The Best of Strategies for the Worst of Times: Can Portfolios Be Crisis Proofed?

- Campbell R. Harvey, Edward Hoyle, Sandy Rattray, Matthew Sargaison, Dan Taylor, and Otto Van Hemert

- The Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

This is a unique article in that it directly assesses the feasibility and effectiveness of protecting equity portfolios using traditional passive means and more contemporary active strategies. It is jam-packed with information and analysis that is best consumed in two parts; however, a good summary of the article by Larry Swedroe can be found here. The focus in part 1 is the usefulness of traditional passive approaches. Part 2 gets after more complex and contemporary strategies. A deeper dive into the full article will not disappoint.

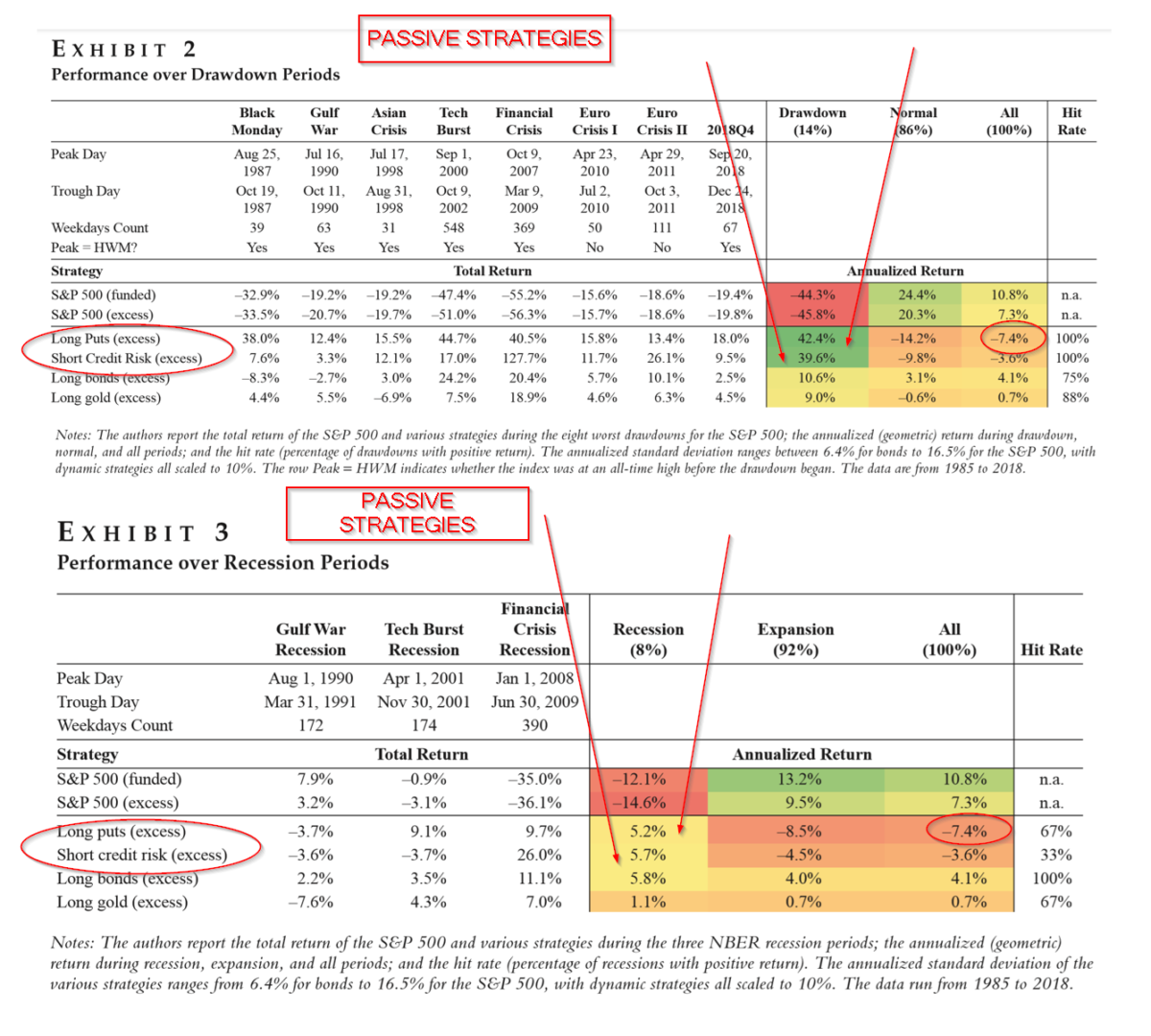

During the sample period of 1985 – 2018, 3 recessions and 8 (of the worst) equity drawdowns were identified for the US. Four passive strategies expected to benefit from declines in firm values are then evaluated on the basis of performance during the recessions and drawdown periods. The strategies include four of the most straightforward hedges available: rolling long puts, holding US 10 year Treasury bonds, long gold, and short credit risk.

- Can long-only equity portfolios be completely shielded by using passive crisis strategies?

- Which passive strategy is the most reliable during large equity drawdowns and recessions?

- Which passive strategy is the least reliable during large equity drawdowns and recessions?

What are the Academic Insights?

- YES. However, passive strategies that are 100% effective are prohibitively expensive, while the others are so unreliable as to be useless. Rolling long puts are the most effective but also the most expensive. No surprise there. Holding corporate bonds as a safe haven is the most unreliable. Long gold held as a safe haven is also less expensive than puts but more reliable than holding bonds. Short credit risk via credit default swaps (the synthetic CDX index, for example) is less expensive than long gold and more reliable than bonds. Not addressed is the difficulty in assessing the impact of mark-to-market pricing and counterparty risk that may also increase during a crisis.

- LONG PUTS The most direct hedge of the four it exhibited a 100% hit rate. This hedge performed well during all equity drawdown periods, however unevenly so. Once into the drawdown the cost of puts increases and the cost of the hedge became prohibitive, somewhere around an excess return of -7%. An equally weighted portfolio of long SP500 plus long puts resulted in an excess return that was negative over all periods. That is, negative during each equity crisis and each normal period. During recessions, the same cost disadvantage is observed. However, the returns were not as negative as long equity returns during the Gulf War recession were unexpectedly positive. One caveat: explicit transactions costs were not included and given the relatively high cost of trading options, the overall cost of the hedge would be even higher. Short credit risk hedges also exhibited a 100% hit rate. Similar to long puts, the short credit risk hedge had negative returns during non-drawdown periods. Over the entire period, the return was -3.6%. Since the year 2000, the strategy has become less effective, moving downward in a dramatic fashion. The cost of trading this hedge was very cheap. It was estimated to be less than 0.1% annually. It was, however, less reliable than the long put hedge. During the ’07-’09 recession it exhibited a large positive return while scoring a negative return during the other two recessionary periods. The authors conclude that the differentiating factor for the investor is the cost of the hedge. Investors desiring to crisis-proof portfolios face a tradeoff between reliability and cost.

- LONG GOLD AND HOLDING BONDS. Gold is the original safe haven asset offering an absolute value during market turbulence, during periods when risk aversion increases and confidence in currencies is lost. Using gold futures, 7 out of the 8 drawdowns resulted in positive returns, approximately 9% annualized. Negative returns were observed during non-drawdown periods. Consequently, performance over all periods was close to flat. Clearly, gold seems to work during drawdown periods and estimated transactions costs of continually maintaining the gold exposure were less than 0.1% per year. Performance during recessions was another story. Positive returns from maintaining the gold hedge worked for only 2 of the 3 recessions studied. Using 10 year Treasury futures resulted in consistent and positive returns during the 3 recessions. In contrast, performance during drawdown periods was positive only after the year 2000. During the pre-2000 drawdown periods, the performance was mixed. Consistent with those results, bond-equity correlations were only negative since 2000. Prior to the year 2000, for approximately 100 years, bond-equity correlations were positive. The authors suggest that these results should give investors pause. If fundamental factors are logically and empirically likely to drive a positive bond-equity correlation, there is little confidence that a long bond position will provide an effective drawdown hedge in the future.

Why does it matter?

This was an excellent article for reasons that I hope were made obvious. In addition to the empirical analysis, the authors provide numerous insights into the nuts and bolts of how passive strategies may perform over crisis periods. The discussion of the behavior of bond-equity correlations since 1900 is particularly insightful. Part 2 of this summary is in process and covers a similar analysis of hedging strategies that are contemporary and more active in nature and substance.

Stay tuned.

The most important chart from the paper

Abstract

In the late stages of long bull markets, a popular question arises: What steps can an investor take to mitigate the impact of the inevitable large equity correction? Hedging equity portfolios is notoriously difficult and expensive. In this article, the authors analyze the performance of different tools that investors could deploy. For example, continuously holding short-dated S&P 500 put options is the most reliable defensive method but also the most costly strategy. Holding safe-haven US Treasury bonds produces a positive carry but may be an unreliable crisis-hedge strategy because the post-2000 negative bond– equity correlation is a historical rarity. Long gold and long credit protection portfolios sit between puts and bonds in terms of both cost and reliability. Dynamic strategies that performed well during past drawdowns include futures time-series momentum (which benefits from extended equity sell-offs) and a quality strategy that takes long (short) positions in the highest (lowest) quality company stocks (which benefits from a flight-to-quality effect during crises). The authors examine both large equity drawdowns and recessions. They also provide some out-of-sample evidence of the defensive performance of these strategies relative to an earlier, related article.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.