How do stock prices react to earnings announcements?

Sometimes prices go up, and sometimes they go down. But here is a potentially more interesting question: What is the average performance across all stocks that have an announcement?

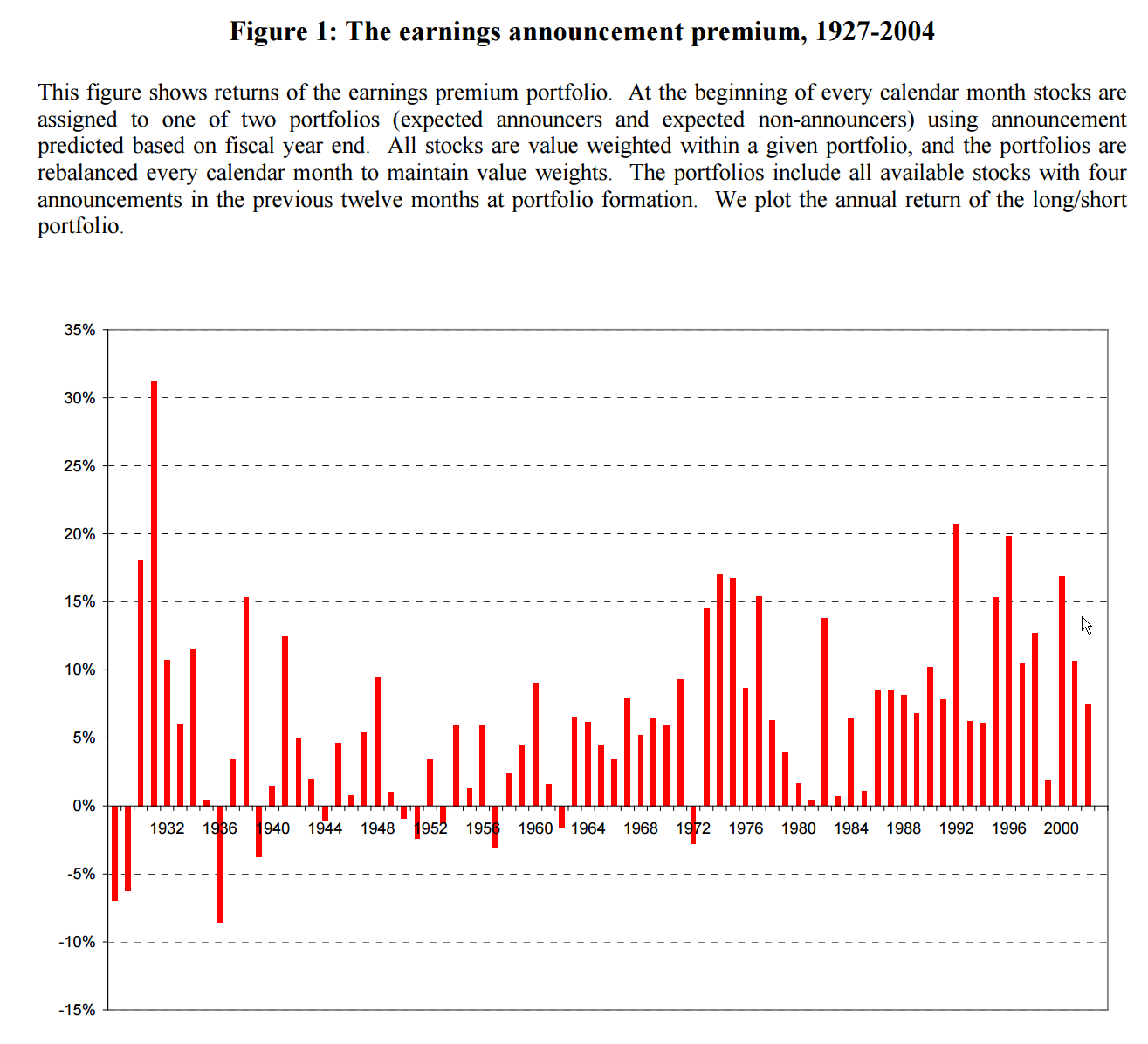

The question of whether stocks earn excess returns in announcement months was first investigated by Prof. William Beaver back in 1968. He found that the magnitude of price changes during earnings reporting periods was indeed significantly larger than during nonreporting periods, which is consistent with the idea that earnings reports convey potentially useful information for investors. Subsequently, an extensive body of literature investigated this phenomenon, which came to be known as the “Earnings announcement premium.” The figure below, sourced from a Frazzini and Lamont (2007) paper, shows the premium from 1927 to 2004 for a long/short portfolio that goes long expected announcers and short expected non-announcers:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Not bad. Simply buying announcers and shorting non-announcers has paid off, on average.

How’s the Effect look Across the Globe?

Recent research by Barber, De George, and et al. (2013) extends this research by exploring, 1) the extent to which this is a global phenomenon, and 2) whether there are cross-country variations on the magnitude of the effect that would shed light on the premium.

Using a sample of 200,000 announcements across 46 global stock markets, the authors construct a portfolio that goes long stocks that are expected to announce earnings during the month and shorts an equal dollar amount of non-announcers. This L/S portfolio earns a raw annualized return of 7.16% from 1991 to 2010 (see the figure below). That’s impressive when you consider that $1 invested in the long/short portfolio would have grown to $4.14 by 2010, versus a long-only equal-weighted global portfolio that grows to $3.64.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

In addition, the Sharpe ratio for the L/S portfolio is 40% higher than for the global portfolio. And after controlling for size, value and momentum (employing a Fama-MacBeth approach), the effect appears to hold.

Intriguingly, the effect seems widespread, and is significantly positive in 9 of the 20 countries with the most observations, although the premium appears to vary by country, from a low of 63 bps in France, versus a high of 236 bps in the UK.

Is this anomaly driven by increased risk?

Why should this effect exist at all?

Eugene Fama might reasonably argue that higher expected returns should coincide with increased risk. However, the authors find no corroborating evidence the premium is compensation for increased systematic risk, or the type of risk that cannot be diversified away. Rather, the authors find it is idiosyncratic volatility (i.e., high uncertainty that is unrelated to common macro factors) that is abnormally higher during the annual announcement window, when compared with non-announcement periods. Additionally, the premium is strongest in countries with the greatest increase in idiosyncratic volatility around earnings announcements. The authors conclude it is idiosyncratic volatility (uncertainty) that drives the earnings announcement premium. But if investors are earning excess returns for holding diversifiable risk we are entering the “anomaly zone.” See our thoughts on value and momentum for other examples.

{kind=link}

If it is idiosyncratic risk, rather than systematic risk, that accounts for these abnormal returns, then another explanation is needed for why the announcement premium exists. The authors explore a handful of possible behavioral-based explanations. For example:

- Investors’ attention: Lamont and Frazzini (2007) and Barber, et al. (2011) hypothesizes that announcements catch the attention of investors, especially small investors, which creates upward pressure on the stock prices. Barber et al. do not find evidence that supports this interpretation.

- Seasonality: Heston and Sadka (2008, 2010) hypothesize that the earnings announcement premium could potentially be a manifestation of return seasonality. Barber et al. are skeptical of this interpretation as well.

- Limit of arbitrage: Cohen, et al. (2007) suggest that the premia are not completely eliminated because of the costs of arbitrage. Barber, et al. also question this interpretation.

Finding no strong evidence for a behavioral interpretation either, Barber, et al. return to arguments in favor of an explanation based on systematic risk as explored by Savor and Wilson (2011), but are once again not convinced. An update of the paper by Savor and Wilson (2015) proposes and tests another risk-based explanation for the premium. Here’s the abstract:

Firms scheduled to report earnings earn an annualized abnormal return of 9.9%. We propose a risk-based explanation for this phenomenon, in which investors use announcements to revise their expectations for non-announcing firms, but can only do so imperfectly. Consequently, the covariance between firm-specific and market cash-flow news spikes around announcements, making announcers especially risky. Consistent with our hypothesis, announcer returns forecast aggregate earnings. The announcement premium is persistent across stocks, and early (late) announcers earn higher (lower) returns. Non-announcers respond to announcements in a manner consistent with our model, both across time and cross-sectionally. Finally, exposure to announcement risk is priced.

Based on this explanation, investors should be compensated for bearing earnings-related systematic risk. In this view, the performance of earnings announcers can help forecast future aggregate earnings growth. Moreover, the earnings announcement premium is persistent over time. Stocks with high (low) past announcement returns will continue to earn high (low) subsequent announcement returns.

It’s unclear how Barber, et al. would respond to this new line of inquiry, but clearly the debate rages on.

While Barber, et al. find evidence that the announcement premium exists around the globe, and is driven by idiosyncratic volatility, they point out that the transaction costs of arbitraging it are very high, since it requires a high portfolio turnover (of approximately 100% per month). In other words, the transaction costs may eat up substantially all of the excess returns. This may be the primary reason why the anomaly seems to persist — no one can trade it profitably.

The earnings announcement premium around the globe

- Barber, George, Lehavy, and Trueman

- A version of the paper can be found here.

- Want a summary of academic papers with alpha? Check out our Academic Research Recap Category.

Abstract:

U.S. stocks have been shown to earn higher returns during earnings announcement months than during non-announcement months. We document that this earnings announcement premium exists across the globe. Moreover, it is not isolated to a few countries. Of the 20 countries with enough data to conduct a within-country analysis, nine exhibit a significantly positive premium. A cross-country analysis finds that the premium is strongest in countries with the greatest increase in idiosyncratic volatility around the time of their firms’ earnings announcements, suggesting that uncertainty over the earnings information to be disclosed is a primary driver of the global announcement premium

About the Author: David Foulke

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.