The article explores the behaviors and decision-making processes of institutional investors in managing their investment portfolios. It focuses on understanding their asset allocations, evaluation horizons, termination frequencies, holding periods before termination, and reasons for terminating investment managers.

Forbearance in Institutional Investment Management: Evidence from Survey Data

- Goyal, Tol and Wahal

- FAJ, 2023

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

- What are the evaluation horizons and termination frequencies for external asset managers employed by institutional investors?

- Who are the decision makers?

- What factors influence institutional investors’ tolerance for underperformance by asset managers?

What are the Academic Insights?

By studying survey data from 218 global institutional investors in 22 countries and $4.1 trillion AUM, the authors find:

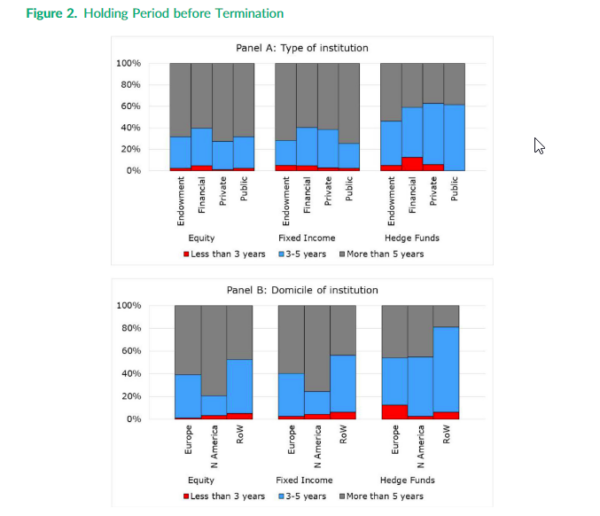

- Evaluation Horizons: approximately 70% of the surveyed institutional investors evaluate their asset managers at least quarterly. 95% of the surveyed institutional investors evaluate their asset managers at least annually. Additionally, holding periods for asset managers are generally quite long, with more than 97% of respondents reporting holding periods of greater than three years for equity and fixed income investments. For hedge funds, more than 94% of respondents report holding periods greater than three years. The study highlights that holding periods are longer than expected, indicating a certain level of forbearance or patience among institutional investors with respect to their investment managers.

- The decision makers are:

- Chief Investment Officer (CIO), accounting for 33% of the decisions.

- Head of the Manager Selection Team, responsible for approximately 21%

- Pension Board, accounting for approximately 20%

- Investment Consultants: Surprisingly, investment consultants are rarely responsible for termination decisions

- The primary reasons for terminating investment managers are categorized into three main categories: performance-related, risk-related, and organization-related reasons:

- Benchmarking: The use of multi-factor benchmarks negatively affects institutional investors’ tolerance for underperformance. Institutions that use multi-factor benchmarks may be more sophisticated in assessing risk and return, leading to less patience with underperforming managers

- Tracking Error Tolerance: Institutional investors’ tolerance for underperformance is positively related to their tolerance for tracking error. Higher tracking error tolerance indicates a willingness to accept greater deviations from the benchmark, which may result in a longer period of patience with underperforming managers

- Locus of Control: The study examines whether the decision-makers’ characteristics influence forbearance. However, the results do not show a significant impact of the locus of control (whether the decision-makers are internal or external) on institutional investors’ tolerance for underperformance

Why does this study matter?

This study contributes to the academic and practical understanding of institutional investment management, providing valuable insights into the dynamics of investor behavior and decision-making. The findings offer guidance for institutional investors, asset managers, and policymakers, ultimately aiming to improve the effectiveness and efficiency of the investment management process and enhance the long-term sustainability of investment strategies.

The Most Important Chart from the Paper:

Abstract

We survey 218 institutional investors from 22 countries representing over $4.1 trillion in AUM to understand the drivers of forbearance in the termination of external asset managers. Although asset managers are fired for a variety of reasons, including taking on too much or too little risk as well as organizational changes at the investment manager or institutional investor level, poor performance is by far the dominant cause. There is surprising tolerance for underperformance and holding periods for investment managers are unexpectedly long. Forbearance is important and we argue that performance evaluation should be multifaceted, akin to a Bayesian decision-maker who conducts continued due diligence and updates beliefs about returns with process information.

About the Author: Elisabetta Basilico, PhD, CFA

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.