Not sure where to start? Read the best from our research blog

By Jose Ordonez|November 28th, 2025|Predicting Market Returns, Podcasts and Video, Research Insights, Macroeconomics Research|

By Elisabetta Basilico, PhD, CFA|November 24th, 2025|Elisabetta Basilico, Factor Investing, Research Insights, Other Insights, Momentum Investing Research|

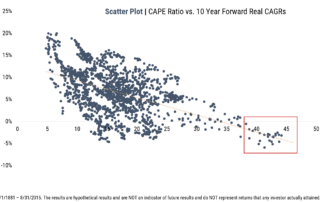

By Larry Swedroe|November 21st, 2025|Predicting Market Returns, Research Insights, Larry Swedroe, Other Insights|

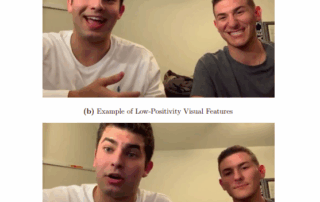

By Elisabetta Basilico, PhD, CFA|November 17th, 2025|Elisabetta Basilico, Research Insights, Other Insights, Behavioral Finance|

By Jose Ordonez|November 13th, 2025|Predicting Market Returns, Empirical Methods, Research Insights, Podcasts and Video, Macroeconomics Research|

By Elisabetta Basilico, PhD, CFA|November 10th, 2025|Elisabetta Basilico, Private Equity, Research Insights, Other Insights|

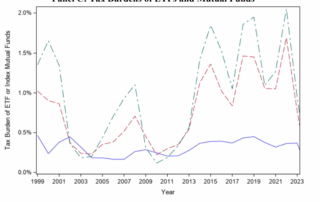

By Larry Swedroe|November 7th, 2025|Larry Swedroe, Research Insights, Other Insights, Tax Efficient Investing|

By Elisabetta Basilico, PhD, CFA|November 3rd, 2025|Elisabetta Basilico, Research Insights, Other Insights, Key Research, Behavioral Finance|