There is a substantial body of evidence linking various accounting ratios to expected stock returns. One explanation of the links is that they could be explained by the accounting ratios being associated with systematic sources of risk. Alternatively, they could be associated with mispricing that arises from systematically biased investor expectations (see here for a discussion on this topic).

Here is a list of the many anomalies associated with accounting variables:

- Accruals: Firms with high accruals earn abnormally lower average returns than firms with low accruals. Investors overestimate the persistence of the accrual component of earnings when forming earnings expectations.

- Net Operating Assets: The difference in a firm’s balance sheet between all operating assets and all operating liabilities, scaled by total assets, is a strong negative predictor of long-run stock returns. Investors tend to focus on accounting profitability, neglecting information about cash profitability, in which case net operating assets (equivalently measured as the cumulative difference between operating income and free cash flow) captures such a bias.

- Asset Growth: Companies that grow their total assets more earn lower subsequent returns. Investors overreact to changes in future business prospects implied by asset expansions.

- Investment-to-Assets: Higher past investment predicts abnormally lower future returns.

- O-Score: An accounting measure of the likelihood of bankruptcy. Firms with higher O-scores (more likely to go bankrupt) have lower returns.

- Gross Profitability Premium: More-profitable firms have higher returns than less-profitable ones.

- Return on Assets: More-profitable firms have higher expected returns than less-profitable firms.

Gregg Fisher, Ronnie Shah, and Sheridan Titman contribute to the literature on mispricing anomalies with their September 2019 study “Do Growth Expectations Help Explain Characteristic-Sorted Portfolio Returns?”.

They examined the biases of long-term earnings forecasts of sell-side analysts, decomposing their forecasts into two components:

- a hard component, which can be explained by accounting variables that predict returns, and:

- a soft component, which is the residual.

Specifically, they examined a profitability measure, a sales growth measure, a net equity issuance measure (net stock issuance and stock returns are negatively correlated as smart managers issue shares when sentiment-driven traders push prices to overvalued levels), and an asset growth measure.

Their data sample included all NYSE, AMEX, and NASDAQ stocks listed on both the Center for Research in Security Prices (CRSP) return files and the Compustat annual industrial files from 1982 through 2014.

Risk or Mispricing?

The following is a summary of their findings:

- The soft component of growth is positively related to actual earnings growth.

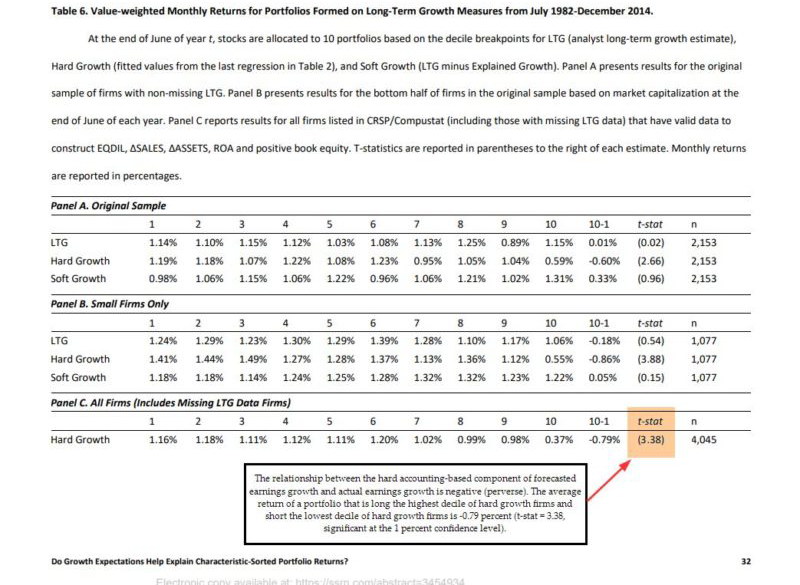

- The relationship between the hard accounting-based component of forecasted earnings growth and actual earnings growth is negative (perverse). The average return of a portfolio that is long the highest decile of hard growth firms and short the lowest decile of hard growth firms is -0.79 percent (t-stat = 3.38, significant at the 1 percent confidence level).

- Realized earnings per share (EPS) growth lines up with projected growth—increasing monotonically from a low of 3.0 percent for the quintile portfolio with the lowest long-term growth (LTG) to a high of 13.6 percent for the highest LTG. However, the average forecast error also increases monotonically moving from left to right, rising from 3.9 percent for the lowest LTG growth to 14.4 percent for the highest LTG group.

- Even the lowest expected-growth firms based on LTG miss their long-term earnings projections, although the misses are relatively small. In contrast, the highest expected-growth firms have average realized growth that is more than 50 percent less than their ex-ante forecasts.

- Forecasts are consistent with analysts believing that profits are mean-reverting. However, profitability actually tends to be fairly persistent.

- Forecasts are consistent with analysts believing that high past sales growth is a good predictor of future earnings growth. However, high sales growth is actually weakly negatively associated with future earnings growth.

- Managerial choices that reflect expected growth, such as the rate of asset growth and the use of external financing, are associated with higher earnings growth forecasts. However, the relationship between these choices and realized earnings growth is actually negative.

- The hard component of forecasted earnings growth is strongly negatively related to revisions in long-term earnings forecasts.

- High expected-growth firms tend to have greater equity dilution and higher past sales and asset growth— the highest growth group has equity dilution ratios, sales and asset growth rates that are twice as large as the 4th quintile.

- Consistent with the idea that greater growth prospects are reflected in higher valuation ratios, high-growth firms tend to have much higher valuation ratios. The highest growth group has a market capitalization that is on average 39x next-period expected earnings, while the lowest growth group has a market capitalization that is only 14x next-period expected earnings.

That is a slew of conclusions, but generally what they show is that the hard component (the accounting ratios) of forecasted earnings growth is strongly negatively related to revisions in long-term earnings forecasts, which exhibits a bias in the initial forecasts. Having established that there are biases in the forecasts, they next asked if market prices influenced by these biases?

They found that:

“stock prices reflect both that stocks have higher prices relative to forward earnings when the hard component as well as the soft component indicate greater expected earnings growth. Thus, investors set prices and growth expectations too high for stocks with low profitability, high sales and asset growth, as well as high use of external financing.” Gregg Fisher, Ronnie Shah, and Sheridan Titman, Do Growth Expectations Help Explain Characteristic-Sorted Portfolio Returns?

They also found that “soft component of earnings growth does not predict future returns – the evidence suggests that this information is efficiently captured by market prices.” They noted that their findings add to the body of evidence that: “overly optimistic long-term growth forecasts contribute to the value premium and that growth stocks underperform when high expectations are not met.”

Conclusion: Analysts are Biased

Fisher, Shah, and Titman concluded:

Although we do not identify new quantitative strategies per se, our analysis helps to understand what causes the mispricing. In particular, hard information signals that are not good predictors of future earnings do in fact explain long-term earnings forecasts as well as forward earnings-to-price ratios.

They added:

Our results suggest that analysts make mistakes when interpreting the persistence of accounting information while setting growth expectations.

Explaining:

Our evidence suggests that investors are pessimistic about highly profitable firms, potentially because they think profits are more mean-reverting than they actually are, and that they are optimistic when firms take actions that promote growth, possibly because they fail to account for managers making choices that are either overly optimistic or have “empire building” tendencies.

The question for investors is now that these findings have been published, will the anomalies persist? Will these characteristics continue to be associated with what appears to be biases in analyst long-term growth forecasts?

About the Author: Larry Swedroe

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.