ investor also receives depreciation tax benefits from their investment (something bonds can’t offer). This depreciation can be used to offset other tax liability, including any tax liability resulting from OZ lease payments.

- Step 4: The Sponsor purchases the facility back from the investor at a pre-arranged price at the end of the investment period (e.g. 10 years). This locks in the capital gains and rate of return on the investment.

Potential Benefits to the Investor

- Reduces investment risk

- Generates bond-like payments over the investment period (or)

- Can be structured to mirror a zero-coupon bond to maximize the capital gain tax benefits

- Locks in gains and rates of return before the investment is made

- Provides depreciation to the investor each year

Benefits to the Sponsor (e.g., Municipality or Credit Worthy Company/Developer)

- Lower cost of capital

- Off balance-sheet financing (they enter into a lease agreement and do not take on debt)

- Immediate cash at closing (due to initial sale of assets to the Opportunity Fund)

The framework outlined above seems to work. Using the steps outlined, I’ve identified a number of potentially lower-risk OZ projects.

Here are some recent examples:

- Municipal parking garages

- Solar developments with offtake power agreements

- Wastewater treatment plants

- Hospital expansions

- Municipal sewer upgrades

- Power plants (combined heat and power generation)

- and many others in development

A More Detailed Example: A Zero-Coupon Bond Example

Note: Although we are mimicking a zero-coupon bond with this example, deals can be structured to include lease payments that would resemble a bond’s coupon.

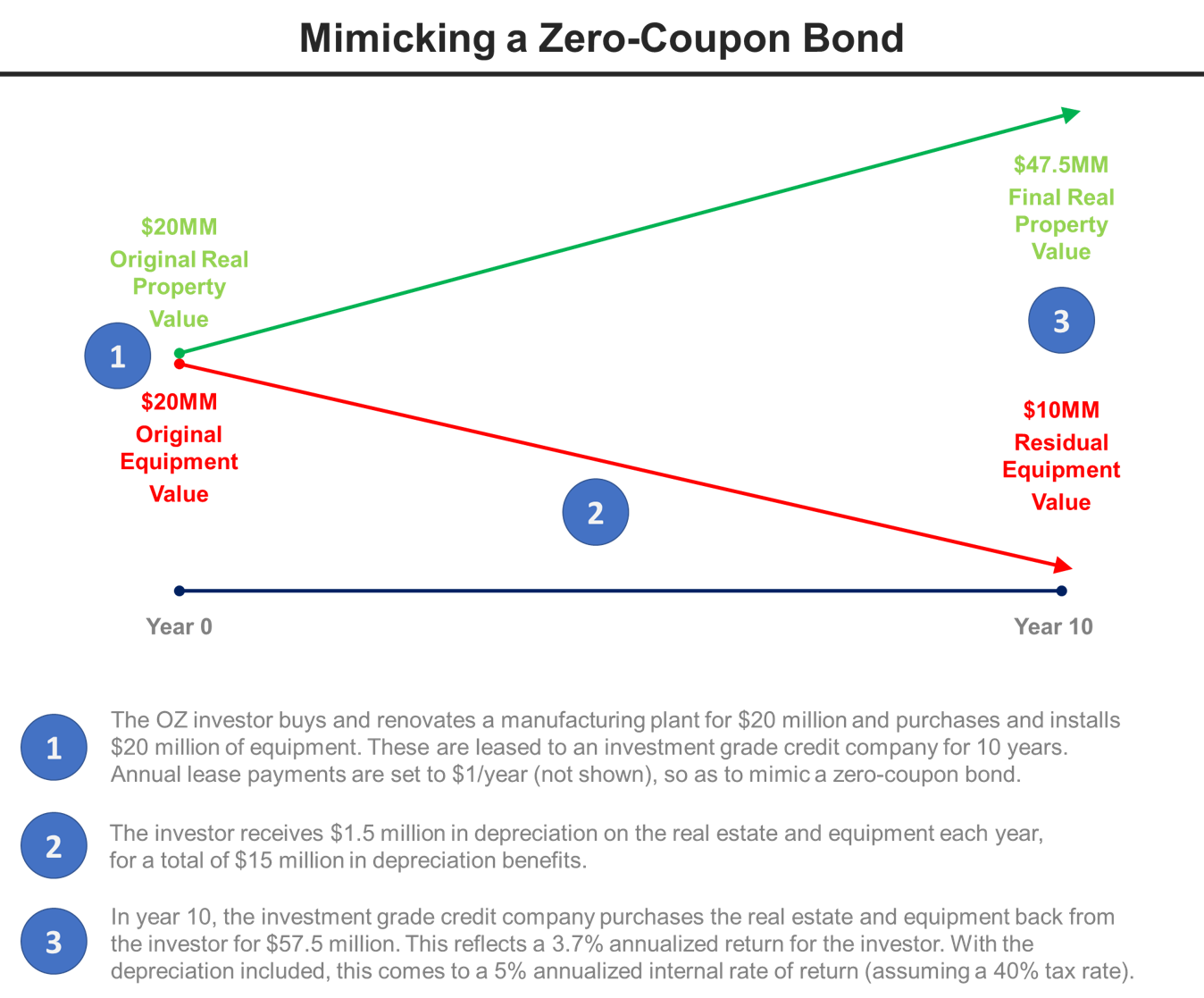

Here’s the Fact Pattern: An investment grade credit business will build a new manufacturing plant in an Opportunity Zone for $40 million. The business has a cost of capital of 4.5% and is willing to accept Opportunity Zone financing at 3.7%.

An Opportunity Zone investor wishes to invest $40 million into the project and wants to receive a zero-coupon bond return profile. The investor forgoes annual lease payments in return for a higher buy-back price at the end of the investment period. This potentially maximizes the final sale price and capital gain tax benefits under the OZ program.

The business agrees to buy the real estate and equipment back from the investor in 10 years for $57.5 million, thus generating a 3.7% capital gain rate of return for the investor — excluding depreciation benefits. The final breakdown of the sale price as as follows:

- The real estate is initially valued at $20 million, and the company is willing to buy it back for $47.5 million (or at a 9% annual appreciation rate, assuming this is defensible in the market).

- The equipment has a useful life of 20 years and would have a residual value of $10 million in year 10. The company will buy the equipment back at this price.

Here is a chart showing the steps and results:

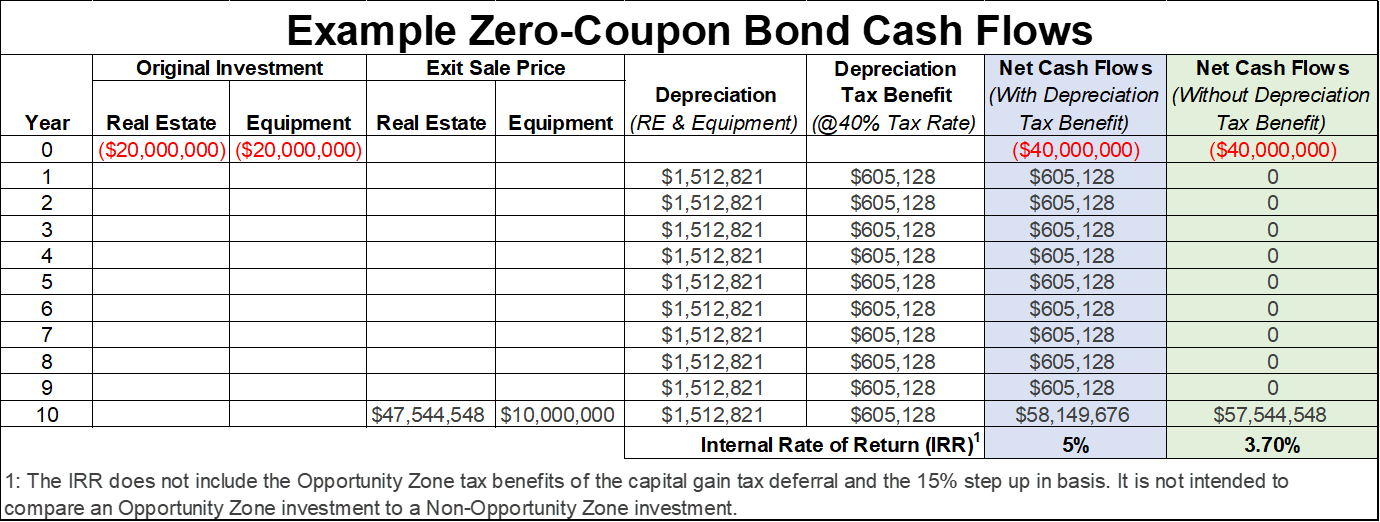

The cash flows and internal rates of return resulting from the example above:

What Returns Can I Expect?

To make this work, an OZ investor needs to offer a cost of capital that is lower than what the project Sponsor can get from a bank or from the municipal bond market. Otherwise, why would the Sponsor take the investor’s money?

At this time (early 2019), municipalities can borrow money in the 3% to 4% range and high-quality corporate debt is in the 4% to 6% range. Realistically, an OZ investor would have to accept returns that are one to two points below these ranges. Of course, if higher returns are desired, an investor could invest in slightly riskier projects or accept a longer investment horizon (i.e. go further out on the yield curve).

Furthermore, investors can benefit from pass-through depreciation as shown in the zero-coupon bond example above. This depreciation can increase returns by up to 1% or more.

What About the Fees?

No discussion about investing is complete without including a few words about fees.(2) There are a range of fees being offered by Opportunity Funds today. These typically mirror private equity fees and include closing fees, annual management fees and carried interest. These fees can become rather burdensome, especially if the investor is expecting a 3% per year tax benefit (see the returns chart in our Opportunity Zone Investor’s Guide). However, I think it’s possible for OZ fund fees to be similar to municipal bond ETF and mutual fund fees. That is, they could be less than 1% — which would have to be the case for these lower-risk, lower-return projects.

Is Affordable Lower-Risk OZ Investing Possible?

Not all investors have the same risk tolerance and diversifying Opportunity Zone investments across both high- and low-risk projects may be a good option. In fact, you’d be hard-pressed to find any wealth manager who would recommend that their clients invest all of their Opportunity Zone investments into high-risk projects. At the moment, most Opportunity Zone Funds seem to be targeting higher returns, but as the program matures, I expect we’ll see more lower-risk options become available.

If you’d like more information on the lower-risk projects mentioned above (e.g. power plants, parking garages, infrastructure projects etc.) or have questions about the investment process outlined here, please feel free to contact me (ask for Adam).

References[+]

| ↑1 | Note: In this article, we assume readers have a basic knowledge of the Opportunity Zone program. To learn more, you can reference our Opportunity Zone Investor’s Guide. Or, if you prefer a downloadable PDF version, you can get it here: Opportunity Zone Investor’s Guide.pdf. |

|---|---|

| ↑2 | See here for the FACTS framework for investment decision-making. |

About the Author: Adam Tkaczuk

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.