Institutional Investment Strategy and Manager Choice: A Critique

- Richard M. Ennis

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Historically Institutional investors have been considered the “smart money” in investment circles. What academic research has tended to show is that the smart money status of institutional investing has some chinks in its armor, as can be seen in a previous paper we summarized here. In this article, which was recently published in the Journal of Portfolio Management, Richard Ennis begins his critique of the performance of institutional investors with this thought:

“Institutional investors speak in reverent terms of the importance of sound policy as the foundation for their work, but that is not what drives them.”

So what has driven institutional investors? A peek at the past gives us some clues.

- What investment themes have driven institutional investors?

- How did the surge in Alternatives perform?

- Did subgroups of institutional investors, including public pension and endowment funds, fare any better?

- Should institutional investors “reboot” and remake investment policy?

What are the Academic Insights?

- DIVERSIFICATION across asset classes appeared to be a top priority. The drive toward increasing diversification took the form of adding Alternatives in order to provide a source of uncorrelated equity returns. During the decade of 1999-2008, institutional investors made limited investments in passive products with allocations of 20% for Public Pensions and14% for Endowments. Public Pensions allocated 52% to active strategies and Endowments allocated 28%. Alternatives came in at 28% for Pensions and a whopping 58% for Endowments. However, that effort was a disappointment as relevant metrics moved in the wrong direction: R-square’s increased, and tracking error decreased. For endowments and pensions, the metrics show that portfolios became increasingly correlated to their benchmarks as institutional investors added non-US stocks, then private equity and hedge funds were added to the mix.

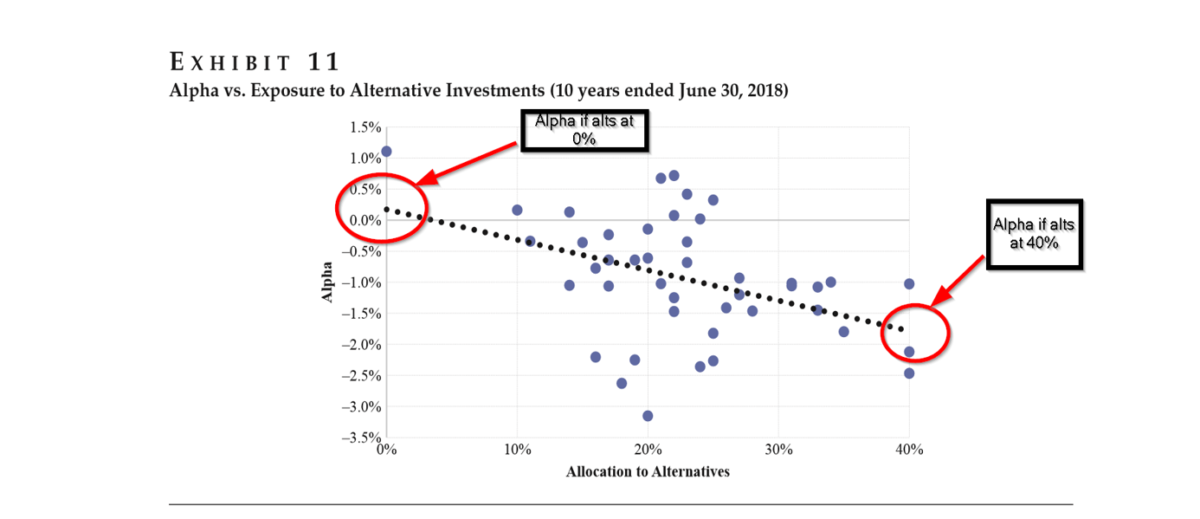

- POORLY. Alternatives failed to deliver on both cost and performance. In the decade since 2008, the reliance on Alternatives has largely failed to deliver exceptional returns. The author documents a reduction in total return of 36 bps per 10 percentage points of alternatives exposure. In terms of excess returns, there was a reduction in alpha of nearly 200 bps relative associated with a 40% allocation to alternatives as shown in the chart below.

- NO. Public pensions and endowment funds did not fare much better when compared to a passive benchmark. Composites of pension and endowments exhibited a statistically significant but negative alpha compared to a 70/30 passive benchmark over the 10 year period. The estimated cost of managing the pension and endowment programs was 0.98% and 1.67% respectively, which was very close to the magnitude of the underperformance. Out of 46 pension funds studied only one showed a positive significant alpha while 17 exhibited a negative but significant alpha. The values for the remaining funds were not statistically significant.

- YES. The author makes two prescriptions:

First, allocate 50% of the portfolio to a few stock and bond index funds

Rationale: Exploit the opportunity to reduce investment expenses to a minimum. This has the added incentive of increasing the chance of outperforming peers who fail to follow suit, over the long run. This prescription applies to large, small, public and private institutional funds. Strive for true passive management obtained at the lowest possible cost. Do not allow the passive choice to be ancillary to other decisions. Passive equity is broad-based, capitalization weighted, and should include international developed and emerging markets. For fixed income, any commercial investment-grade index fund will suffice.

Second, continue to alter the passive allocation in a systematic fashion

Rationale: Based on the performance of their active investments. If active managers underperform the benchmark, then transfer assets to the passive allocation. If active managers outperform net of costs, then reallocate passive funds if sufficient justification exists.

Why does it matter?

Although the sample period is short for making prescriptions about policy, the advice is clear: Keep it simple and lower costs.

A quote from the author:

“Institutional investors speak in reverent terms of the importance of sound policy as the foundation for their work, but that is not what drives them……..If experience tells us anything about institutional investing, it is that low cost trumps genius over the long run….. The key here is to overcome the temptation to be clever. At the risk of being repetitive, the idea is to capture broad market exposures at the lowest possible cost with minimal maintenance.”

The most important chart from the paper

Abstract

The diversification of public pension funds and educational endowments is explained by a few stock and bond indexes alone. Alternative investments ceased to be diversifiers in the 2000s and have become a significant drag on institutional fund performance. Public pension funds underperformed passive investment by 1.0% a year over a recent decade; the annual shortfall of endowments is 1.6% a year. Given the extent of institutional diversification, the diminished effect of alternatives, and the funds’ prevailing cost structure, institutional investors face the prospect of continuing significant underperformance in the years ahead. There is a better approach to institutional investment strategy and manager choice.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.