Protecting the Downside of Trend When It Is Not Your Friend

- Kun Yang, Edward Qian, and Bran Belton

- Journal of Portfolio Management

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

We’ve done a poor job hiding our interest in Trend Following (see Trend, Trend, Trend, is your friend. And swing over to Corey Hoffstein’s site for even more!). So this paper hits on a subject we know and love. The authors of this study (part 1) have one basic objective: determine if the downside performance of a simple trend-following strategy can be improved by either adding complexity to the signal and/or improving the associated portfolio construction approach. They succeed on both counts.

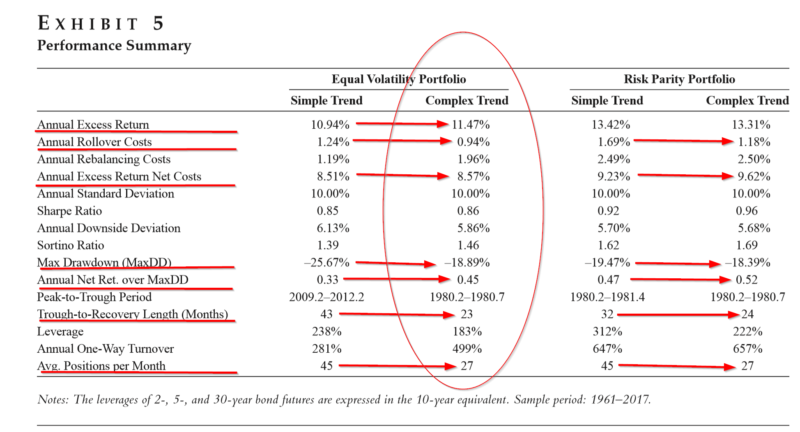

The initial signal (S=simple) used as a baseline employs the sign of asset’s trailing return and an equal volatility (EV) portfolio weighting scheme. This is then compared to results with four strategies combining a more complex signal (C=complex) and/or a risk parity (RP) construction approach. The authors describe the complex signal as a channel breakout entry and exit rule as an overlay to the simple signal. The RP approach accounts for both volatility and correlations across markets in contrast to the simple volatility weighting scheme used in the simple trend strategy.

- Can a simple form of trend-following strategies be improved by simply substituting a complex trend signal?

- Can a simple form of trend-following strategies be improved with better, more diversified portfolio construction without changing the signal?

- How robust are the results to implementation and trading costs?

What are the Academic Insights?

- YES. The complex trend strategy improved the distribution of returns vs simple trend by virtue of better downside protection. The C strategy had lower downside deviations, lower max drawdowns, and much shorter trough to recovery periods. The Sortino (downside risk-adjusted ratio) and the return over the max drawdown ratio were higher. The C strategy also had lower leverage and fewer securities, and lower rollover costs, for both equal volatility (EV) and risk parity (RP) construction methods. This was as a result of the stricter (higher standard) rule for initiating and maintaining positions. On the negative side, the C strategy had high turnover, and higher costs to rebalance as a result of the higher number of signal changes. Sharpe ratios were essentially the same for S and C portfolios regardless of the construction method.

- YES. Risk Parity (RP) portfolios are superior in that they improve the mean return and the distribution of returns due to better downside protection. The evidence shows that net of transaction costs, RP portfolios outperform EV portfolios on almost all measures: higher Sharpe and Sortino ratios, and higher return over max drawdown ratios. However, as might be expected the risk parity (RP) portfolios have higher leverage, higher turnover, higher rollover costs, and higher costs of rebalancing when compared to the equal volatility (EV) constructed portfolios. The negative attributes of the risk parity (RP) construction have to do with the larger need to balance risk exposures across positions and the greater exposure to changes in volatility and correlation when compared to the EV approach.

- PRETTY ROBUST. The authors account for rollover and rebalancing costs that impair portfolio performance when leverage and turnover varies considerably. They also handle implementation “slippage” by assuming a one-day trading lag. The securities in the EV (RP) portfolios targeted 40% (10%) annualized volatility for initial weights, while both construction methods were set to 10% annually, ex-post to facilitate comparisons.

Why does it matter?

Risk managers and other investors using simple trend-following strategies can enhance the expected return and distribution of those returns by adding “complexity”. (something in which we should generally be skeptical). This can be achieved in two ways: adding complexity in the form of a more complex signal such as breakout entry and exit components; and/or using a portfolio construction method that more optimally balances risk exposures as in the risk-parity approach.

The most important chart from the paper

Abstract

Simple trend-following strategies have been documented as cost-effective, transparent alternatives to the hedge-fund style managed futures strategies. Although largely capturing the returns of the managed futures industry, those simple strategies may periodically suffer significant losses due to oversimplified trend signals and underdiversified portfolio construction. In this article, the authors show that trend-following strategies with moderate sophistication and better diversification can significantly reduce the downside risk of simple trend-following strategies without sacrificing much upside potential. The authors therefore recommend that investors who seek the benefits of cost-effective trend-following strategies consider adding reasonable complexity to the strategies.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.