Out of Sight No More? The Effect of Fee Disclosures on 401(k) Investment Allocations

- Kronlund, Pool, Sialm and Stefanescu

- Journal of Financial Economics, 2021

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

This study asks the following:

- Did the 2012 participant-level disclosure reform by the Department of Labor ( which requires fiduciaries to provide expense- and performance-related summary statements directly to participants(1)) affect investment decisions in 401(k) plans?

- Who reacts to fee information?

What are the Academic Insights?

By hand-collecting information on the menu of options offered in a large sample of 401(k) plans using plan-level annual filings from 2010 to 2013, along with participants’ allocations to each of these options, the authors find:

- Yes, fee reform worked.

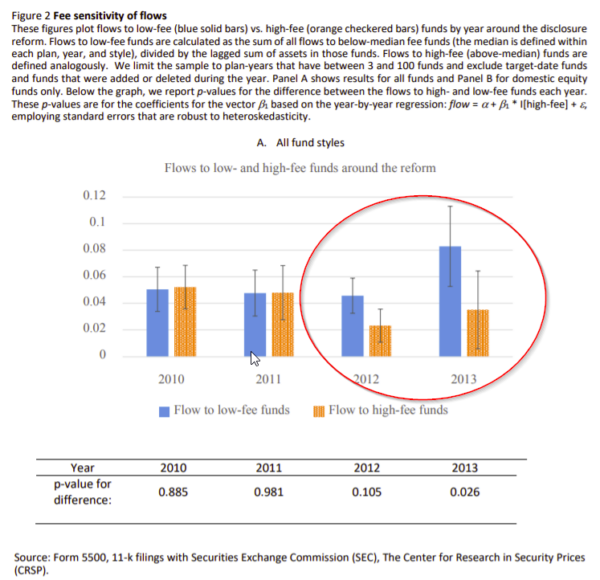

- Participants’ sensitivity to fees increases after the reform. For example, funds with a one-standard-deviation higher expense ratio (i.e., 0.36 percentage points) experience a statistically significant reduction in their plan share of 0.17 percentage points per year after the regulatory change.

- Investors actively move money away from expensive funds: a one-standard-deviation increase in the expense ratio is associated with an eight percentage points higher probability that a fund experiences negative flows after the reform.

- The impact of the reform is non-linear: participants become especially sensitive to the lowest-fee funds. These extreme funds receive abnormally high flows after the regulatory change, beyond what can be explained by the linear expense ratio. In fact, the authors find that investors allocate significantly more flows toward index funds after the reform.

- The authors consider the fact that the results may not be unique to the 2012 regulatory reform. To address these concerns, the authors re-run the analysis using a series of placebo periods, where they counterfactually assume that the regulatory reform occurred in different years. They do not find a discontinuous relation between fees and changes to flows around these placebo years.

- Certain investors react differently.

- Participant-directed investment allocations in plans where average participant contributions are larger, experience a stronger increase in their sensitivities to fund fees after the reform, compared to other plans.

- The post-reform increase in fee sensitivities is larger in plans that do not offer a large number of investment option.

- When a plan’s mutual fund investment options are particularly expensive, participants shift more assets toward the employer’s stock once they acquire better information about these fees through the new disclosures. This, according to the authors is an unintended consequence of the fee disclosure.

Why does it matter?

This paper is important because it analyses the effects of the DOL’s disclosure reform on fund allocations by 401(k) plan participants. It shows that participants become more attentive to fund fees and to short-term fund performance after the regulation. In short, fee disclosures can improve investor decision-making.

The Most Important Chart from the Paper:

Abstract

We examine the effects of a 2012 regulatory reform that mandated fee and performance disclosures for the investment options in 401(k) plans. We show that participants became significantly more attentive to expense ratios and short-term performance after the reform. The disclosure effects are stronger among plans with large average contributions per participant and weaker for plans with many investment options. Additionally, these results are not driven by secular changes in investor behavior or sponsor-initiated changes to the investment menus. Our findings suggest that providing salient fee and performance information can mitigate participants’ inertia in retirement plans.

About the Author: Wesley Gray, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.