Is (systematic) Value Investing Dead?

- Ronen Israel, Kristoffer Laursen and Scott Richardson

- Working Paper, published at aqr.com

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Although there is widespread agreement that systematic value strategies have turned in at least a decade of underperformance, there is little agreement as to the underlying cause or cause(s). However, a number of rationalizations and critiques have emerged that question the long term viability of value strategies. The authors address in detail the relevant research or empirically test each of the criticisms in turn. They find very little supporting evidence.

The authors present a cogent discussion of four rationales for the demise of systematic value investing. The discussion is detailed and comprehensive. The authors utilize their own empirics in combination with evidence published elsewhere to make their case. It is quite an interesting read. The article proceeds logically through a dismissal, for the most part, of each of the common criticisms of systematic value investing, ending with a final discussion of the ultimate question:

- Share repurchases. The dramatic increase in share repurchases has decoupled book equity for valuation purposes. B/P has not been a useful systematic metric for quite awhile and repurchase activity has ramped up in recent periods.

- Conservative accounting rules. In combination with the increasing importance of intangibles as firms change their basic business models with accounting systems that fail to incorporate the associated value on financial statements, the role of accounting metrics has diminished.

- Monetary policy and intervention by central banks, low interest rates.

- Widespread use of simple value metrics has resulted in crowding, and elimination of the value premium

What are the Academic Insights?

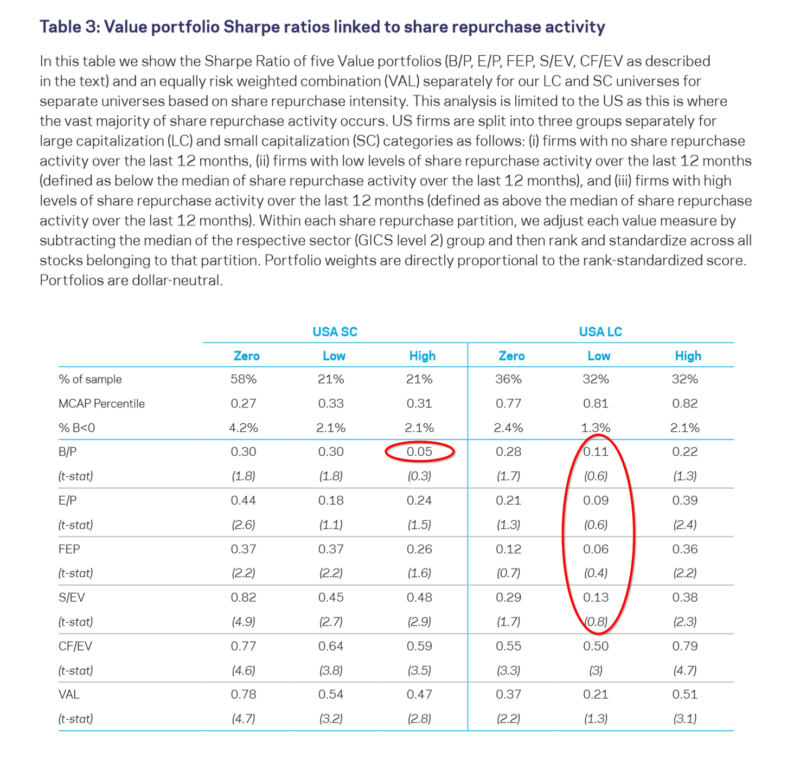

- The degree to which share repurchase activity has reduced the impact of five value measures, based on recent repurchase activity can be found in Table 3 below. Sharpe ratios across high, low, and zero repurchase activity are presented for the large-cap (LC) and small-cap (SC) universes. If a value strategy is compromised by recent share repurchase activity, then high groups should not work as well as for low groups. There is mixed evidence that this is the case. B/P returns are lower for the high group (.05) relative to zero or low groups for the SC universe only. In the LC universe, the results run counter to expectations. The authors also note: “ In unreported tests, we can reject the null hypothesis of equal average returns across pairs (e.g., High vs. Zero, Low vs. Zero and Zero vs. Low) for only two combinations out of the possible 36 combinations (6 measures, 2 size universes, 3 repurchase partitions), and that difference was for S/EV in SC.” The authors note for the period 2014 – 2019, 60% of small-cap stocks and 80% of large-cap stocks have engaged in repurchase activity, a distinct difference from previous periods. Additionally, for the period 2014 – 2019, 60% of small-cap stocks and 80% of large-cap stocks have engaged in repurchase activity. This large increase may mask the impact of negative book value on performance. For both universes, the percentage of negative book value increased to approximately 4% in the recent period, and to 6% for the high share repurchase large-cap groups. In another chart (not presented in this summary) the authors report rolling 2-year Sharpe ratios for B/P groups for high, low, and no repurchase activity. There was no evidence that the high activity firms performed any worse than low activity firms using the B/P metric, in spite of the recent increased intensity of repurchase activity itself.

- In combination with the increasing importance of intangibles, as firms change their basic business models with accounting systems that fail to incorporate the associated value on financial statements, the role of accounting metrics has diminished. Using an improved metric, adjusted operating cash flow (from the Credit Suisse HOLT database), designed to improve the usefulness of accounting information the authors compare it to CF/EV. The adjustment to operating cashflow essentially reverses the limitations imposed by current accounting rules. The metric (CFHOLT) is calculated as net income adjusted for special items, depreciation, amortization, interest expense, rental expense, minority interest, plus other proprietary economic adjustments, then standardized by enterprise value. A comparison of the CF/EV and the HOLT version showed that they performed similarly. Again, rolling 2 year Sharpe ratios for a recent 5 year period, large and small-cap universes showed a similar decline in performance for all value metrics. An attempt to accommodate for conservative accounting rules showed little difference. Apparently changes in business models, intangibles, and so on, although important, do not explain the most striking underperformance of value strategies we have experienced.

- An environment of low-interest rates and vigorous intervention into the equity markets by the Federal Reserve would seem to imply higher than justified prices for value stocks. That assumes value stocks behave as short-duration assets although the research (Asness, Maloney, and Moskowitz (2020) fails to confirm this particular hypothesis. There is empirical support for the proposition that positive performance by value strategies is weakly correlated (R-squares less than 10%) with the slope of the yield curve in both the US and globally.

- This criticism is normally applied when systematic strategies like value, have not performed well. Although it is difficult to conclude that because a systematic factor is well known that it should not be expected to be a source of expected returns. Value behaves as a risk premium, but that does not preclude it from being a source of return due to errors in expectations on the part of investors. In any case, arguing that increased attention and cash flows into the value factor have all but eliminated the associated return premium ignores considerable evidence. Empirical studies that document that across countries, asset classes, time periods, out-of-sample, and theoretically grounded require fact-based evidence to conclude that value is dead.

Why does it matter?

So, what gives? What explains the underperformance of value strategies? It seems that most, if not all of the obstacles and criticisms have been examined and discarded. Value strategies do well when the wedge between fundamentals and prices converge. We believe that wedge emerged from the tendency of investors to over extrapolate the historical performance of a firm, making value stocks just a little bit (or a lot) too cheap and growth (glamour) stocks just a little bit too expensive. As long as that tendency remains a feature of investor behavior, we will just have to wait for it to emerge again. We have seen similarly long periods of time where value has underperformed. The original behavioral hypothesis never depended upon the state of accounting rules, economic or technological (intangibles) changes, nor monetary policy at any point in time, did it? I will say however, it does seem to make sense to use a diversified set of metrics to signal “value” in any case or any market, rather than a single perhaps less optimal metric like B/P.

The most important chart from the paper.

Abstract

Value investing involves buying securities that appear cheap relative to some fundamental anchor. For equity investors that anchor is typically a measure of intrinsic value linked to financial statements. Recently, much has been written about the death of value investing. While undoubtedly many approaches to value investing have suffered recently, we find the suggestion that value investing is dead to be premature. Both from a theoretical and empirical perspective, expectations of fundamental information have been and continue to be an important driver of security returns. We also address critiques levelled at value investing and find them generally lacking in substance.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.