“Litigation funding allows lawsuits to be decided on their merits, and not based on which party has deeper pockets or stronger appetite for protracted litigation(1).”

Eileen Bransten, New York Supreme Court Justice

The 42-year period from 1980 through 2021 saw bull markets for both stocks and bonds, which provided investors with strong returns. However, those strong returns left equity valuations at historically high levels and bond yields at historically low levels—meaning expected returns are now lower than their historical averages. The result is that the current environment has created challenges for the traditional portfolio, such as a “balanced” 60 percent equities/40 percent bonds portfolio.

That has led many investors—both institutional and retail—to search for a variety of “alternative investments” each with their own specific risks and returns, dramatically increasing their allocations to alternative investments with much less exposure to the economic cycle risk of stocks and bonds and the inflation risk inherent to bonds. The term alternative investment covers a broad range of investment strategies that fall outside the realm of traditional asset classes. One such alternative that has attracted significant interest in recent years is the rapidly growing asset class of litigation finance (debt and equity investments in litigation claims and law firms).

Litigation Finance

Litigation finance, which has existed for more than 20 years in the United States, refers to transactions in which a third party provides capital (debt, equity, or a hybrid) to one of the parties to a legal claim (a plaintiff or law firm) in exchange for a financial interest derived in part from the outcome of the claim. Repayment of the financing is generally contingent upon the successful outcome of the underlying claim, whether by way of a judgment or, more frequently, an out-of-court settlement between the parties. The market for litigation finance is made up of three segments: commercial litigation finance, mass tort litigation finance, and personal litigation finance.

Litigation finance is one of the classes that has shared in the influx of capital targeting alternative investments due to the high returns that have been achieved and the fact that those returns have been (and should expect to be) uncorrelated to the economic cycle risks of both stocks and bonds, providing strong diversification benefits that reduce tail risks. It is a highly specialized niche due to: the lacking of liquidity; the lack of transparent pricing (there is a limited publication of pricing by a handful of private research firms, no centralized exchange, and terms can vary significantly from provider to provider, including duration, pricing, and deal structure); the lack of standardized structure; and the fact that each investment opportunity is tied to unique litigation (lots of idiosyncratic risks).

Thomas Healey, Michael McDonald, and Thea Haley, authors of the paper, “Litigation Finance Investing: Alternative Investment Returns in the Presence of Information Asymmetry,” published in the Spring 2022 issue of The Journal of Alternative Investments, provide an overview of litigation finance (what it is, how it works, and the key players); describe the process of sourcing and structuring litigation finance investments, and review the risk and return data provided by an alternative investments consulting firm and valuation agent for the period 2015 to 2019.

They began by noting:

“The litigation finance industry began in the late 1990s and picked up considerable momentum following the 2008 financial crisis… As of 2020, there were 46 dedicated fund managers in the litigation finance area, up from 41 in 2019. Most are comparatively small; the total dedicated industry AUM was $11.3B at the end of 2020, up 18% vs. 2019. These figures are only for dedicated litigation funders and exclude broader asset managers that are entering the space. Dedicated litigation funders executed $2.47B in 312 new commercial litigation funding deals in 2020.”

Potential Benefits of Litigation Finance

Litigation finance companies provide a number of important benefits to plaintiffs, attorneys, law firms, and investors.

- Plaintiffs

- Helps undercapitalized plaintiffs continue to pursue meritorious cases by financing commercial litigation expenses

- Provides capital injections for already-filed cases that experience funding constraints

- Unlocks liquidity for working capital

- Provides a cushion for personal expenses

- Allows companies to manage how litigation costs affect their balance sheets

- Enables greater access to top legal resources

- Attorneys and Law Firms

- Allows attorneys and law firms to accept cases from plaintiffs who otherwise could not afford their fees

- Provides capital for key litigation expenses, including expert witness fees

- Reduces the risk that clients will run out of money during litigation

- Enables attorneys and law firms to offer more flexible payment arrangements to prospective clients

- Increases plaintiffs’ effectiveness by providing funding for working capital and personal expenses

- Helps achieve recoveries that more accurately reflect case merits and damages

- Investors

- Investments in legal claims are generally uncorrelated to capital markets

- Outsized historical returns compared with other alternative asset classes

- Moderate time to liquidity compared to other alternative investments

Structuring Litigation Finance Investments

Healey, McDonald, and Haley noted:

While still in its early stages, the market for litigation finance is diverse and varied in the characteristics of its underlying investments. Some areas where investment options may differ include:

▪ Type of litigation. The diverse categories of underlying cases include intellectual property (IP), antitrust, breach of contract, tax disputes, commercial class action, fraud, employment, and domestic and international arbitration. Some firms tend to focus on key areas of expertise of their in-house legal professionals, such as IP and patents.▪ Size of claims. Litigation funders also tend to have different “sweet spots” for the size of cases they choose to fund. There is generally a direct correlation between target claim size and the minimum investment amounts for these vehicles.

Healey, McDonald, and Haley

▪ Stage of process. Investments can be made at various stages of a case, from pre-filing and discovery to trial, and even to the appeal phase.

▪ Single case versus portfolio. Some funds consist of a collection of investments in individual cases. Others invest in “portfolio deals,” where capital is provided to a law firm for a collection of contingency cases in return for some portion of the settlement or judgment won.

▪ Geographic scope. Funds may invest solely in U.S. litigation, or they may take a more global approach, typically investing in cases from other common law countries such as Canada, the United Kingdom, and Australia.

Origination

“Case origination leverages numerous channels, including inbound inquiry, attorney referrals, and outbound marketing efforts such as press releases and paid advertising in legal trade publications… It appears that many cases seeking funding do not engage in any sort of bidding process with funders, but instead simply accept funding from the first broker who makes an offer they deem reasonable. The other major factor that seems to play a role in funder selection is any existing relationship between the attorney and the funder… Some firms also employ artificial intelligence (AI) tools that use algorithms to mine databases as a first pass at identifying potential cases.”

Healey, McDonald, and Haley

Screening Process

A critical part of the process in deciding to invest in a litigation case is the screening process that should take place before a potential case goes to full underwriting. “Generally, funders look for such case characteristics as:

- Strong legal merits

- Defendants who are financially capable of paying the claim

- A case that will result in an enforceable judgment

- A highly reputable counsel/legal team

- A case where a successful outcome will have a meaningful financial upside

- An attractive damages-to-investment ratio

- Time to expected settlement or case judgment”

Underwriting

“The underwriting process involves an in-depth analysis of a case, including extrinsic factors that could impact a favorable recovery, such as regulatory changes. Many firms have internal underwriting teams consisting of seasoned law professionals, some with specific areas of expertise. These teams examine documentation surrounding a case and consider such factors as pricing, return, collectability risk, jurisdictional risk, and procedural considerations that might impact it. Firms also may engage external legal experts with specialized expertise to perform a review of a case in addition to their own in-house work.”

Case Structuring

“A key component of this stage is drafting the investment agreement, which clearly outlines the rights and obligations of all parties involved in the litigation financing. This document covers such features as pricing and payment terms, including the order of payment in the event of a successful claim and a budget for the case, including key milestones. Most investment agreements also include an attorney’s undertaking or acknowledgment, which is a series of covenants compelling the plaintiff’s attorney to comply with the terms of the investment agreement and to engage in (or refrain from) certain actions.”

“Litigation finance firms often assign case managers to negotiate the investment management agreement, continue to monitor the case after it is consummated, and manage its budget as it moves forward. Note that the funder’s ‘control’ of the case cannot extend to any decision-making with regard to the legal management of the case.”

Structure of Litigation Funds

Typical litigation finance funds are designed around a private equity-like structure involving committed capital that is drawn down as it is deployed, along with a fixed investment term, typically three to four years.(2) Some private investment funds also offer the option to co-invest in individual cases alongside a broader fund investment. Investment minimums range from $5,000 in a single case to a more typical $1–$5 million, or even as much as $10 million for larger, established funds. Pricing for litigation finance transactions may be based on a multiple of the amount of capital provided, a percentage of the recovery in the underlying claim, or some combination. In a typical example, pricing increases the longer a case is expected to last.

Risk and Rewards

Among Healey, McDonald, and Haley’s key findings were that

“IRRs [internal rates of return] for funding transactions available from publicly traded firms suggest the possibility that they can exceed 20%.” In addition, those high returns have exhibited limited correlation to other investment areas. However, they also noted the high returns are compensation for the large risks as “these cases carry significant risk: if the case is lost, the investment has close to zero value (though sometimes a very small settlement may be reached to avoid ongoing appeals).”

They added:

“Settled case loans typically carry lower interest rates than unsettled case loans, given the difference in risk. In some cases these are recourse loans, where the borrowing law firm’s partners directly guarantee the loans themselves. That additional security serves to lower risk and the associated interest rate.”

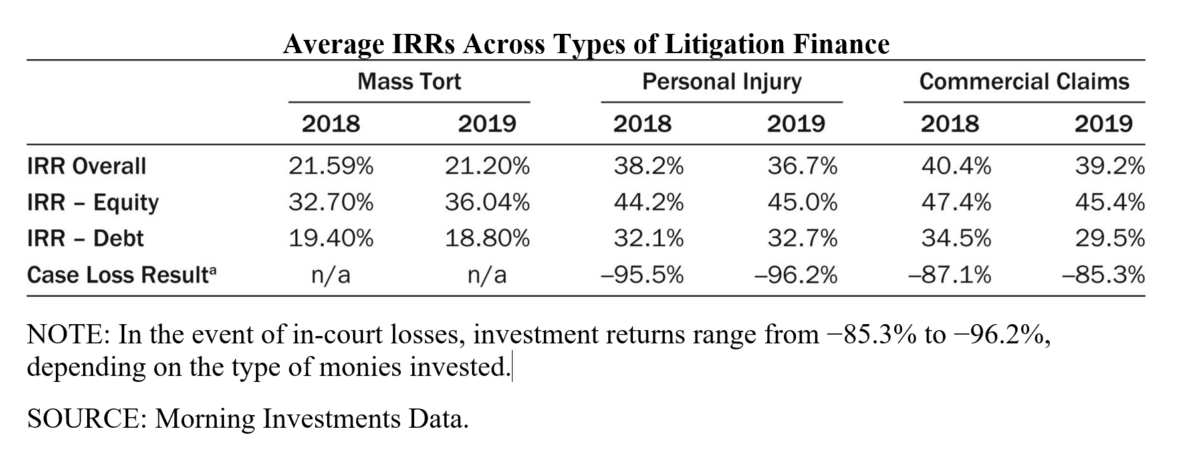

The following table shows the

“mean returns for a sample of 214 transactions made by litigation finance funds in the areas of mass tort, personal injury, and commercial claims. These transactions cover hundreds of thousands of individual cases in personal injury and mass tort, and dozens of transactions in the commercial claims space. All transactions shown are based on realized cash flows for claims finalized in the year in question.”

Healey, McDonald, and Haley noted:

“Stronger investment opportunities are able to attract debt-style investments [having lower costs], while weaker ones attract equity investments that feature fewer investor controls over the investment, and debt deals may involve quasi-covenants to give investors some control over the putative borrower.”

In terms of risk of loss:

“An evaluation of more than 100,000 actual litigation finance investments in the personal injury space between 2009 and 2018 revealed that approximately 3% of cases involved a partial loss or full write-off for the funder.”

Their findings led Healey, McDonald, and Haley to conclude that the

“excess return may be due to information asymmetry and barriers to entry in the space.”

They added:

“Barriers to greater acceptance of this asset class (including institutional conservatism and a lack of understanding) are falling slowly, resulting in continuing opportunities for excess returns.”

Perhaps their paper will speed up the process.

Summary

Thanks to the high realized returns achieved and the lack of correlation with traditional assets litigation finance is one of the classes that has shared in the influx of capital targeting alternative investments. Institutional investors, endowments, and foundations already are making significant investments in litigation finance. It is a specialized niche that is experiencing rapid growth with multi-billion-dollar firms even making litigation finance their sole business.

For investors, the highly specialized nature of the risks makes it imperative that thorough due diligence be performed to ensure that an investment firm has the resources to source and negotiate quality products, perform the necessary screening and underwriting, and manage the process until closure. The firm should also have the expertise to capture the benefits of artificial intelligence which increasingly is enhancing the efficiency and productivity of the litigation funding process. And it should provide broad diversification to minimize the high idiosyncratic risk of each individual case.

Finally, investors considering an allocation to litigation finance should not forecast the type of rates of returns that have been experienced in the past (e.g., 20% IRR) because the knowledge of those high returns, along with the lack of correlation to traditional assets, is bringing increased attention and cash flows to the space. As the asset class becomes more familiar/popular, the increase in capital allocated to the space could lead to lower future returns. With that said, the global market for litigation finance is huge, estimated at more than $400 billion in annual legal expenditures on cases. Thus, there is plenty of capacity to absorb new investment flows.

Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. Investors should carefully consider interval fund risks and investment objective, as an investment in interval funds may not be appropriate for all investors and interval funds is not designed to be a complete investment program. There can be no assurance that interval funds will achieve its investment objective, or the estimates/projections. An investment in any interval fund involves a high degree of risk. It is possible that investing in interval funds may result in a loss of some or all the amount invested. Before investing in any interval fund, an investor should read the discussion of the risks of investing in such fund and the risks in the prospectus. LSR-22-290

References[+]

| ↑1 | https://www.lexshares.com/litigation-finance-101 |

|---|---|

| ↑2 | There are also interval funds, such as Cliffwater’s Enhanced Lending Fund (CELFX) which provide limited quarterly liquidity that has allocations to litigation finance. |

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.