Dissecting Green Returns

- Lubos Pastor, Robert F. Stambaugh, Lucian A. Taylor

- SSRN working paper

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

Capitalizing on an equilibrium 2-factor (CAPM + ESG) model of the world, (henceforth the PST model as in Pastor, Stambaugh, and Taylor, 2021), this research tests and confirms its main prediction. Although theoretically green stocks have lower expected returns, they can produce higher realized returns when investor demand shifts unexpectedly in favor of green stocks (For more on the rationale of ESG performance review Larry’s post here). The sample period of this research is from 2012-2020, for US stocks, is used to address the following questions:

- What does the past performance of green assets imply about their future performance? Should green stocks’ recent outperformance lead one to expect high green returns going forward?

- If the expected return for green stocks vs. brown stocks is lower, then what accounts for the green factor’s strong realized performance over the last 10 years?

- Do stocks react in an efficient manner to climate-concern shocks?

- To what extent can the strong performance of green stocks relative to brown stocks account for the recent decade’s historic underperformance of value, or for the positive performance of momentum?

What are the Academic Insights?

- NO. As a result of investor demand for green assets, PST predicts lower expected returns to green stocks relative to brown stocks, even though in realized terms, returns are higher. What then explains the divergence? Shifts in investors taste for green stocks can shift unexpectedly a number of ways: (1) Green prices could be driven up if preferences for green stocks also increase; (2) Green stocks may become more profitable and drive demand as a result of outside influences such as environmental regulation; (3) Demand for brown stocks and their associated products and services may decrease relative to green stocks on a contemporaneous basis.

- CLIMATE CHANGE EVENTS. The authors conclude that the unexpected outperformance of green stock returns was primarily due to increased concerns about climate issues and not due to the increased demand for the products and services supplied by green stocks or flows into sustainable mutual funds. Using the media index of climate change concerns developed by Ardia et al. (2021), the authors document a substantial increase in climate change concerns over the recent decade that are associated with a significant positive relationship to green factor returns. They found green stocks outperform when the news about climate change is negative and further conclude the outperformance disappears when the interaction between the degree of greenness per stock and the shock of climate events is included in the analysis. The shock of climate concerns explains the outperformance of green stocks. Even though green returns are expected to be lower, green outperforms brown simply due to the positive surprises during this sample period.

- NO. Over the time period studied, stock prices were observed to react slowly to news about climate events. The relationship between the contemporaneous climate event and green returns was weak, while the relationship with the previous months’ climate event was positive and significant. When the time frame was collapsed to a weekly frequency the lagged effect was strongest at 4 weeks, although it did range from 2 to 5 weeks.

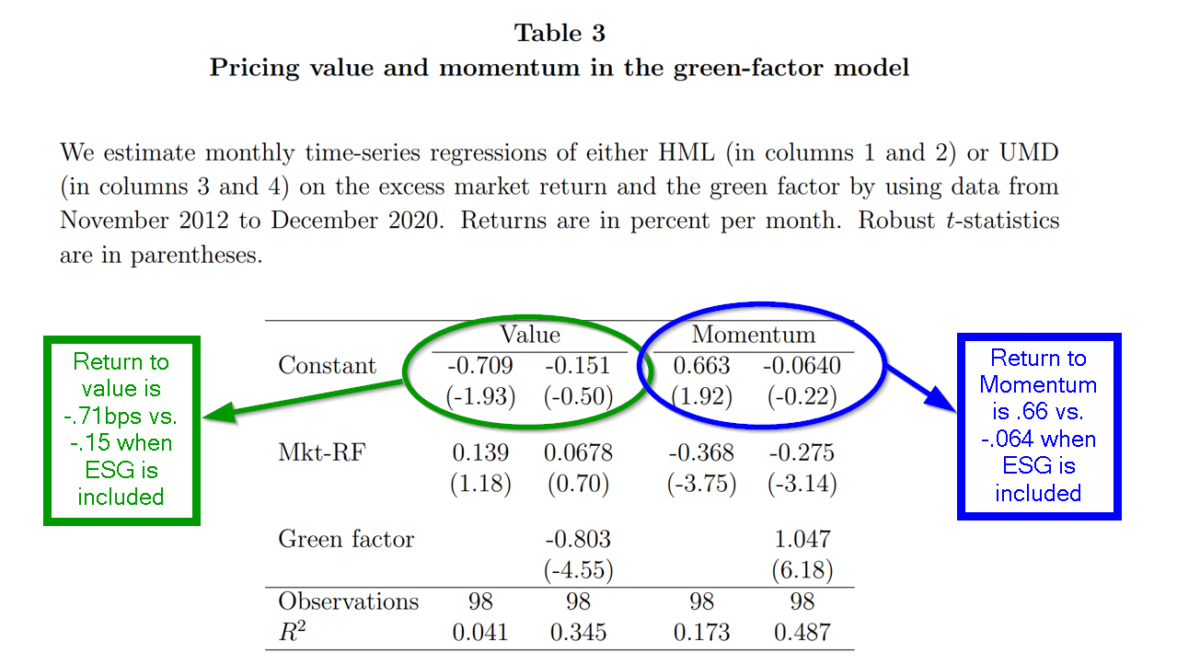

- The authors make the argument that the performance of the green factor (where the green/brown spread is substituted for the ESG factor in the 2-factor PST model) provides insight into the recent and substantial underperformance of the Fama-French HML/value factor. Assuming a 2-factor model as in PST (the market and an ESG factor), authors decompose the returns to value and to momentum separately. Regressions on value and momentum returns are conducted separately, with and without the ESG or green factor. The results are presented in table 3 below. Note that for value and momentum the excess returns present in the single-factor model disappear when the green factor is included. For value, when adding the green factor the negative excess return is reduced from -71bps to an insignificant -15bps. For momentum, when adding the green factor the positive excess return is reduced from 66bps to an insignificant -6bps. It seems that value stocks tend to be brown and growth stocks tend to be green and a change in the demand for one or the other will impact the realized returns of value stocks.

Why does it matter?

Most assuredly this is an interesting and unusual take on the cause of the very large underperformance by value stocks recently observed. If it is true that green stocks outperform brown stocks when climate events occur, that result surely has implications for modelers of climate risk. The authors explain:

Empirically confirming a climate risk premium, however, must confront the large unanticipated positive component of green stock returns during the last decade. Without accounting for those unexpectedly high returns on stocks that appear to be relatively good climate hedges, one could be led astray. That is, one could infer that stocks providing better climate hedging have higher expected returns, not lower as theory predicts.

However, in considering the results reported in this research, I would add one caveat: The use of 2- factors, even though theoretically derived, likely presents a problem with omitted variables. Taken in the context of traditional asset pricing models, the omitted variable bias is well-documented in applications of OLS. It deserves more attention in this analysis.

The most important chart from the paper

Abstract

Green assets delivered high returns in recent years. This performance reflects unexpectedly strong increases in environmental concerns, not high expected returns. German green bonds outperformed their higher-yielding non-green twins as the “greenium” widened, and U.S. green stocks outperformed brown as climate concerns strengthened. To show the latter, we construct a theoretically motivated green factor—a return spread between environmentally friendly and unfriendly stocks—and find that its positive performance disappears without climate-concern shocks. A theory-driven two-factor model featuring the green factor explains much of the recent underperformance of value stocks. Our evidence also suggests small stocks underreact to climate news.

About the Author: Tommi Johnsen, PhD

—

Important Disclosures

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.